Key Takeaways

- 82% of U.S. businesses use some form of financing when acquiring equipment; spreading payments over 12 to 84 months while the equipment itself serves as collateral.

- Credit score requirements start at 550 for alternative lenders, 620 for most equipment-specific lenders, and 680+ for banks and SBA programs; a low score doesn’t automatically disqualify you if revenue and collateral are strong.

- SBA 504 loans offer fixed rates of 6.51–6.64% on amounts up to $5.5M, while online lenders charge 10–45% APR in exchange for approvals as fast as 24 hours.

- Financed equipment qualifies for the full Section 179 deduction (up to $2,500,000 in 2025) in the year it’s placed in service; you don’t need to pay cash to claim it.

- Blanket liens cover all business assets including inventory and receivables, not just the financed equipment; always confirm whether the UCC-1 filing is equipment-specific before signing.

- A $150,000 equipment purchase financed at ~$2,800/month keeps the full $150,000 working as operating capital instead of draining reserves in a single transaction.

- Prepayment penalties can run 1–5% of the remaining balance, or require full-term interest regardless of early payoff; negotiate this term before committing to any agreement.

Buying equipment outright drains cash fast. Most businesses simply can’t afford to do it, and honestly, even the ones that can often shouldn’t. Business equipment financing lets you get the tools you need now and pay over time, preserving working capital for everything else.

This guide breaks down every financing path by company size, compares lenders transparently, and flags the risks most lenders won’t mention.

What Is Business Equipment Financing?

Business equipment financing is a loan or lease that lets companies acquire equipment, vehicles, or software by spreading payments over time instead of paying the full cost upfront. The equipment itself typically serves as collateral, which makes qualifying easier than with most traditional loans.

Repayment runs in fixed monthly installments over terms of 12 to 84 months. At the end of the term, you own the equipment outright.

It’s more common than most people realize. According to the Equipment Leasing and Finance Association, 82% of U.S. businesses use some form of financing when acquiring equipment. If you’re new to how it works, start with what equipment financing is before diving into lender comparisons.

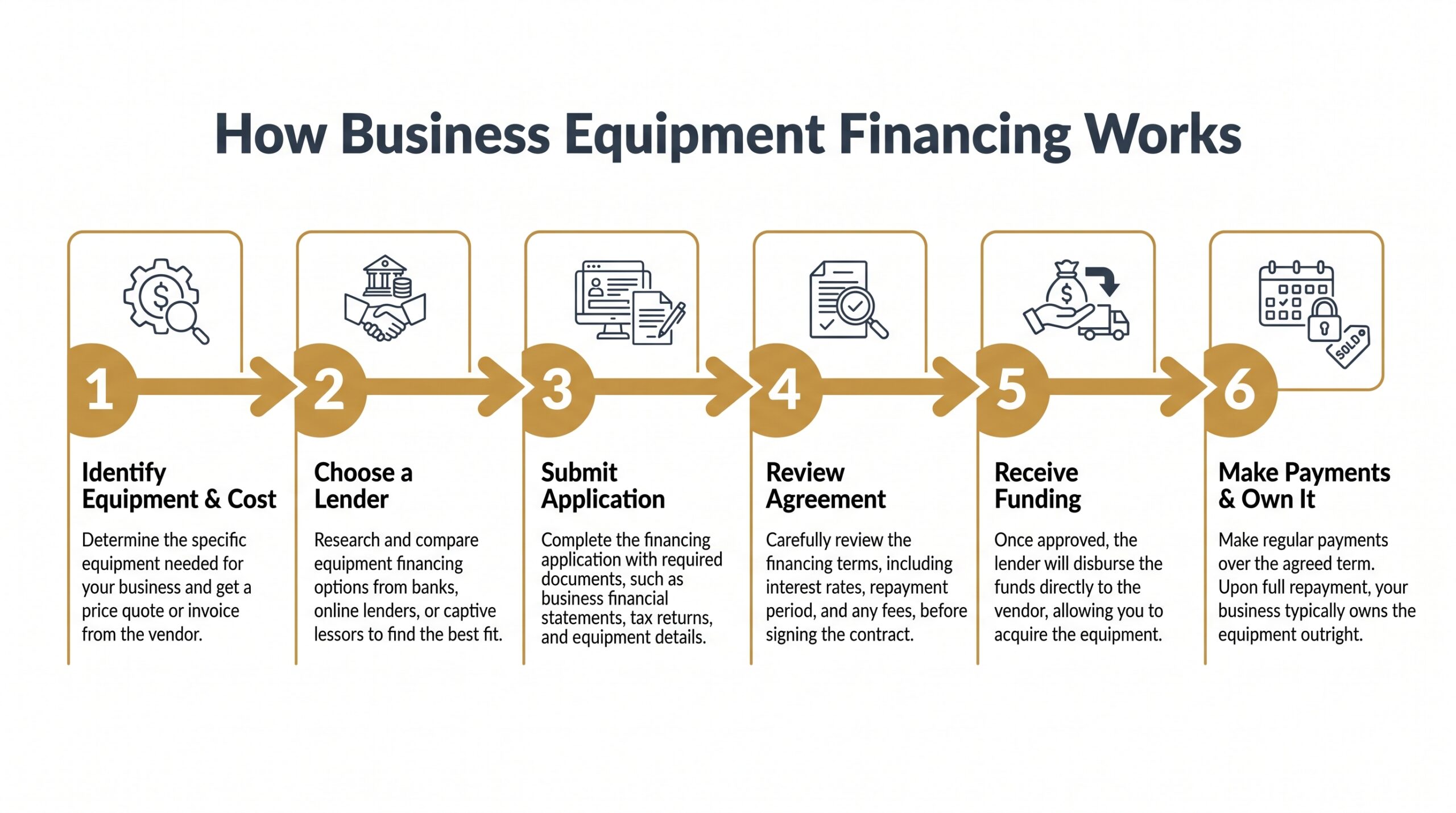

How Does Business Equipment Financing Work?

The process is more straightforward than most people expect. Here’s how business equipment financing works from start to finish.

Step 1: Identify the Equipment and Total Cost

Get a vendor quote. Know exactly what you’re financing, including installation or delivery fees if applicable.

Step 2: Choose a Lender or Financing Program

Banks, online lenders, SBA programs, and vendor financing all offer equipment financing for businesses. Each has different rates, terms, and qualification thresholds.

Step 3: Submit Your Application and Documentation

Expect to provide bank statements, tax returns, a vendor invoice, and basic business information. Some lenders approve equipment under $150,000 with minimal paperwork.

Step 4: Get Approved and Review Your Agreement

Read every line of your equipment financing agreement before signing. Watch for blanket liens, prepayment penalties, and whether soft costs like installation are included.

Step 5: Receive Funding and Take Possession of Equipment

Many lenders fund same-day or within 24 to 48 hours for straightforward applications. The lender pays the vendor directly in most cases.

Step 6: Make Fixed Monthly Payments and Own the Equipment

You repay in fixed installments over your agreed term. Once the final payment clears, the equipment is yours free and clear.

Types of Business Equipment You Can Finance

Almost any tangible business asset qualifies. Both new and used equipment typically meet lender requirements, and soft costs like delivery, installation, and training can often be bundled into the total financing amount.

Common equipment categories include:

- Construction: Excavators, cranes, dozers, and heavy machinery. See our guide to construction equipment financing for specifics.

- Healthcare: MRI systems, diagnostic tools, dental chairs, and imaging devices. Medical equipment financing has unique program structures worth knowing.

- Manufacturing: CNC machines, robotics, and assembly line systems.

- Restaurant and food service: Commercial ovens, refrigeration units, and POS systems.

- Transportation: Semi-trucks, delivery vans, and full fleet packages.

- Technology: Servers, computers, and software licenses.

- Agriculture: Tractors, combines, and irrigation systems.

- General office: Copiers, HVAC systems, and security equipment.

If your business uses it to generate revenue, there’s likely a financing program built around it.

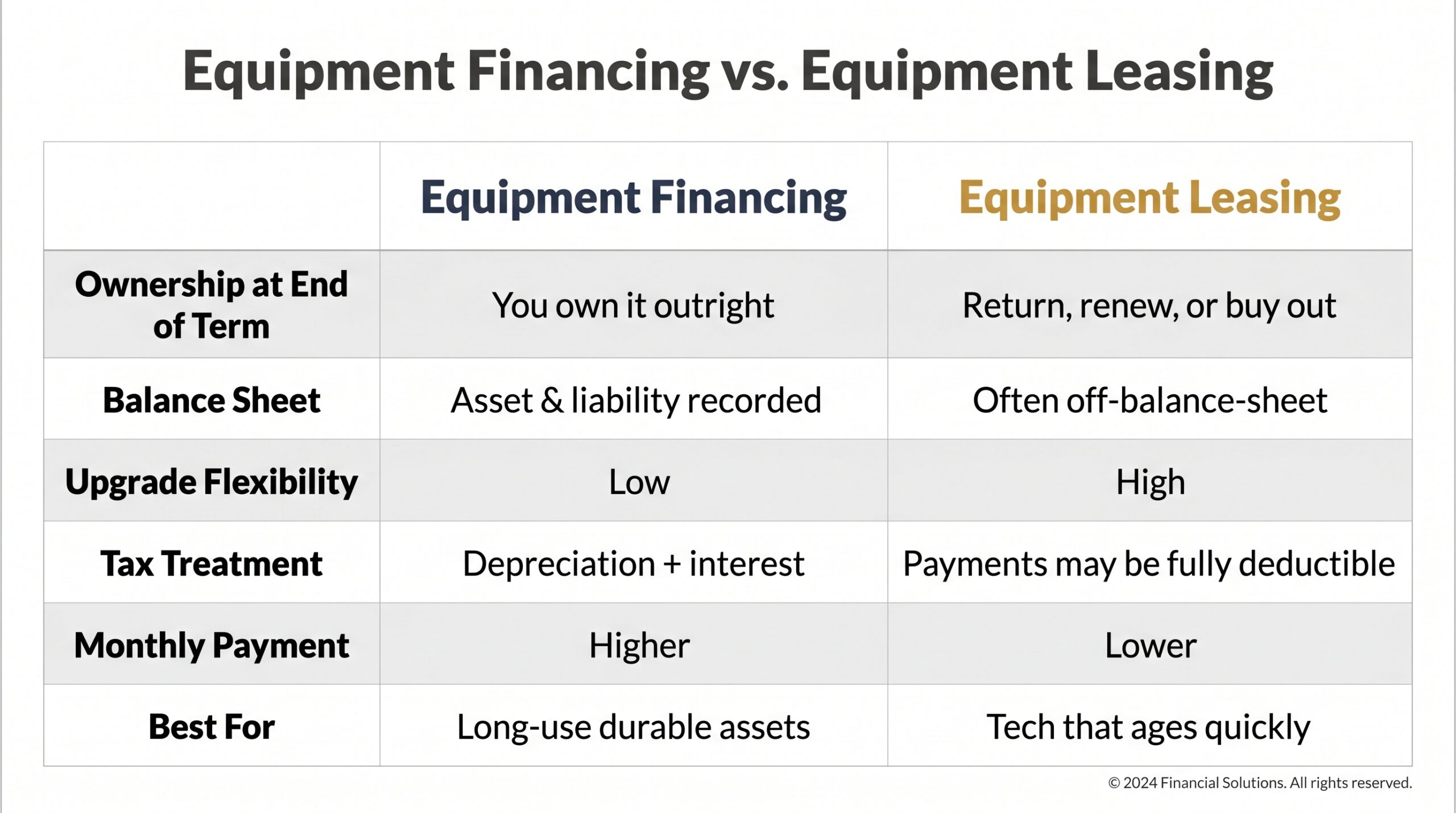

Equipment Financing vs. Equipment Leasing: Key Differences

Financing and leasing both spread costs over time, but they’re structured very differently. The right choice comes down to one question: do you want to own the asset, or do you need the flexibility to walk away?

| Factor | Equipment Financing | Equipment Leasing |

|---|---|---|

| Ownership at end of term | You own it outright | Return, renew, or buy out |

| Balance sheet treatment | Asset and liability recorded | Often kept off-balance-sheet |

| Flexibility to upgrade | Low | High |

| Tax treatment | Depreciation + interest deduction | Payments may be fully deductible |

| Monthly payment | Higher | Lower |

| Best for | Long-use, appreciating assets | Tech or equipment that ages quickly |

Business equipment financing makes sense when you plan to use the asset for years and want to build equity. Leasing wins when you need the latest technology every few years without being stuck with outdated hardware.

For a deeper breakdown, read our guide on equipment leasing vs. financing.

Best Business Equipment Financing Options by Company Size

Here’s what most financing guides get wrong: they treat every business the same. Your options, rates, and requirements shift significantly depending on where your company actually stands.

Equipment Financing for Startups and New Businesses

Under a year in business? Traditional lenders will likely pass. Your best paths are vendor financing programs, startup-friendly online lenders, and alternative underwriting based on personal credit and cash flow.

Expect down payment requirements of 10 to 20% and rates that reflect the higher risk. Only about 46% of the smallest firms use financing at all, mostly because they don’t know options exist. See our full guide on startup equipment financing.

Equipment Financing for Small Businesses

One to five years in business with under $5M in revenue puts you in the broadest lending pool. SBA 7(a) and 504 loans offer competitive rates with longer terms. Online equipment lenders move faster and require $50,000 to $250,000 in annual revenue with a credit score of 620 or better. Small business equipment financing is genuinely competitive at this stage.

Equipment Financing for Mid-Size and Enterprise Companies

Above $5M in revenue, bank financing becomes accessible with rates typically ranging from 4 to 10%. Loan amounts scale significantly, and private equipment finance companies offer customized structures. Watch for blanket liens in large agreements, and negotiate prepayment terms before signing anything.

How to Qualify for Business Equipment Financing

Qualification requirements vary more than most lenders advertise. Here’s what actually moves the needle.

Credit Score Requirements

Banks prefer 650 to 700+. Most equipment-specific lenders accept 620+. Alternative lenders may approve scores as low as 550 to 600.

A low score doesn’t automatically disqualify you. Strong monthly revenue, a larger down payment, or high-value collateral can offset credit weaknesses. For low-credit options specifically, see equipment financing with no credit check.

Time in Business Requirements

Traditional lenders typically want two or more years of operating history. Online and alternative lenders often accept six to twelve months. Startups may still qualify using personal credit and a solid down payment.

Revenue and Financial Documentation

Most lenders set minimum annual revenue thresholds between $50,000 and $250,000. Prepare these documents before applying:

- Business tax returns (last 2 years)

- Bank statements (3 to 6 months)

- Equipment invoice or vendor quote

- Business license

- Personal credit authorization

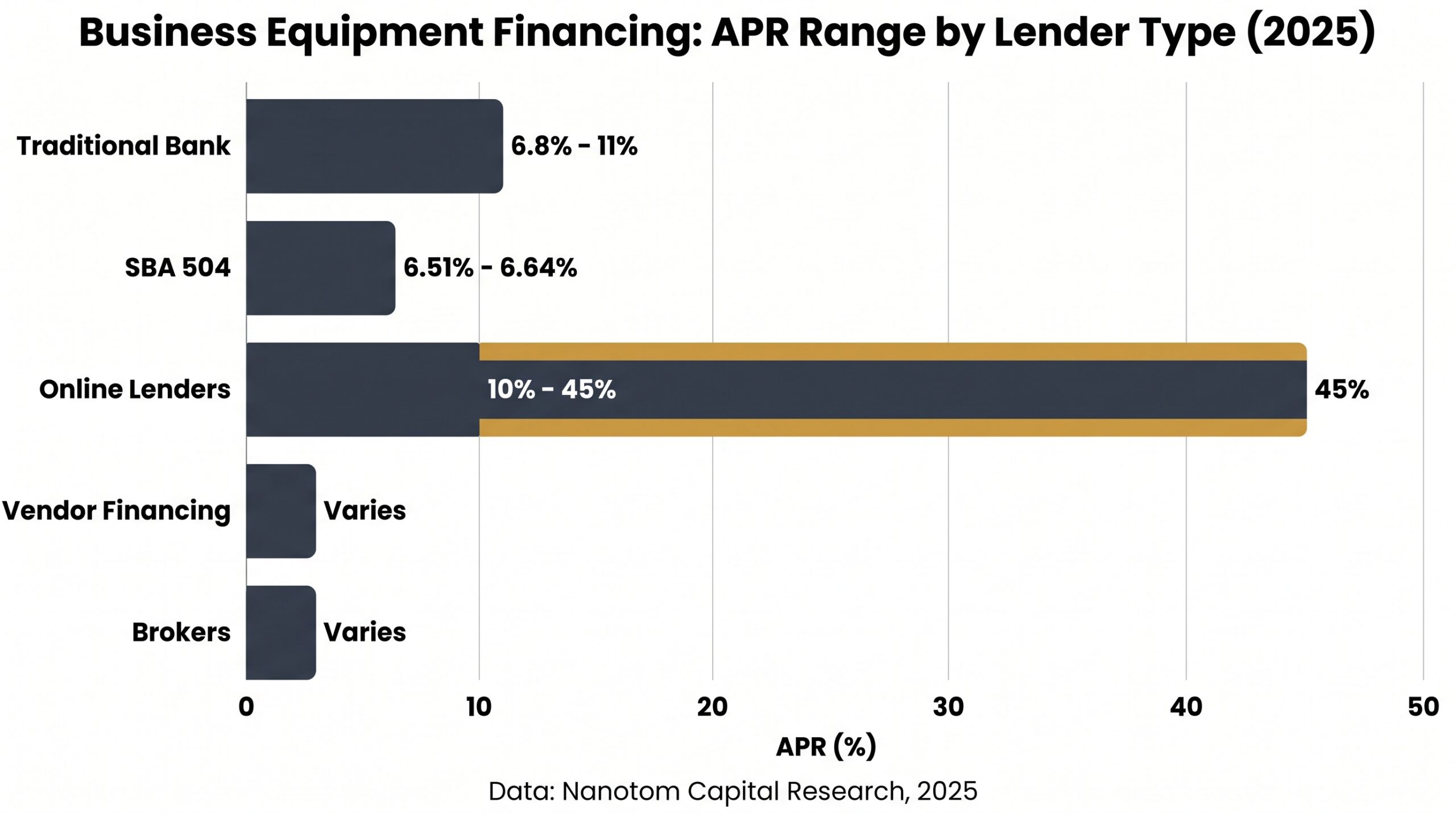

Business Equipment Financing Options Compared

Not all lenders are built the same. Here’s how every major financing path stacks up.

| Lender Type | Typical APR | Loan Amounts | Min Credit Score | Time in Business | Funding Speed | Best For |

|---|---|---|---|---|---|---|

| Traditional Bank | 6.8–11% | $50K–$5M+ | 680+ | 2 years | 1–4 weeks | Established businesses |

| SBA 504 | 6.51–6.64% (CDC portion) | Up to $5.5M | 680+ | 2 years | 30–90 days | Large long-term acquisitions |

| Online Lenders | 10–45% | $5K–$2M | 550–620+ | 6–12 months | 24 hours–1 week | Speed and flexibility |

| Vendor Financing | Varies, promotional rates possible | Tied to purchase | Varies | Flexible | Fastest | Buying direct from manufacturer |

| Brokers | Varies | All sizes | All types | Varies | Fast matching | Complex or declined applications |

Traditional Bank Equipment Loans

Banks offer the lowest rates but the strictest requirements. Plan for a multi-week underwriting process and strong financials.

SBA 504 and SBA 7(a) Equipment Loans

SBA programs offer exceptional rates and terms for qualifying businesses. According to the SBA, the 504 loan program provides fixed-rate financing at 6.51–6.64% on the CDC portion for 2025. The tradeoff is time, 30 to 90 days from application to funding is common.

Online Equipment Lenders

Speed is the primary advantage. Many online lenders approve equipment financing for small businesses within 24 hours, though rates run higher to offset the risk.

Vendor Financing Programs

Buying directly from a manufacturer or dealer often unlocks promotional financing rates. It’s seamless and fast, but you’re not rate shopping, which can cost you more than you’d expect.

Equipment Financing Brokers

If you’ve been declined or need specialized equipment, brokers connect you to multiple lenders simultaneously. Learn more in our guide to equipment financing brokers, or compare top lenders directly at best equipment financing companies.

Business Equipment Financing Rates and Terms to Expect

Rates range from 4% to 45% APR in 2025. Where you land depends entirely on your lender type and borrower profile.

| Lender Type | Typical APR Range | Typical Terms |

|---|---|---|

| Traditional Bank | 6.8–11% | 24–84 months |

| SBA 504 | 6.51–6.64% (fixed) | Up to 10 years |

| Online Lenders | 10–45% | 12–60 months |

Fixed rates offer payment predictability and protect you from rate increases. Variable rates may start lower but carry real cost risk on terms beyond three years.

Key factors that move your rate up or down:

- Credit score

- Time in business

- New vs. used equipment

- Down payment size

- Loan term length

Watch for prepayment penalties. Some lenders charge 1 to 5% of the remaining balance, or require full-term interest regardless of early payoff. Ask about this before you sign anything, it’s one of the terms most borrowers don’t think to negotiate until it’s too late.

Use our equipment financing calculator to model payments, and see our full breakdown of equipment financing rates to understand what drives your number.

Benefits of Financing Business Equipment Instead of Paying Cash

Even if you have the cash on hand, financing business equipment often makes more financial sense. The honest answer is that preserving liquidity is usually worth more than the interest you’d save by paying outright.

A $150,000 piece of equipment financed at roughly $2,800 per month keeps $150,000 working in your business. That cash covers payroll, inventory, or the next growth opportunity. Draining reserves for a single asset purchase is a real operational risk, one that shows up fast when an unexpected expense hits.

The case for equipment financing goes beyond cash flow:

- Predictable budgeting: Fixed monthly payments are easy to plan around.

- Self-liquidating asset: The equipment generates revenue while you’re still paying for it.

- Inflation protection: You lock in today’s equipment price and repay with cheaper future dollars.

- Speed: Financing lets you act on a contract or growth opportunity immediately.

- Business credit building: Consistent payments strengthen your borrowing profile.

- Preserves credit lines: Business equipment financing doesn’t touch your existing bank line of credit the way a large cash withdrawal does.

Cash isn’t always king. Sometimes it’s the most expensive option you have.

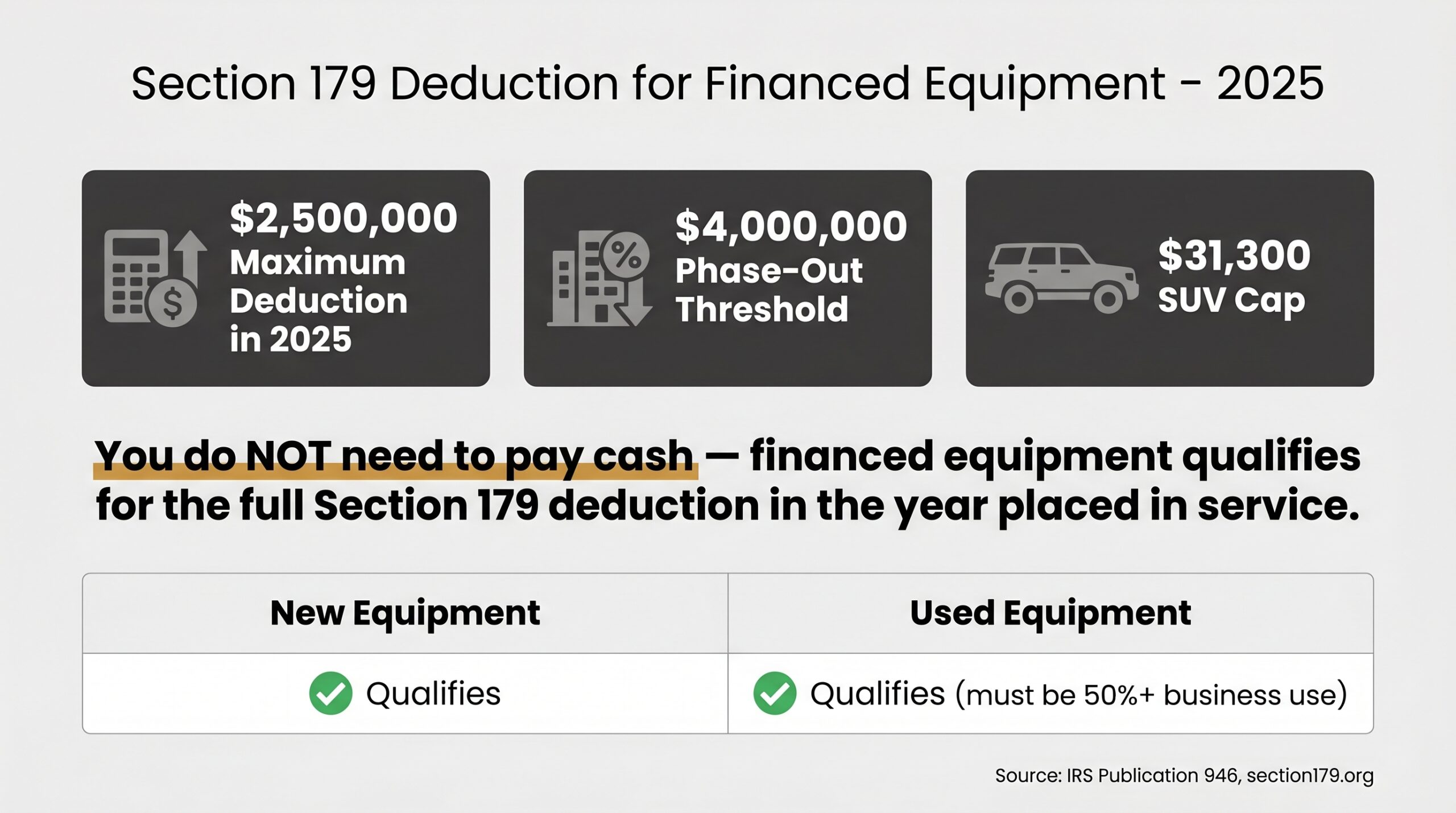

Tax Advantages of Business Equipment Financing (Section 179 & Bonus Depreciation)

Here’s what most guides skip: financing your equipment doesn’t just preserve cash, it can also deliver a significant tax deduction in the same year you acquire the asset.

Section 179 for 2025: According to IRS Publication 946, businesses can deduct up to $2,500,000 in qualifying equipment purchases. The phase-out begins at $4,000,000 in total purchases. This applies to both new and used equipment used more than 50% for business purposes.

The detail most businesses miss is this: you don’t need to pay cash to claim the deduction. Financed equipment qualifies for the full Section 179 deduction in the year it’s placed in service. You can preserve working capital and still write off the full purchase price.

If you’re financing vehicles, note the SUV cap of $31,300 for 2025.

Bonus depreciation is still available but phasing down following the Tax Cuts and Jobs Act. It’s worth modeling both strategies with your tax advisor before finalizing any equipment financing for your business.

Sources: IRS Publication 946, section179.org. Tax laws change, always verify with a qualified tax professional.

Important Terms to Watch in an Equipment Financing Agreement

The rate isn’t the only thing that matters. Certain contract terms can cost you far more than a higher APR ever would. Always review your equipment financing agreement carefully before signing.

Blanket Liens vs. Equipment-Only UCC Filings

A UCC-1 filing tied to the financed equipment is standard and expected. A blanket lien is a different animal. It covers all your business assets, including inventory, accounts receivable, and bank accounts, which can block you from securing future financing with other lenders.

Always ask directly: Is this lien equipment-specific or blanket?

Prepayment Penalties

Some lenders charge 1 to 5% of the remaining balance if you pay early. Others require full-term interest regardless. Ask about this before you commit to any business equipment financing agreement; don’t wait until you’re reviewing the final paperwork.

Soft Cost Coverage

Delivery, installation, training, and extended warranties can often be bundled into your financed amount. This reduces your upfront cash requirement further and is one of the underused advantages of financing equipment for small business purchases.

How to Apply for Business Equipment Financing

For amounts under $250,000, many online lenders offer same-day or 24 to 48-hour approvals. The application itself is usually simpler than people expect. Here’s the full sequence:

- Get a vendor quote or invoice. Most lenders require this before approving equipment financing for your business.

- Gather your documentation. Tax returns, bank statements, and business license. Have these ready before you start applications.

- Compare lenders or use a broker. Don’t apply to one and stop. Rate shopping protects you.

- Submit your application. Many online lenders use a single-page application for small business equipment financing requests.

- Review the agreement carefully. Check for blanket liens and prepayment penalties before you sign.

- Lender funds the purchase. Payment typically goes directly to the vendor.

- Begin payments and track for Section 179. Document the in-service date for your tax filing.

For a deeper walkthrough, see how to get a loan for any business equipment.

Industry-Specific Equipment Financing Use Cases

Equipment financing looks different depending on your industry. The amounts, structures, and lender preferences all shift. Here’s how it plays out in practice.

Construction and Heavy Equipment

Construction end-users finance equipment at an 85% rate according to ELFA data. An excavator or crane costing $400,000 financed over 60 months keeps a contractor bidding on new projects without tying up bonding capacity. See our guide to heavy construction equipment financing.

Healthcare and Medical Practices

Medical equipment is financed at 84% of acquisition volume, and it’s easy to see why. An MRI or CT scanner can run $1M to $3M. Financing spreads that cost while the equipment generates billable procedures from day one. Full breakdown: medical and dental equipment financing.

Manufacturing and Industrial

Industrial and manufacturing businesses finance at roughly 78% of acquisition volume. CNC machines, laser cutters, and production lines are capital-intensive assets that pay for themselves through output. Business equipment financing lets manufacturers upgrade without disrupting cash flow.

Restaurants and Food Service

Commercial kitchens require significant upfront investment in ovens, refrigeration, and exhaust systems. Financing spreads those costs across the revenue the kitchen generates, which is exactly how it should work. Learn more: restaurant equipment financing.

Transportation and Trucking

A single Class 8 truck runs $180,000 to $200,000 new. Fleet operators use business equipment financing to add trucks without draining reserves needed for fuel, insurance, and maintenance. Details: trucking equipment financing.

Frequently Asked Questions About Business Equipment Financing

Can I finance used equipment?

Yes. Most lenders finance used equipment, though rates may run slightly higher and some lenders require an independent appraisal to confirm value.

What credit score do I need for equipment financing?

Most lenders require a minimum score of 620. Alternative lenders approve at 550 and above. You’ll need 700 or higher to access the best rates on business equipment financing.

Can a startup get equipment financing?

Yes, with a strong personal credit score, a down payment, and a business plan. See our full guide to startup equipment financing for lender options built specifically for new businesses.

What is the maximum amount I can finance for equipment?

Most lenders cover $5,000 to $5 million or more. SBA 504 loans go higher for qualifying projects. The right ceiling depends on your revenue, credit, and time in business.

Does equipment financing require a down payment?

Not always. Equipment collateral often eliminates the down payment requirement. That said, putting 10 to 20% down typically improves both your approval odds and your rate.

Can I get equipment financing with bad credit?

Yes. Alternative lenders approve scores of 550 and above, and strong revenue can offset weak credit. Explore your options in our guide to equipment financing with no credit check.

How fast can I get approved for equipment financing?

Online lenders can approve same-day for amounts under $250,000. Traditional banks typically take one to four weeks depending on documentation requirements.

What happens at the end of an equipment financing term?

With a loan, you own the equipment outright once the final payment is made. With a lease, you’ll typically have the option to return, renew, or exercise a buyout.

Is equipment financing the same as an equipment lease?

No. Financing means you’re buying and building equity. Leasing means you’re renting with options at the end. The full breakdown is in our guide to equipment leasing vs. financing.

Business equipment financing is one of the most accessible and financially efficient tools available to companies at every stage. Whether you’re a startup funding your first piece of equipment or an enterprise managing a multi-million dollar fleet, the right structure exists for your situation. Compare your options, read every agreement, and don’t leave the Section 179 deduction on the table.

Founder of Nanotom Capital & Nanotom Labs