Key Takeaways

- Medical equipment financing spreads costs of $50,000 to $500,000+ over terms of 12 to 84 months, with interest rates of 5% to 15% for well-qualified borrowers and $0 down available through many lenders.

- A 650 credit score is the practical minimum for most lenders; hit 680+ and you unlock traditional bank and SBA programs with approval rates of 78–85%.

- Section 179 lets you deduct up to $2,500,000 in financed equipment in the year it’s placed in service, meaning a $200,000 imaging system financed over 60 months can still deliver a full year-one tax deduction.

- Startups face approval rates of only 25–35%, versus 70–82% for practices with two or more years of history; lenders compensate by weighing personal credit, professional credentials (MD/DDS), and equipment resale value.

- Leasing beats financing for fast-obsolescence technology like CBCT scanners and EMR hardware; financing wins for long-use assets like surgical tools and exam tables you’ll run for 10-plus years.

- Medicare does not fund equipment purchases by healthcare practices; Medicare Part B only covers durable medical equipment for patients in home settings.

- Online lenders approve medical equipment financing in 24–48 hours; traditional banks take one to three weeks, making online the faster path for time-sensitive equipment needs.

New or upgraded equipment can cost $50,000 to $500,000 or more. Most healthcare practices can’t, or simply shouldn’t, drain their cash reserves to cover that.

Medical equipment financing solves the problem by spreading the cost over time, and this guide covers everything you need to make a confident decision: exact credit score thresholds, sample payment calculations, startup options, and lender comparisons for both medical and dental practices.

What Is Medical Equipment Financing?

Medical equipment financing is a loan or lease arrangement that lets healthcare businesses purchase or use medical equipment by spreading the cost over time. Instead of paying the full price upfront, you make fixed monthly payments over a set term, typically 12 to 84 months, while the equipment itself often serves as collateral.

If you’re new to this type of funding, equipment financing basics are worth understanding before you compare lenders.

Healthcare is one of the most capital-intensive industries in the country. Technology cycles move fast. A CT scanner or digital imaging system that’s current today may be outdated in five years, and financing lets practices stay current without gutting the working capital they need for payroll, supplies, and day-to-day operations.

The U.S. medical equipment financing market was valued at approximately $44 billion in 2024, according to SNS Insider and Precedence Research estimates. This guide covers financing needs across both clinical and dental equipment financing.

How Does Medical Equipment Financing Work?

The Basic Loan Structure

A lender advances funds to purchase the equipment, and you repay in fixed monthly installments over an agreed term. The equipment itself serves as collateral, so you’re not pledging your building, personal assets, or other business property.

Interest rates typically run 5% to 15% for well-qualified borrowers. For a deeper look at how rates are set and how to get the best deal, see our guide on equipment financing rates. Standard terms are 24 to 60 months, though specialty healthcare lenders like Henry Schein Financial Services and Synovus offer up to 10 to 15 years for large diagnostic systems. Many programs also offer 100% financing with $0 down, which matters when you’re preserving cash for staff and supplies.

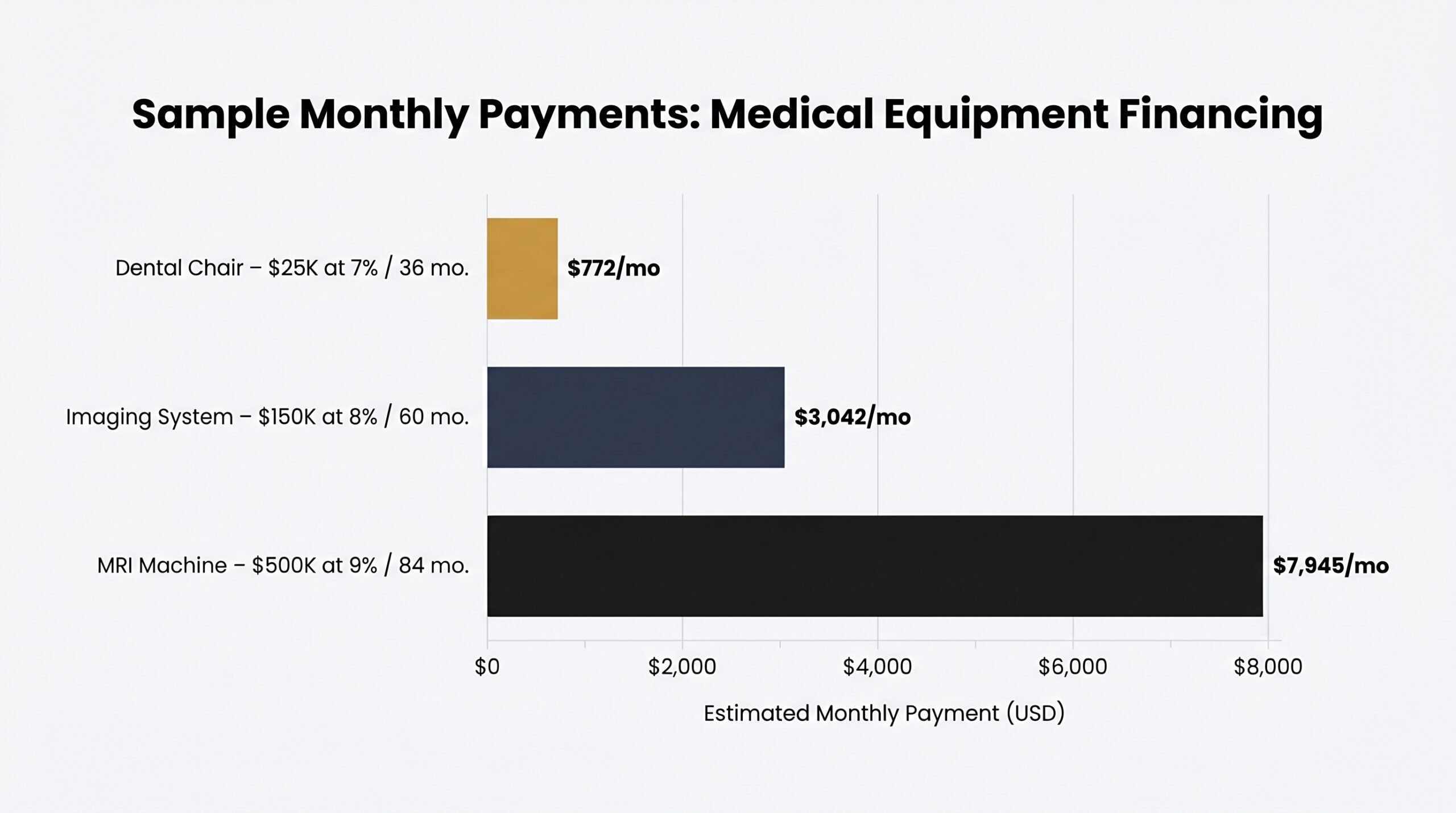

Sample Monthly Payment Calculations

These figures are approximate and assume good credit. Use an equipment financing calculator to get exact numbers for your scenario.

| Equipment | Amount | Rate | Term | Est. Monthly Payment |

|---|---|---|---|---|

| Dental chair | $25,000 | 7% | 36 months | ~$772 |

| Imaging system | $150,000 | 8% | 60 months | ~$3,042 |

| MRI machine | $500,000 | 9% | 84 months | ~$7,945 |

Types of Medical and Dental Equipment You Can Finance

Medical Equipment

Most lenders will finance virtually any revenue-generating clinical asset. MRI machines alone range from $150,000 for a refurbished unit to over $3 million for a new high-field system, which is exactly why medical equipment financing exists.

- MRI machines ($150K–$3M+)

- CT scanners and X-ray machines

- Ultrasound units

- Surgical tables and tools

- Patient monitoring systems

- Laboratory equipment

- Autoclave and sterilization units

- EHR/EMR hardware and point-of-care technology

- Ophthalmic equipment

- Physical therapy machines

- Exam tables and infusion pumps

Dental Equipment

Dental equipment financing covers everything from a single chair to a fully equipped operatory. Outfitting one operatory from scratch typically runs $30,000 to $75,000 or more, so even established practices routinely finance these purchases rather than pay out of pocket.

- Dental chairs ($2,000–$20,000+)

- Digital and panoramic X-ray units

- Intraoral cameras

- Cone beam CT scanners (CBCT)

- Autoclaves and sterilization units

- Dental drills and handpieces

- CAD/CAM milling machines (e.g., CEREC)

- Nitrous oxide delivery systems

- Suction units

- Practice management software and hardware

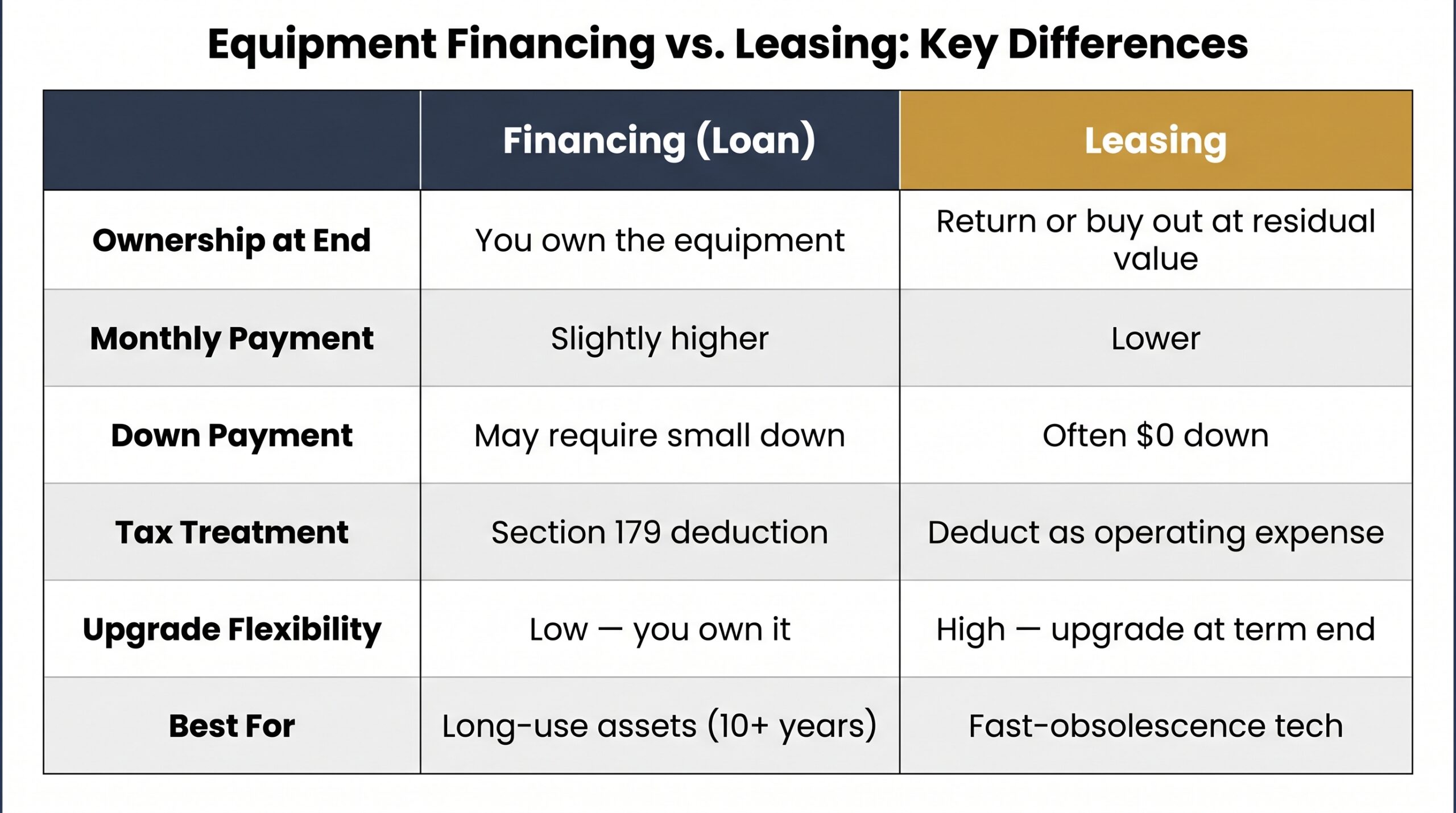

Medical Equipment Financing vs. Leasing: Key Differences

Both options spread your costs over time, but they work very differently. Here’s how they compare across the factors that matter most to healthcare practices.

| Factor | Financing (Loan) | Leasing |

|---|---|---|

| Ownership at end of term | You own the equipment | Return it or buy out at residual value |

| Monthly payment size | Slightly higher | Lower |

| Down payment | May require small down | Often $0 down |

| Tax treatment | Section 179 deduction on purchase price | Deduct lease payments as operating expense |

| Flexibility to upgrade | Low; you own it until you sell | High; upgrade at end of term |

| Best for | Long-use equipment (exam tables, surgical tools) | Technology that becomes obsolete quickly |

Choose financing for equipment you’ll run for 10-plus years. Leasing makes more sense for CBCT scanners, digital imaging systems, or EMR hardware where a newer model will meaningfully improve patient care or revenue within five years. See our full equipment leasing vs. financing breakdown for a deeper comparison.

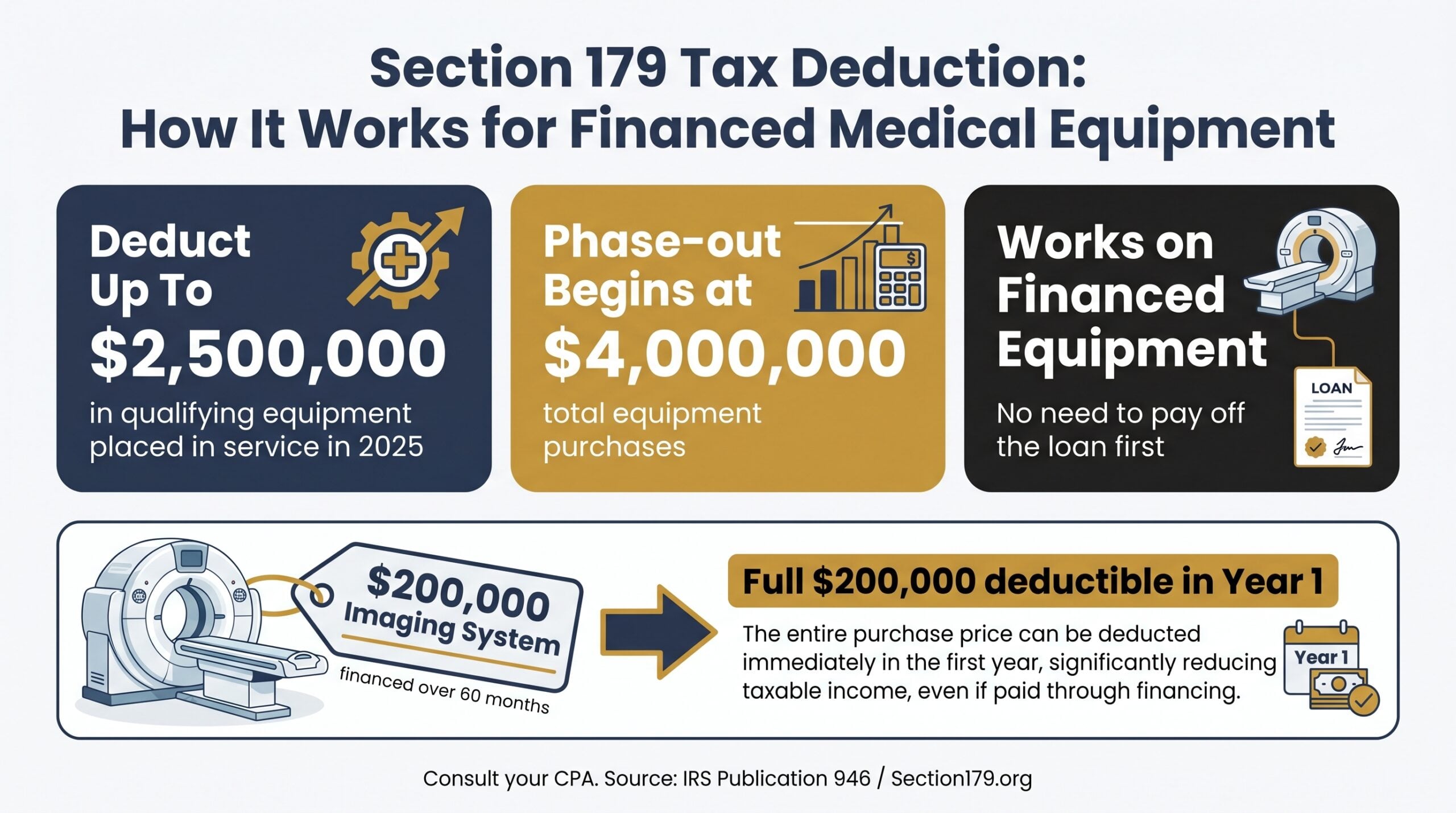

Tax Benefits of Financing Medical Equipment

Here’s what most guides skip: you can deduct the full purchase price of financed equipment in year one, even if you’re still paying off the loan. That’s not a loophole. It’s exactly how Section 179 is designed to work.

Under Section 179 of the IRS tax code, businesses can deduct up to $2,500,000 in qualifying equipment placed in service during the 2025 tax year, according to IRS Publication 946. The phase-out begins once total equipment purchases exceed $4,000,000. Critically, the deduction applies to financed equipment, not just outright purchases.

Real example: You finance a $200,000 imaging system and place it in service in 2025. You’re repaying it over 60 months, but you may still deduct the full $200,000 on your 2025 tax return, potentially offsetting a significant portion of your tax liability in year one.

Bonus depreciation may offer additional deductions depending on current IRS rules, though the percentage has been phasing down in recent years. See Section179.org for current bonus depreciation figures and qualifying property rules.

These advantages make financing significantly more cost-effective than the sticker price suggests. That said, every practice’s tax situation is different; consult your CPA before making decisions based on depreciation strategy.

How to Qualify for Medical Equipment Financing

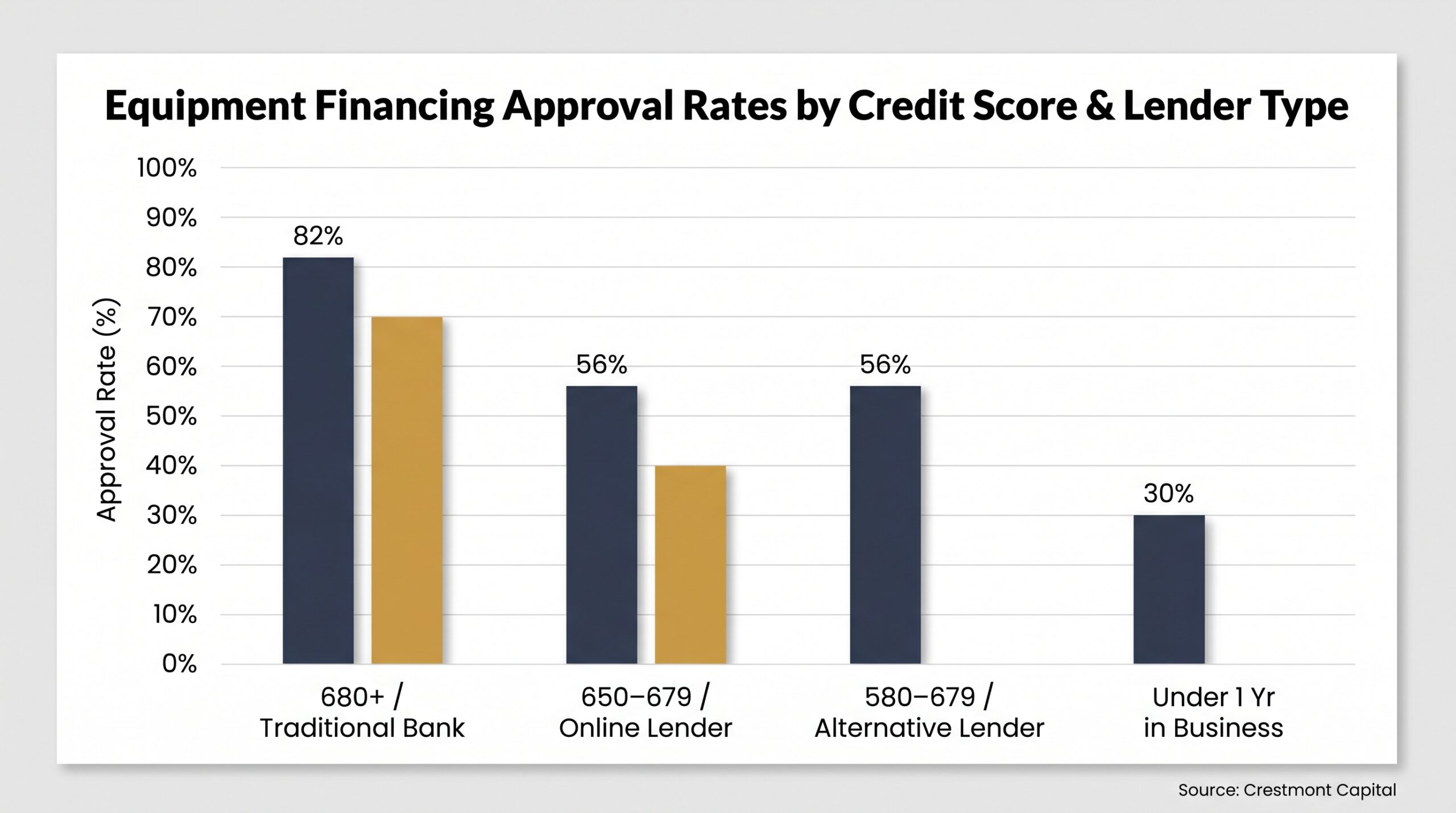

What Credit Score Do You Need?

Most lenders use 650 as the practical floor. Here’s how the tiers break down:

- 680+: Traditional banks and SBA-backed programs; 78–85% approval rates (Crestmont Capital)

- 650–679: Most online lenders and specialty healthcare financiers; 50–62% approval rates

- 600–649: Alternative lenders, often with stronger revenue requirements

- 520–550: Some specialty equipment financiers, typically requiring larger down payments or proven revenue

Other Qualification Requirements

Credit score isn’t the only factor. Most lenders also want to see:

- Time in business: 1–2 years minimum (some alternative lenders accept 6 months)

- Annual revenue: $50,000+ commonly required

- Last 2 years of business tax returns

- 3–6 months of bank statements

- Equipment invoice or vendor quote

- Business plan for startups or newer practices

Options If You Have Bad Credit

The honest answer is that medical equipment financing is more forgiving than most business loans, because the equipment itself secures the debt, lenders carry less risk. If your credit is thin or damaged, you still have real options.

Consider alternative online lenders with lower score minimums, offering a larger down payment, adding a creditworthy co-signer, or pursuing a lease instead of a loan. See our guide on equipment financing with no credit check for more low-barrier options.

Startup Medical and Dental Practice Financing

New practices can get medical equipment financing, but approval rates are lower. Practices under one year old see approval rates of roughly 25–35%, compared to 70–82% for practices with two or more years of operating history (Crestmont Capital). That gap is real, and it’s worth knowing before you apply.

Without revenue history, lenders shift their focus to other signals:

- Personal credit score (650+ is the practical minimum)

- Personal net worth and financial strength

- Professional credentials. Being a licensed MD or DDS carries real weight

- Equipment resale value (easier-to-resell assets reduce lender risk)

- A business plan with projected patient volume and revenue

Your best options as a startup practice include:

- Equipment leasing, which has a lower qualification bar than loans

- SBA 7(a) loans or SBA microloans

- Healthcare-specific startup lenders that underwrite on personal credit

- Manufacturer or dealer promotional financing (Henry Schein and similar vendors regularly offer 0–3.9% promotional rates)

- Personal guarantee to strengthen a borderline application

For a full breakdown of your options, see our guide on startup equipment financing.

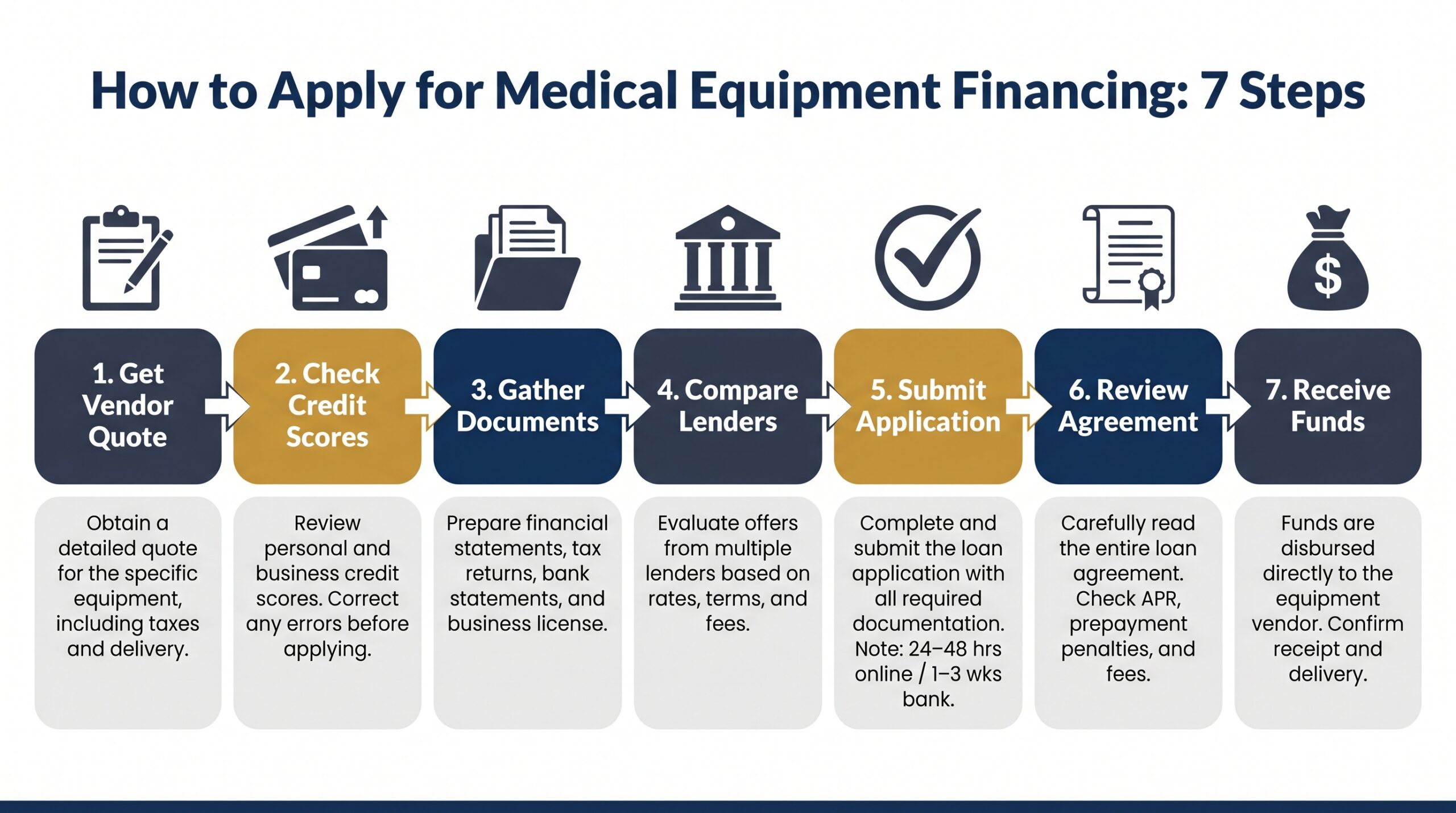

How to Apply for Medical Equipment Financing

- Get a vendor quote or invoice. Lenders need to know exactly what you’re buying and what it costs. Contact your equipment vendor or manufacturer and request a formal quote before you apply.

- Check your credit scores. Pull both your personal and business credit scores. Knowing where you stand helps you target the right lenders and avoid unnecessary hard inquiries.

- Gather your financial documents. Most lenders want two years of business tax returns, three to six months of bank statements, financial statements, your business license, and the equipment details.

- Compare lenders. Banks, credit unions, online lenders, healthcare specialty lenders, and equipment vendors all offer financing at different rates and terms. See our best equipment financing companies guide for a vetted shortlist.

- Submit your application. Online lenders often approve within 24 to 48 hours. Traditional banks typically take one to three weeks.

- Review the financing agreement carefully. Don’t just look at the monthly payment. Focus on APR, total cost of financing, prepayment penalties, and end-of-term conditions. Our equipment financing agreement guide explains every clause worth scrutinizing.

- Receive funds and take delivery. Some lenders pay your vendor directly. Others deposit funds into your business account for you to complete the purchase.

Medical Equipment Financing vs. Other Funding Options

One common misconception worth clearing up before you start planning your budget: Medicare does not cover equipment your practice purchases for clinical use. Medicare Part B covers durable medical equipment for patients, things like wheelchairs and oxygen concentrators, but that’s a patient benefit, not a practice funding source.

Here’s how medical equipment financing stacks up against other funding routes:

- Business line of credit: Flexible, but typically lower limits and higher rates than dedicated equipment financing. Better for operational expenses than large equipment purchases.

- SBA 7(a) loan: Lower rates and longer terms, but slower approval (weeks to months) and heavier documentation requirements.

- Practice acquisition loan: Designed for buying an existing practice, not individual equipment purchases. Different underwriting criteria entirely.

- Equipment financing: Purpose-built for this use case. The equipment secures the loan, approval is faster, and terms align with the asset’s useful life.

For most healthcare practices buying specific clinical assets, dedicated equipment financing is the most efficient path.

Pros and Cons of Medical Equipment Financing

| Pros | Cons |

|---|---|

| Preserves working capital and cash flow | Total cost is higher than paying cash due to interest |

| Fixed monthly payments make budgeting predictable | Equipment may become obsolete before the loan is paid off |

| Equipment secures the loan; no other assets pledged | Missed payments can trigger repossession |

| Potential Section 179 deduction on the full purchase price in year one | Payment obligations continue even if practice revenue drops |

| Finance up to 100% of equipment cost with some lenders | |

| Faster approval than SBA loans or traditional business loans |

Financing makes the most sense when the equipment directly generates revenue ( imaging systems, laser devices, diagnostic tools), where monthly income from its use covers or exceeds the loan payment. If you’re financing equipment without a clear revenue tie, run the numbers carefully before committing.

Medical Equipment Financing FAQs

What credit score is needed for medical financing?

Most lenders require a minimum personal credit score of 600–650. A score of 650+ unlocks better rates and terms, while traditional banks and SBA programs typically want 680 or higher.

How hard is it to get equipment financing?

It’s one of the more accessible forms of business financing because the equipment secures the loan. Approval rates run approximately 68–75% with alternative lenders and 42–52% with traditional banks (Crestmont Capital).

Can a new medical practice get equipment financing?

Yes, though approval is harder. Lenders will lean heavily on your personal credit score, professional credentials, and the resale value of the equipment you’re financing.

Does Medicare pay for medical practice equipment?

No. Medicare Part B covers certain durable medical equipment for patients in home settings. It does not fund equipment purchases made by healthcare practices.

What is the difference between medical equipment financing and leasing?

Financing ends in ownership. Leasing means returning or buying out the equipment at term end. For fast-evolving technology like imaging or laser systems, leasing often makes more sense.

Can I finance used medical equipment?

Yes. Many lenders will finance pre-owned or refurbished equipment, though some impose age or condition limits. See our full guide on used equipment financing for lender-specific details.

Whether you’re equipping a startup practice or upgrading an established clinic, the right financing puts revenue-generating tools in place without draining your cash reserves. Compare lenders, know your numbers, and apply with your documents ready. The sooner the equipment is placed in service, the sooner it starts paying for itself.

Founder of Nanotom Capital & Nanotom Labs