Key Takeaways

- Heavy equipment financing rates range from 0% (manufacturer promos) to 36% APR, your credit score, time in business, and lender type determine where you land.

- 82% of U.S. companies use financing when acquiring equipment, making it the industry standard, not the exception.

- Alternative lenders approve loans under $250,000 in as little as 24 hours; banks take 1–8 weeks but offer lower rates (5%–9% APR) for borrowers with 680+ credit scores.

- The 2025 Section 179 deduction limit is $1,250,000, you can deduct the full purchase price in Year 1 while only making monthly payments, a powerful cash flow advantage.

- Used equipment financing carries shorter terms (24–60 months) and rates 1–3 points higher than new, meaning a lower sticker price doesn’t guarantee a lower monthly payment.

- Most lenders cap used equipment at 5–10 years old; age restrictions disqualify more deals than credit scores do, so confirm limits before applying.

- Seasonal payment schedules and 60–90 day payment deferrals are available from select lenders, letting construction businesses align payments with project revenue cycles.

Heavy equipment doesn’t come cheap. A single excavator can run $100,000 to $500,000, and most contractors can’t (or shouldn’t) drain their working capital to buy one outright. Heavy equipment financing solves that problem by spreading the cost over months or years, keeping cash available for payroll, materials, and operations.

This guide covers everything: payment estimates, lender comparisons, bad-credit options, and more.

What Is Heavy Equipment Financing?

Heavy equipment financing is a loan or lease that lets businesses acquire construction and industrial equipment, like excavators, cranes, bulldozers, dump trucks, and more by spreading payments over time instead of paying the full purchase price upfront.

The equipment itself typically serves as collateral, making approval more accessible than unsecured business loans.

The U.S. construction equipment finance market reached approximately $20.9 billion in 2025 (Global Market Insights). That scale makes sense: the Equipment Leasing and Finance Association (ELFA) reports 82% of U.S. companies use financing when acquiring equipment. Financing heavy equipment is simply how the industry operates.

Need a broader foundation first? Start with what equipment financing is before diving into construction-specific details.

Types of Heavy Equipment You Can Finance

Most lenders will finance any machine with a clear title and resale value. Here’s what that looks like across the most common equipment categories, including typical price ranges and what’s usually financeable beyond the base unit.

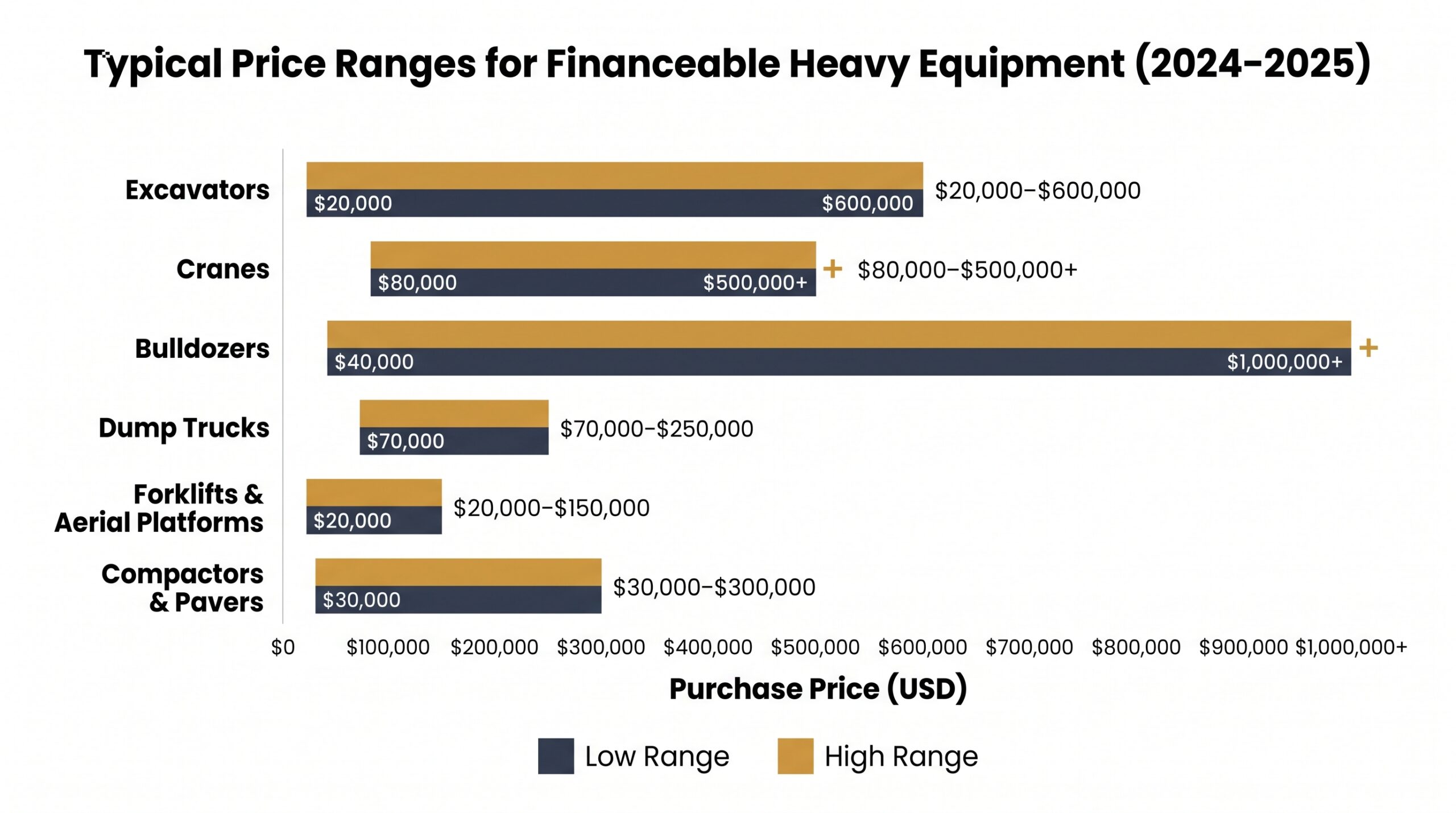

Excavators

New excavators run $20,000 to $600,000, with mid-range machines landing between $100,000 and $300,000. Heavy equipment financing is especially common here; excavators depreciate slowly and hold strong resale value, which lenders like.

Cranes

Rough-terrain cranes start around $80,000. Tower and crawler cranes push $500,000 and beyond. Financing construction equipment this large almost always makes more sense than an outright purchase.

Bulldozers and Motor Graders

Bulldozers range from $40,000 to over $1,000,000, depending on size class. Motor graders sit in a similar band. Both hold collateral value well.

Dump Trucks and Haul Trucks

Commercial dump trucks typically cost $70,000 to $250,000 new. See our guide to dump truck and fleet financing for fleet-specific strategies.

Forklifts and Aerial Work Platforms

Forklifts start around $20,000; boom lifts and scissor lifts run $30,000 to $150,000. Both qualify for heavy construction equipment financing with standard lender terms.

Compactors, Pavers, and Road Equipment

Asphalt pavers run $50,000 to $300,000. Compactors start around $30,000. Financing heavy equipment in this category often includes attachments and delivery costs rolled into the loan.

Other Construction and Industrial Equipment

Concrete mixers, trenchers, skid steers, and drilling rigs all qualify. Soft costs, like attachments, installation, and initial maintenance, can frequently be bundled into the financing amount.

Heavy Equipment Financing vs. Leasing: Which Is Right for You?

Two structures dominate the market. The right choice depends on how long you’ll use the machine, your tax situation, and how much monthly payment flexibility you need.

Heavy Equipment Loans

You own the machine at payoff. The equipment serves as collateral, you build equity from day one, and the full purchase price is eligible for the Section 179 deduction, up to $1,220,000 in 2024. Heavy equipment financing via loans works best for machines you’ll run hard for 10+ years.

Heavy Equipment Leases

Three structures exist. A finance lease (lease-to-own) builds toward ownership. An operating lease delivers the lowest monthly payment with no equity, you return the machine at term end. Short-term equipment rental covers project-specific needs. Cat Financial, for example, offers all three through their dealer network.

When to Finance vs. When to Lease

Finance when the machine is core to your business and you want long-term asset value. Lease when you need newer equipment every few years or want lower payments to protect cash flow. See the full leasing vs. financing guide for a deeper breakdown.

| Factor | Loan | Finance Lease | Operating Lease |

|---|---|---|---|

| Ownership | You own it | Option to buy | Lender owns it |

| Monthly Payment | Higher | Moderate | Lowest |

| Tax Treatment | Section 179 / depreciation | Partial deduction | Lease payments deductible |

| End-of-Term Options | Own outright | Buy, return, or refinance | Return or buy at FMV |

| Best For | Long-term core equipment | Ownership with flexibility | Frequent upgrades |

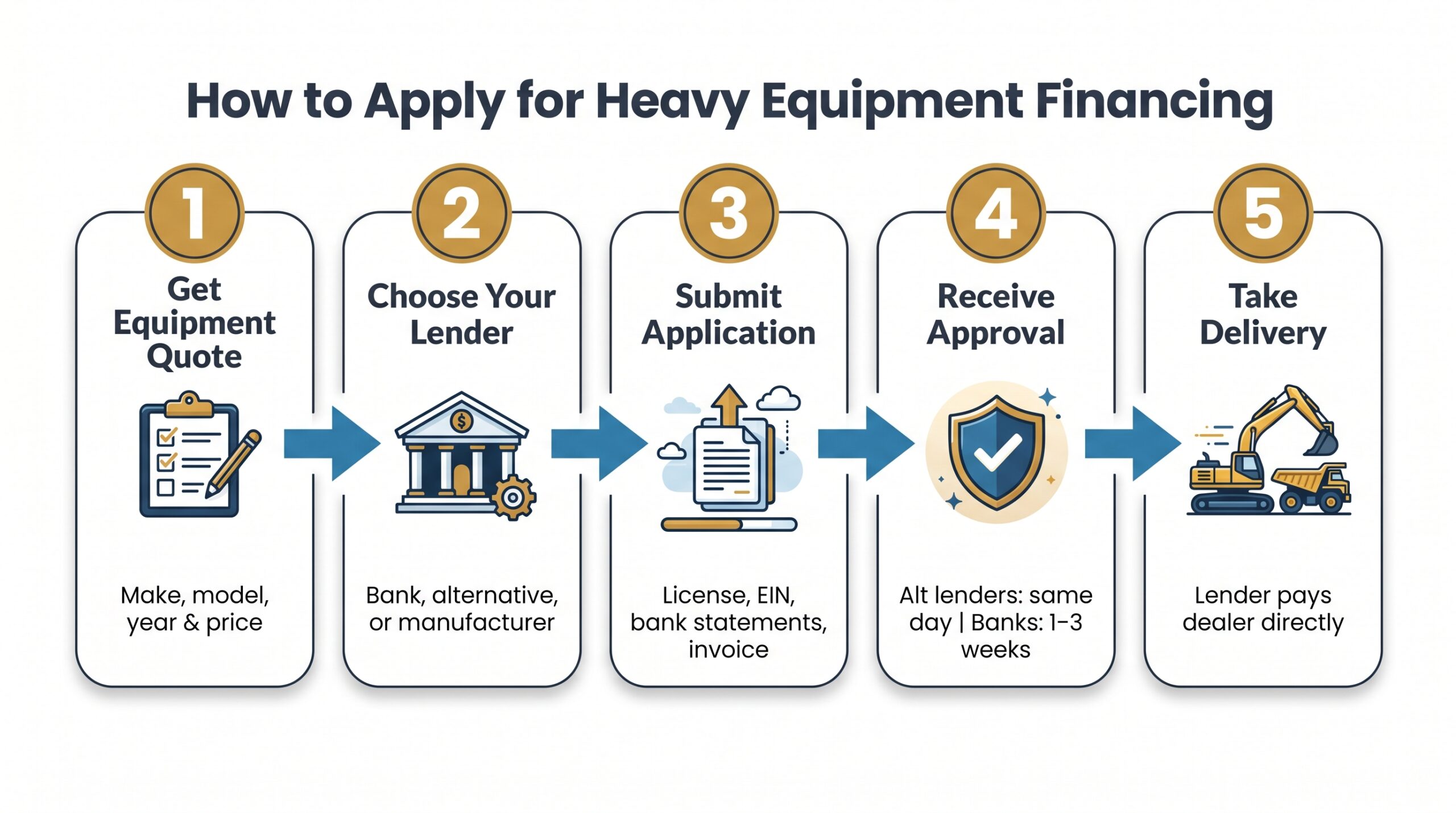

How Heavy Equipment Financing Works: Step-by-Step

The process is straightforward. Most contractors go from application to funded in 2 to 5 business days, sometimes faster.

Step 1: Choose Your Equipment and Get a Quote

Get a dealer invoice or equipment quote before you apply. Lenders need the make, model, year, and purchase price to structure your financing for heavy equipment.

Step 2: Select a Lender Type

Three main options exist: traditional banks, alternative lenders, and manufacturer programs like Cat Financial. Each has different speed, rate, and qualification tradeoffs, covered in detail in the comparison section below.

Step 3: Submit Your Application

Standard documents for heavy equipment financing include:

- Business license and EIN

- 3 to 6 months of bank statements

- Equipment invoice or dealer quote

- Business tax returns and financial statements (loans over $250,000)

Step 4: Receive Approval and Review Your Terms

Alternative lenders often deliver same-day or next-business-day decisions on loans under $250,000. Banks take longer, typically 1 to 2 weeks. Review your rate, term length, and any prepayment penalties before signing.

Step 5: Take Delivery and Start Making Payments

Once funded, the lender pays the dealer directly. You take delivery and begin your repayment schedule. Heavy construction equipment financing terms typically run 24 to 84 months, depending on loan size and machine type.

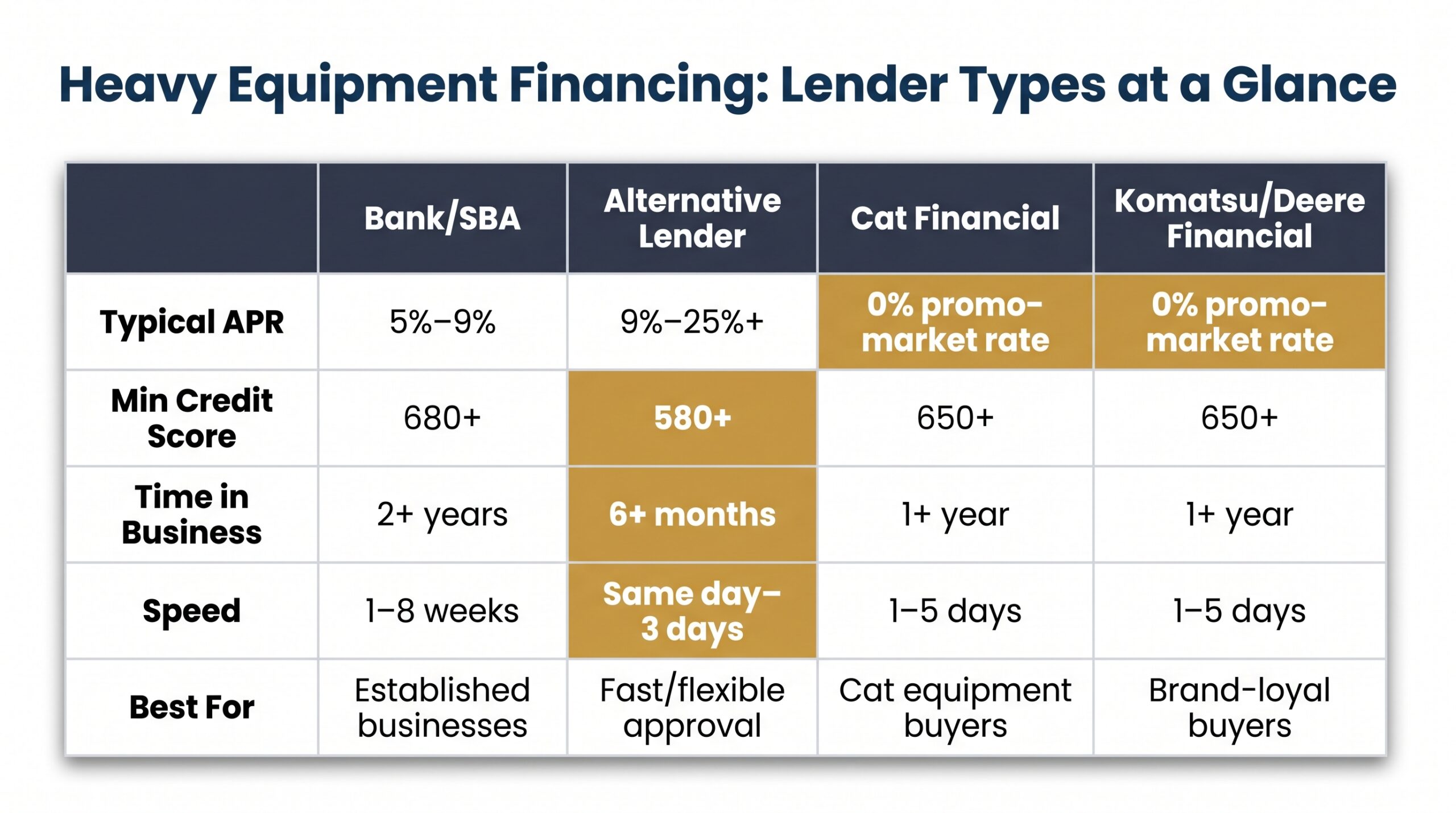

Heavy Equipment Financing Options Compared: Banks, Alternative Lenders & Manufacturer Programs

Your lender choice affects your rate, speed, and approval odds more than almost any other decision. Here’s how the three main channels stack up.

Bank and SBA Loans

Banks offer the lowest APRs (typically 5% to 9%) but require strong credit, 2+ years in business, and full financial documentation. SBA 7(a) and 504 loans work well for large equipment purchases but take 4 to 8 weeks to close. Best for established contractors with clean financials who aren’t in a hurry.

Alternative and Online Equipment Lenders

Alternative lenders approve financing for heavy equipment faster than any other channel, often same-day on loans under $250,000. APRs run 9% to 25%+, and minimum credit score requirements start as low as 580. The tradeoff is cost. Worth it when timing matters or credit isn’t perfect.

Manufacturer and Dealer Financing (Cat Financial, Komatsu, John Deere)

Caterpillar equipment financing through Cat Financial is one of the most competitive manufacturer programs available. They regularly run 0% promotional APR for up to 60 months on qualifying compact equipment, with standard rate programs for larger machines.

Komatsu Financial and John Deere Financial offer similar structures, low promotional rates tied to specific models, and purchase windows. All three require buying through an authorized dealer, but the rates frequently beat bank offerings during promotional periods.

Comparison Table: Lender Types at a Glance

| Lender Type | Typical APR | Loan Amounts | Min Credit Score | Time in Business | Speed | Best For |

|---|---|---|---|---|---|---|

| Bank / SBA | 5% – 9% | $50K – $5M+ | 680+ | 2+ years | 1 – 8 weeks | Established businesses, large purchases |

| Alternative Lender | 9% – 25%+ | $10K – $2M | 580+ | 6+ months | Same day – 3 days | Fast approval, flexible credit |

| Cat Financial | 0% promo – market rate | $20K – $2M+ | 650+ | 1+ year | 1 – 5 days | Cat equipment buyers, promo deals |

| Komatsu / Deere Financial | 0% promo – market rate | $25K – $1M+ | 650+ | 1+ year | 1 – 5 days | Brand-loyal buyers, seasonal promos |

For a full lender directory with reviewed options, see the best equipment financing companies.

How to Qualify for Heavy Equipment Financing

Qualification requirements vary significantly by lender type. Here’s what each factor actually means for your approval odds.

Credit Score Requirements

Most lenders want a 600 to 650 minimum for heavy equipment financing. Alternative lenders will go as low as 500 to 575, but expect a larger down payment and higher rate. Banks and manufacturer programs like Cat Financial typically require 650 or better.

Time in Business

Traditional lenders require 2+ years. Startup-friendly programs accept 6 to 18 months, especially when you have contracts on hand or strong personal credit. See startup equipment financing options if you’re under the two-year mark.

Revenue and Cash Flow

Most lenders want $50,000 to $250,000+ in annual revenue with consistent monthly deposits. They’re looking for proof your cash flow covers the payment, not just a number on a tax return.

Down Payment Requirements

Well-qualified borrowers often put 0% to 10% down. Startups and lower-credit applicants typically need 20% to 50%. A larger down payment reduces lender risk and can unlock better rates on financing for heavy equipment.

Equipment Age and Condition Restrictions

Most lenders cap used equipment at 5 to 10 years old or a specific hour threshold. Machines past their useful life may require a shorter loan term, higher down payment, or a co-signer. Always confirm age limits before applying; this disqualifies more deals than credit scores do.

Bad credit doesn’t automatically mean no deal. Explore no-credit-check equipment financing for alternative approval pathways.

New vs. Used Heavy Equipment Financing

New and used machines both qualify for financing, but the terms look different enough to affect your total cost significantly.

New equipment gets the best treatment: terms up to 84 months, the lowest available rates, and access to manufacturer promotional programs like Cat Financial’s 0% APR offers. Financing heavy equipment new also means no age or hour restrictions to worry about.

Used equipment financing typically comes with shorter terms (24 to 60 months) and rates 1 to 3 percentage points higher. Most lenders cap used machines at 5 to 10 years old from manufacture date and may impose hour limits, often under 5,000 to 10,000 hours for excavators and heavy construction equipment.

Here’s the tradeoff most buyers miss: a lower purchase price on used equipment doesn’t automatically mean a lower monthly payment. A shorter term and higher rate can produce payments comparable to, or higher than, financing new. Run the numbers both ways before deciding.

For a deeper look at used machine approval criteria and lender options, see our used equipment financing guide.

Heavy Equipment Financing Rates: What to Expect in 2025

Rates on heavy equipment financing range from 5% to 36% APR in 2025. Where you land depends on several factors you can actually control.

Factors That Affect Your Rate

Six variables move the needle most: credit score, time in business, down payment size, equipment type and age, loan term length, and lender type. A 720 credit score with 3 years in business and 10% down gets a very different rate than a 580 score with 8 months of history.

Rate Ranges by Lender Type

- Banks and SBA: 5% – 9% APR for well-qualified borrowers

- Mid-tier alternative lenders: 9% – 15% APR

- Higher-risk borrowers: 20% – 36% APR

- Manufacturer promos (Cat Financial, Komatsu, Deere): 0% for qualifying equipment during promotional windows

Fixed vs. Variable Rate Options

Fixed rates dominate construction equipment financing because predictable payments matter when project cash flow fluctuates. Variable rates may start lower but introduce risk if rates rise mid-term. Most contractors choose fixed.

Always use pre-qualification (soft pull) to compare offers before committing. It won’t affect your credit score. See the equipment financing rates guide for a full breakdown.

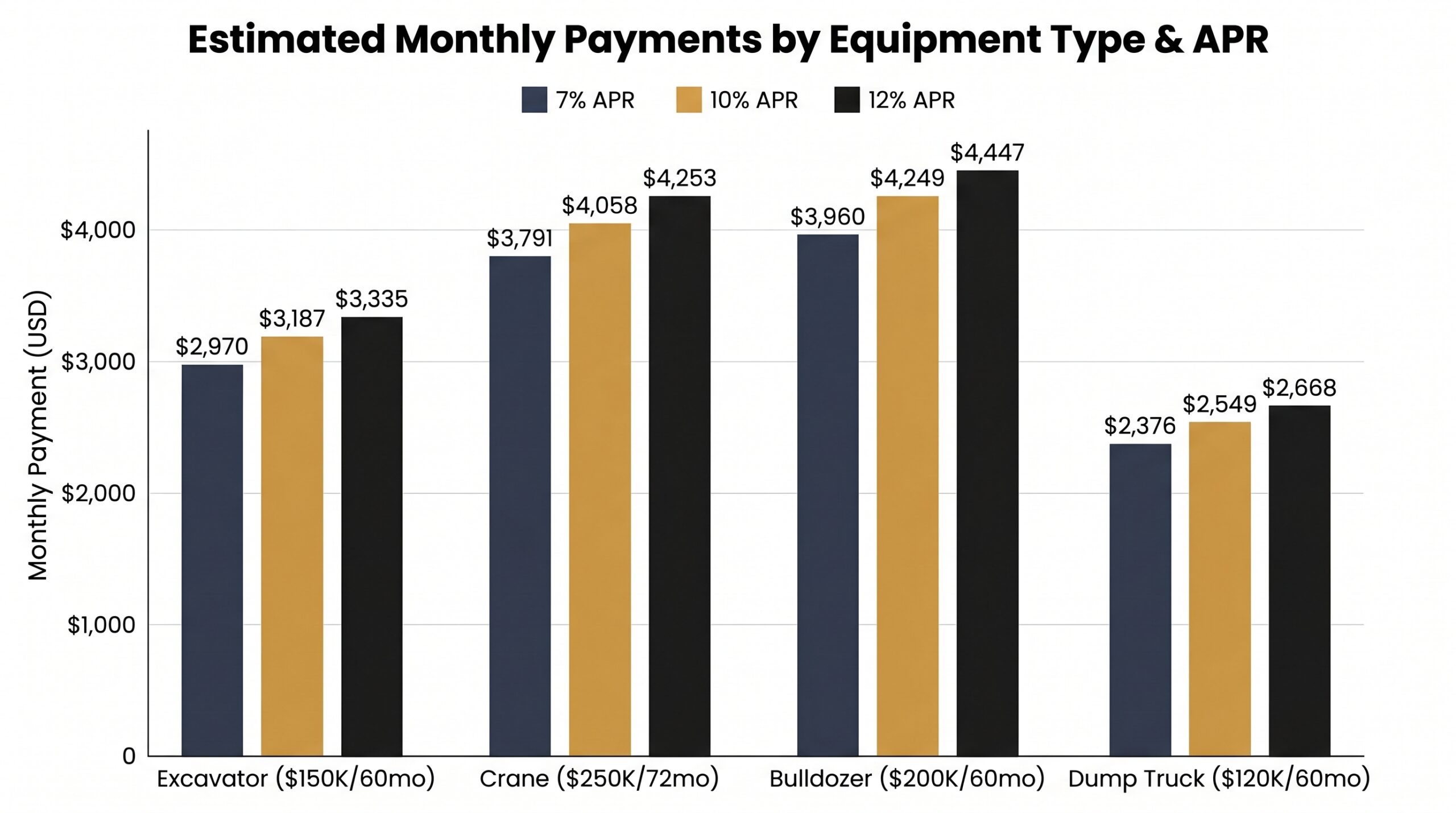

Real Cost Examples: What Heavy Equipment Financing Actually Costs

Most guides skip the numbers. Here’s what financing for heavy equipment actually looks like on a monthly basis across four common machine types.

Excavator Financing Example

Purchase price: $150,000 | Term: 60 months

| APR | Est. Monthly Payment |

|---|---|

| 7% | $2,970 |

| 10% | $3,187 |

| 12% | $3,335 |

Crane Financing Example

Purchase price: $250,000 | Term: 72 months

| APR | Est. Monthly Payment |

|---|---|

| 7% | $3,791 |

| 10% | $4,058 |

| 12% | $4,253 |

Bulldozer Financing Example

Purchase price: $200,000 | Term: 60 months

| APR | Est. Monthly Payment |

|---|---|

| 7% | $3,960 |

| 10% | $4,249 |

| 12% | $4,447 |

Dump Truck Financing Example

Purchase price: $120,000 | Term: 60 months

| APR | Est. Monthly Payment |

|---|---|

| 7% | $2,376 |

| 10% | $2,549 |

| 12% | $2,668 |

These figures assume no down payment and a fixed rate. Your actual payment depends on credit profile, down payment, and lender terms. Use the equipment financing payment calculator to model your specific scenario.

Loan Terms, Payment Structures & Repayment Options

Heavy equipment financing isn’t one-size-fits-all. Several repayment structures exist specifically for construction cash flow patterns.

Standard Term Lengths

Terms run 24 to 84 months. Most heavy construction equipment financing falls in the 60 to 84 month range, long enough to keep monthly payments manageable on six-figure machines without stretching beyond the equipment’s useful life.

Seasonal Payment Schedules

This is where construction financing gets useful. Many lenders offer reduced or skipped payments during Q4 and Q1, the slow season for most contractors. You pay more in spring and summer when project revenue is flowing. Not every lender offers this, so ask directly during the application process.

Balloon Payment Programs

Balloon structures lower your monthly payment throughout the term with a larger lump-sum due at the end. It works well if you’re expecting a major contract payout or plan to sell the equipment before the balloon comes due. The risk is obvious, you need that cash ready.

Deferred Payment Options

Some lenders offer 60 to 90 days before your first payment is due. For financing construction equipment on a new project, that buffer lets the machine start generating revenue before you’re making payments, a practical advantage worth asking about when comparing offers.

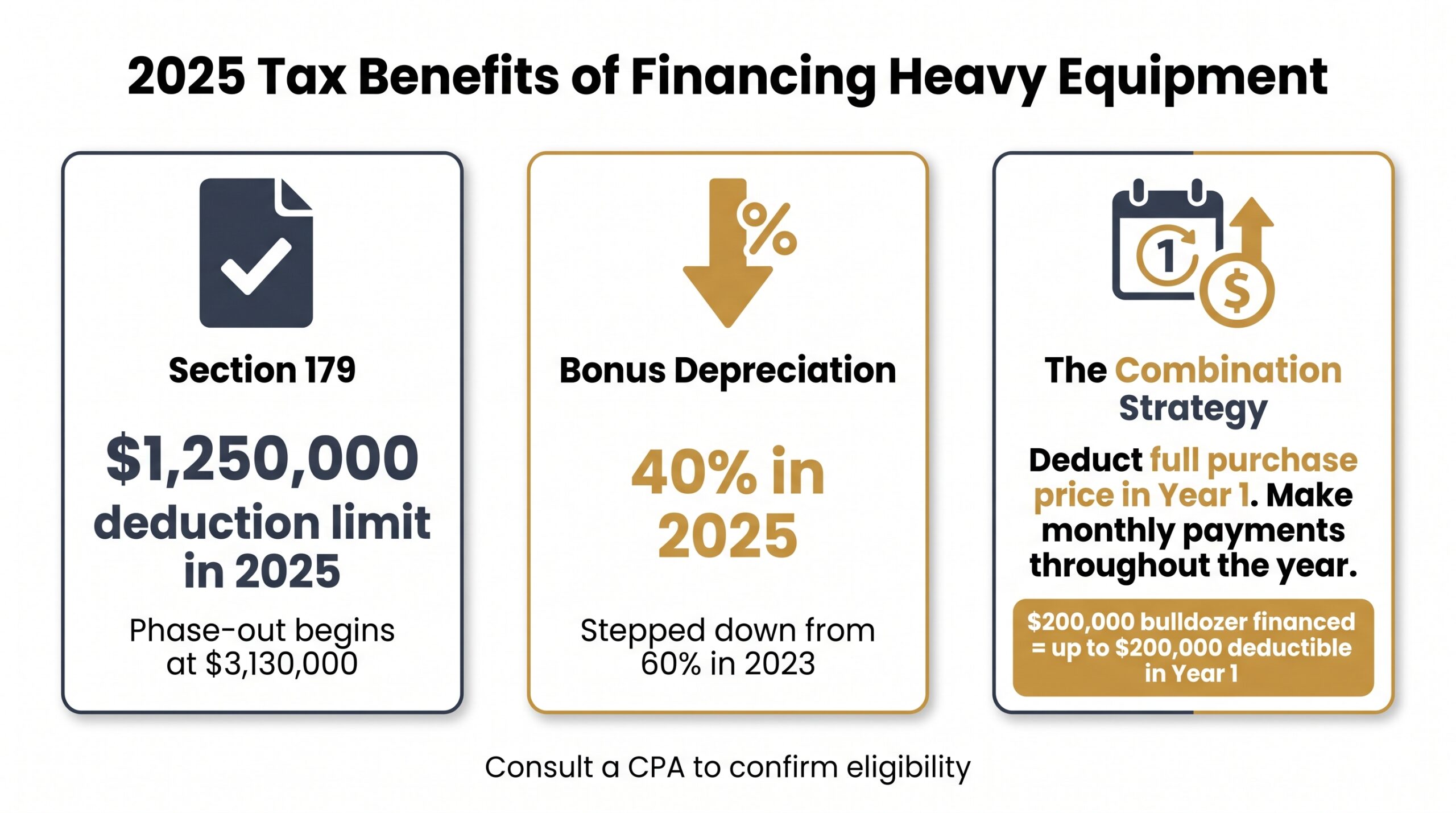

Tax Benefits of Financing Heavy Equipment (Section 179 & Bonus Depreciation)

Financing construction equipment doesn’t just preserve cash; it can generate a significant tax advantage in the same year you put the machine to work.

Section 179 Deduction for Heavy Equipment

The 2025 Section 179 deduction limit is $1,250,000, with the phase-out beginning at $3,130,000 of total qualifying property placed in service, per the IRS Instructions for Form 4562. Equipment must be used more than 50% for business purposes and placed in service during the tax year.

Bonus Depreciation in 2025

Bonus depreciation drops to 40% in 2025, down from 60% in 2023. It applies to new and used qualifying equipment and stacks with Section 179 for contractors with large purchases.

How Financing Preserves Your Tax Benefit

Here’s the combination that makes heavy equipment financing genuinely powerful: you can deduct the full purchase price in Year 1 under Section 179 while only making monthly payments throughout the year. You get the entire tax deduction immediately without paying the full purchase price upfront, cutting your tax bill while keeping cash in the business.

A $200,000 bulldozer financed at 7% over 60 months costs roughly $3,960 per month. But the full $200,000 may be deductible in Year 1. Consult a CPA to confirm eligibility for your specific situation.

Industry-Specific Heavy Equipment Financing Programs

Not all heavy equipment financing programs are built the same. Several industries have specialized options worth knowing about.

Construction and Contracting

Construction contractors can access milestone-based financing structures where draws align with project phases. Manufacturer programs like Cat Financial and Komatsu Financial understand construction cycles and offer seasonal payment flexibility that generic lenders don’t. SBA 504 loans are also a strong fit for contractors buying equipment above $500,000.

Mining and Quarrying

Mining operations typically run equipment harder and longer than construction sites. Specialized lenders in this space are comfortable with high machine hours and remote deployment scenarios that would disqualify equipment at a standard lender. Expect stricter appraisal requirements and shorter terms on high-hour machines.

Agriculture and Forestry

Agriculture has some of the most competitive financing rates available. USDA Farm Service Agency loans and AgDirect programs offer rates as low as 3.75% to 5.75% for qualifying borrowers. Forestry equipment often qualifies under the same agricultural programs. See our full guide on agricultural equipment financing for details.

Oil and Gas

Oil and gas operations typically work with captive lenders tied to specific equipment manufacturers or specialized commercial lenders familiar with the sector’s revenue volatility. Financing heavy equipment in this space often requires stronger cash flow documentation given the commodity-price sensitivity of the industry.

Risks to Consider Before Financing Heavy Equipment

Heavy equipment financing works well when the machine generates revenue. It gets painful when it doesn’t. Here are three risks worth understanding before you sign.

Repossession Risk

The equipment is the collateral. Miss enough payments, and the lender repossesses and sells it. If the resale value is below your remaining loan balance (which happens more often than buyers expect), you still owe the difference. That deficiency balance doesn’t disappear with the machine.

Depreciation and Negative Equity

Heavy construction equipment depreciates sharply in the first one to three years. Financing 100% with no down payment means you’re likely underwater immediately. If you need to sell early, due to a lost contract or a business pivot, you could owe more than the machine is worth.

Overfinancing Soft Costs

Rolling shipping, attachments, and extended warranties into your financing for heavy equipment feels convenient upfront. But every dollar added to the loan balance generates interest over the full term and accelerates negative equity. Keep soft costs out of the loan where possible, pay them separately, or negotiate them out of the deal entirely.

How to Apply for Heavy Equipment Financing

The application process is straightforward. Getting your documents ready before you start saves time and speeds up approval.

Documents You’ll Need

- Business license and EIN/tax ID

- Equipment invoice or dealer quote

- 3 to 6 months of business bank statements

- Most recent business tax return (typically required for loans over $150,000)

- Driver’s license for personal guarantee

The Application Process

Alternative lenders use a simple one-page online application. Decisions on heavy equipment financing under $250,000 can come back in 2 to 4 hours. Banks move more slowly, expect 1 to 3 weeks for full underwriting.

Nanotom Capital‘s application takes minutes and gets you a decision fast without unnecessary back-and-forth.

What Happens After Approval

You review and sign the financing agreement, the lender pays the dealer directly, and the equipment is delivered. Payments begin per your agreed schedule. Know what you’re signing.

Read our guide on what to look for in an equipment financing agreement before you commit.

Frequently Asked Questions About Heavy Equipment Financing

Can I get a loan for heavy equipment?

Yes. Heavy equipment financing is widely available through banks, alternative lenders, and manufacturer programs like Cat Financial. Because the equipment serves as collateral, it’s more accessible than unsecured business loans, even for borrowers with average credit or limited business history.

What credit score do I need to finance heavy equipment?

Most lenders want 600 to 650 minimum. Some alternative lenders will go down to 500 to 575 with a larger down payment and strong business revenue. Banks typically require 680 or higher for the best rates on heavy construction equipment financing.

How hard is it to get a loan for an excavator?

Moderately straightforward. If you have 600+ credit, two or more years in business, and a dealer quote in hand, alternative lenders can approve financing for construction equipment in as little as 24 hours. Banks take longer but may offer better rates for well-qualified borrowers.

How hard is it to get a $1,000,000 business loan for heavy equipment?

It’s achievable but requires stronger documentation. Expect lenders to want 680+ credit, two or more years in business, full financial statements, and sometimes a formal business review. Approval timelines run one to three weeks at this level. SBA 504 loans are worth considering for purchases in this range.

Can I finance heavy equipment with bad credit?

Yes, but the terms reflect the risk. Bad credit borrowers typically need a 20% to 50% down payment and should expect higher interest rates. Equipment condition matters more at this tier; newer, lower-hour machines are easier to approve. Some alternative lenders specialize in this space.

Does financing heavy equipment require a down payment?

Not always. Well-qualified borrowers with strong credit and established business history can access 0% down financing. For most borrowers, 10% to 20% down is typical. A larger down payment lowers your monthly payment, reduces your interest paid, and helps avoid negative equity on depreciating equipment.

How long can you finance heavy equipment?

Terms range from 24 to 84 months. The most common range for heavy construction equipment financing is 60 to 84 months, balancing manageable monthly payments with the equipment’s useful working life. Shorter terms mean higher payments but less total interest paid over the life of the loan.

Ready to move forward? Nanotom Capital specializes in financing for heavy equipment across construction, mining, agriculture, and more. Whether you’re buying your first excavator or expanding a fleet, we’ll match you with the right structure for your cash flow and credit profile.

Founder of Nanotom Capital & Nanotom Labs