Key Takeaways

- Commercial kitchen equipment costs $40,000–$200,000 for most startups, making financing the only practical path to opening for the majority of restaurant operators.

- Equipment loans (7.9%–34% APR) give you immediate ownership; leases run lower monthly payments but cost more over time and leave you with no asset at the end.

- A 680+ credit score unlocks the best rates and SBA eligibility; scores between 550–679 still qualify with most lenders, but expect higher APRs and larger down payments.

- Section 179 lets you deduct up to $1,250,000 in equipment costs in the year it’s placed in service, meaning you can write off a financed oven system in full while still making monthly payments.

- SBA 504 loans offer the lowest rates at 5%–7% for large equipment purchases; merchant cash advances carry factor rates of 1.10–1.50, making a $50,000 advance cost as much as $75,000 total.

- Online lenders can approve restaurant equipment financing in 24–48 hours; SBA loans take 2–4 weeks minimum. Match your timeline to the right product before applying.

- Vendor financing programs occasionally offer 0% promotional rates, making them the cheapest option available if you qualify. Always ask before defaulting to a third-party lender.

Buying commercial kitchen equipment outright can drain your entire operating budget before you serve a single plate. Restaurant equipment financing solves that by spreading costs over time, keeping cash available for payroll, inventory, and growth.

This guide covers everything, loans, leases, SBA programs, credit requirements, and exactly how to apply.

What Is Restaurant Equipment Financing?

Restaurant equipment financing is a funding solution that lets owners acquire commercial kitchen equipment, ovens, refrigerators, fryers, POS systems, walk-in coolers through loans or leases instead of paying the full cost upfront, with repayment structured in fixed monthly installments over a set term. If you want a broader primer before diving in, see our guide on what equipment financing is and how it works.

The stakes are real. According to the National Restaurant Association’s 2024 industry data, the U.S. restaurant industry generates $1.4 trillion in annual sales across more than 1 million locations. A well-equipped kitchen isn’t optional; it’s your entire operation.

Startup kitchen equipment typically runs $40,000 to $200,000, which makes cash purchases impractical for most operators. Financing restaurant equipment lets you open or upgrade without wiping out your reserves on day one.

Whether you’re launching your first concept or expanding an existing location, financing for restaurant equipment gives you access to professional-grade tools without a six-figure cash requirement sitting between you and opening day.

What Equipment Can Be Financed?

Most lenders treat restaurant equipment financing broadly; if it’s tangible and tied to your operation, it’s likely eligible. Financing limits typically range from a few thousand dollars up to $5 million depending on the program and lender.

- Cooking equipment: ovens, ranges, fryers, grills, griddles, charbroilers

- Refrigeration: walk-in coolers and freezers, reach-in units, ice machines, display cases

- Food prep: slicers, mixers, food processors, prep tables

- Warewashing: commercial dishwashers, glasswashers

- Beverage equipment: espresso machines, draft beer systems, coffee brewers

- POS and technology: point-of-sale systems, kitchen display systems, inventory software

- Ventilation: hood systems, exhaust fans, fire suppression

- Front-of-house: seating, tables, dinnerware, lighting fixtures

Used equipment is also eligible for financing restaurant equipment, though lenders may require larger down payments or tighter credit thresholds. Learn more in our guide to used equipment financing.

Types of Restaurant Equipment Financing

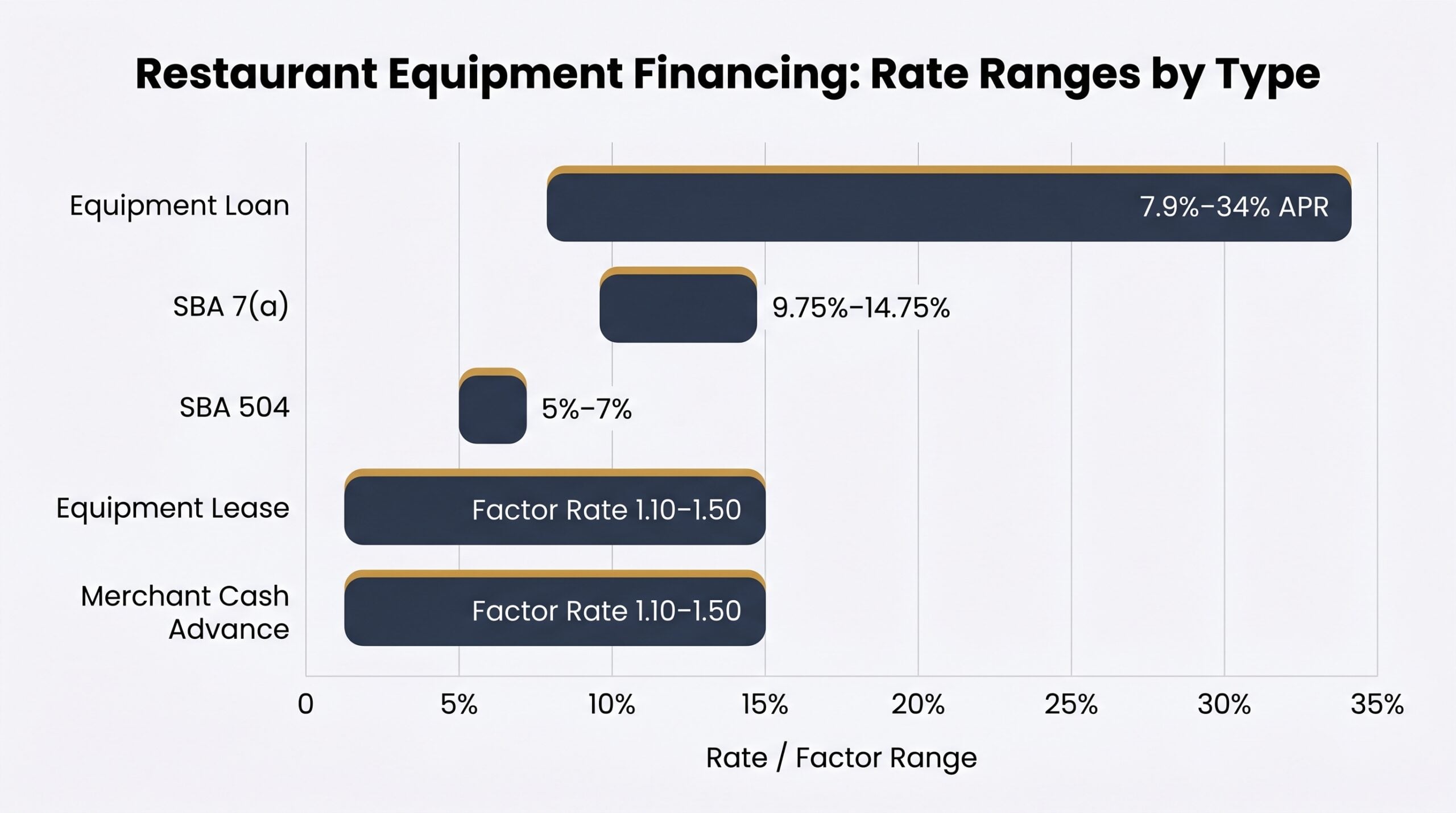

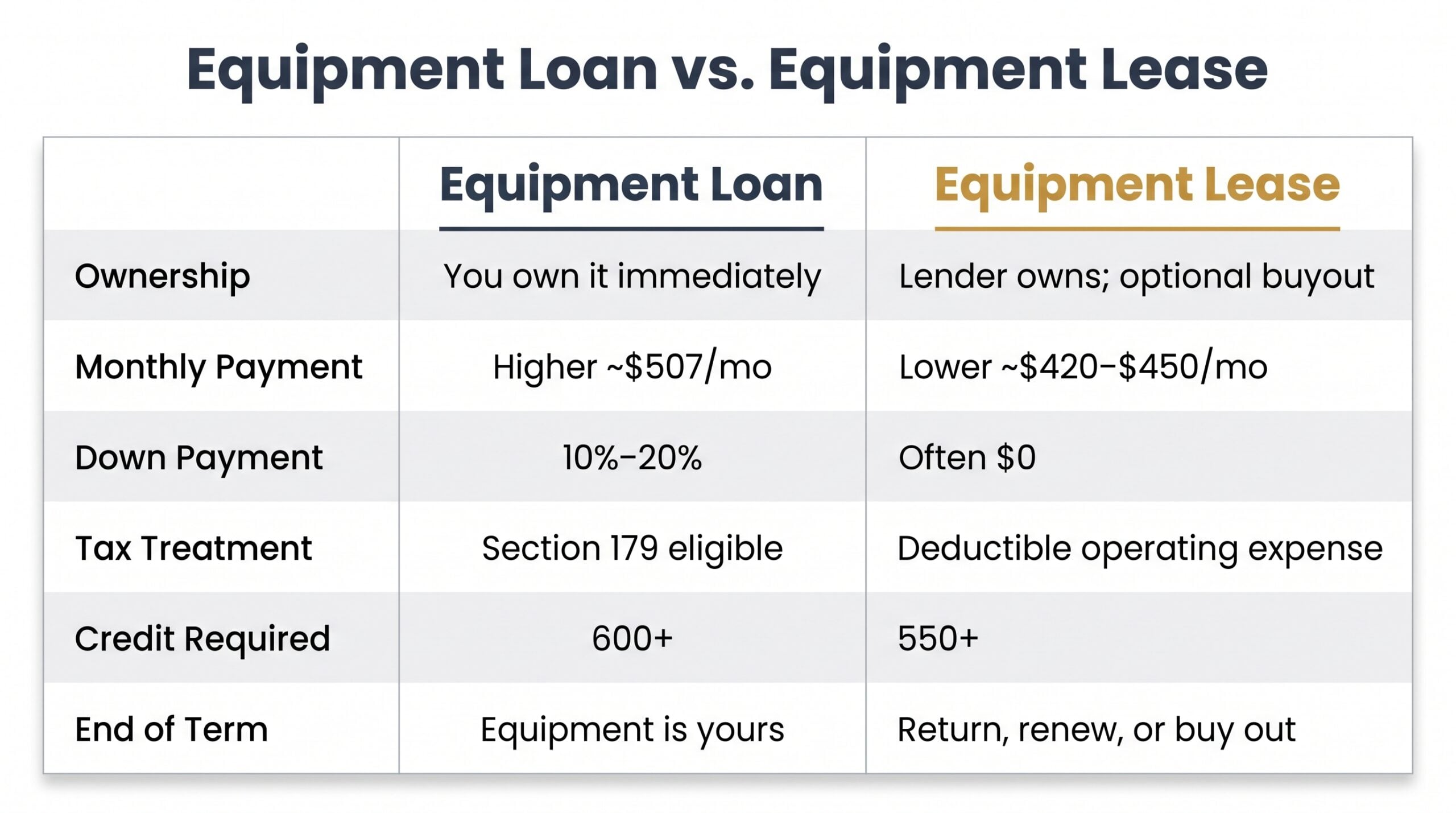

Equipment Loans

The lender funds the equipment, you own it immediately, and repay in fixed monthly installments. The equipment itself serves as collateral. Typical APR runs 7.9%–34%, terms span 2–7 years, and most lenders require a 10%–20% down payment.

Equipment Leasing

You use the equipment, the lender retains ownership, and you pay monthly until the lease ends, then buy out, return, or upgrade. Monthly payments run lower, but total cost is higher.

Here’s what most guides skip on this one: leasing works best for tech-heavy equipment that’ll be obsolete in three to five years. Locking into a five-year loan on a POS system that’s outdated in two isn’t a win just because you own it.

Real numbers on a $20,000 piece of equipment: a loan at 10% APR over 48 months costs roughly $507/month and you own it. A lease on the same equipment runs $420–$450/month with no ownership. See our full equipment leasing vs. financing breakdown to decide which fits your situation.

SBA Loans

Two programs matter most for financing restaurant equipment:

- SBA 7(a): Up to $5M, rates at Prime + 3%–6.5% (currently ~9.75%–14.75% ceiling). In FY2025, the SBA waived upfront fees on loans at or below $1M, reducing out-of-pocket costs at closing.

- SBA 504: Better for large fixed-asset purchases, rates 5%–7%, longer terms. Requires stronger credit and full financial documentation.

Business Lines of Credit

Revolving credit you draw as needed, paying interest only on what you use. It’s ideal for ongoing equipment purchases, repairs, or smaller upgrades spread across multiple buys rather than one large transaction.

Merchant Cash Advances

A lump sum repaid as a percentage of daily card sales. Factor rates run 1.10–1.50, meaning a $50,000 advance at a 1.4 factor rate costs you $70,000 total.

Use this only when speed is critical and every other restaurant equipment financing option is genuinely off the table. Check current equipment financing rates before committing to any product.

Loan vs. Lease: A Side-by-Side Comparison

The honest answer is: neither is universally better. Choosing between a loan and a lease comes down to how long you’ll actually use the equipment, your tax situation, and how much monthly cash flow matters right now.

| Feature | Equipment Loan | Equipment Lease |

|---|---|---|

| Ownership | You own it immediately | Lender owns it; optional buyout at end |

| Monthly Payment | Higher | Lower |

| Down Payment | 10%–20% typical | Often $0–first/last payment |

| Tax Treatment | Section 179 deduction eligible | Lease payments deductible as operating expense |

| Best For | Long-life equipment (ranges, walk-ins) | Tech or equipment that becomes obsolete quickly |

| Credit Requirements | Typically 600+ for most lenders | Can be more flexible; 550+ at some lessors |

| End of Term | Equipment is yours, fully paid | Return, renew, or buy out at residual value |

If you’re financing restaurant equipment that’ll run for 10-plus years (a commercial range or walk-in cooler), a loan almost always wins on total cost. For POS systems or espresso machines, leasing keeps you current without locking into depreciating assets. Explore the full trade-offs in our equipment leasing vs. financing guide.

How to Qualify for Restaurant Equipment Financing

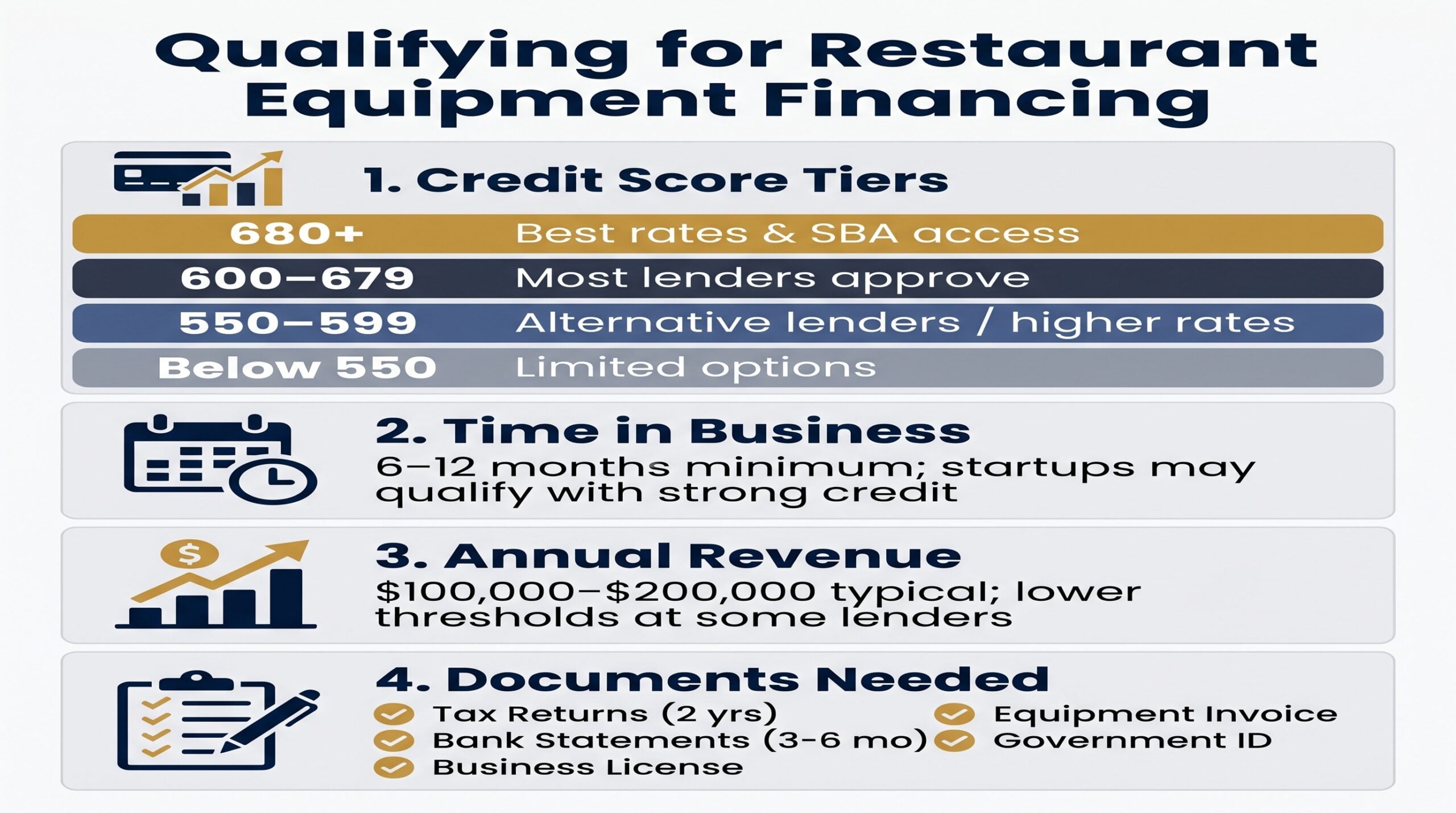

Credit Score Requirements

Your credit score is the first filter most lenders run. Here’s what each tier realistically gets you:

- 680+: Best rates and terms; access to SBA programs and bank lenders

- 600–679: Most lenders approve; expect slightly higher APR

- 550–599: Alternative lenders available; higher rates and down payments likely

- Below 550: Limited options; may need collateral, a larger down payment, or no-credit-check equipment financing

Time in Business

Most lenders require 6–12 months of operating history. Startups can still qualify, but expect stricter credit requirements or a business plan review. Our startup equipment financing guide covers those options in detail.

Revenue Requirements

Standard programs typically require $100,000–$200,000 in annual revenue. Some alternative lenders set lower thresholds, especially for financing restaurant equipment under $50,000.

Documents You’ll Need

- Business tax returns (last 2 years)

- Bank statements (3–6 months)

- Business license

- Equipment invoice or vendor quote

- Driver’s license or government-issued ID

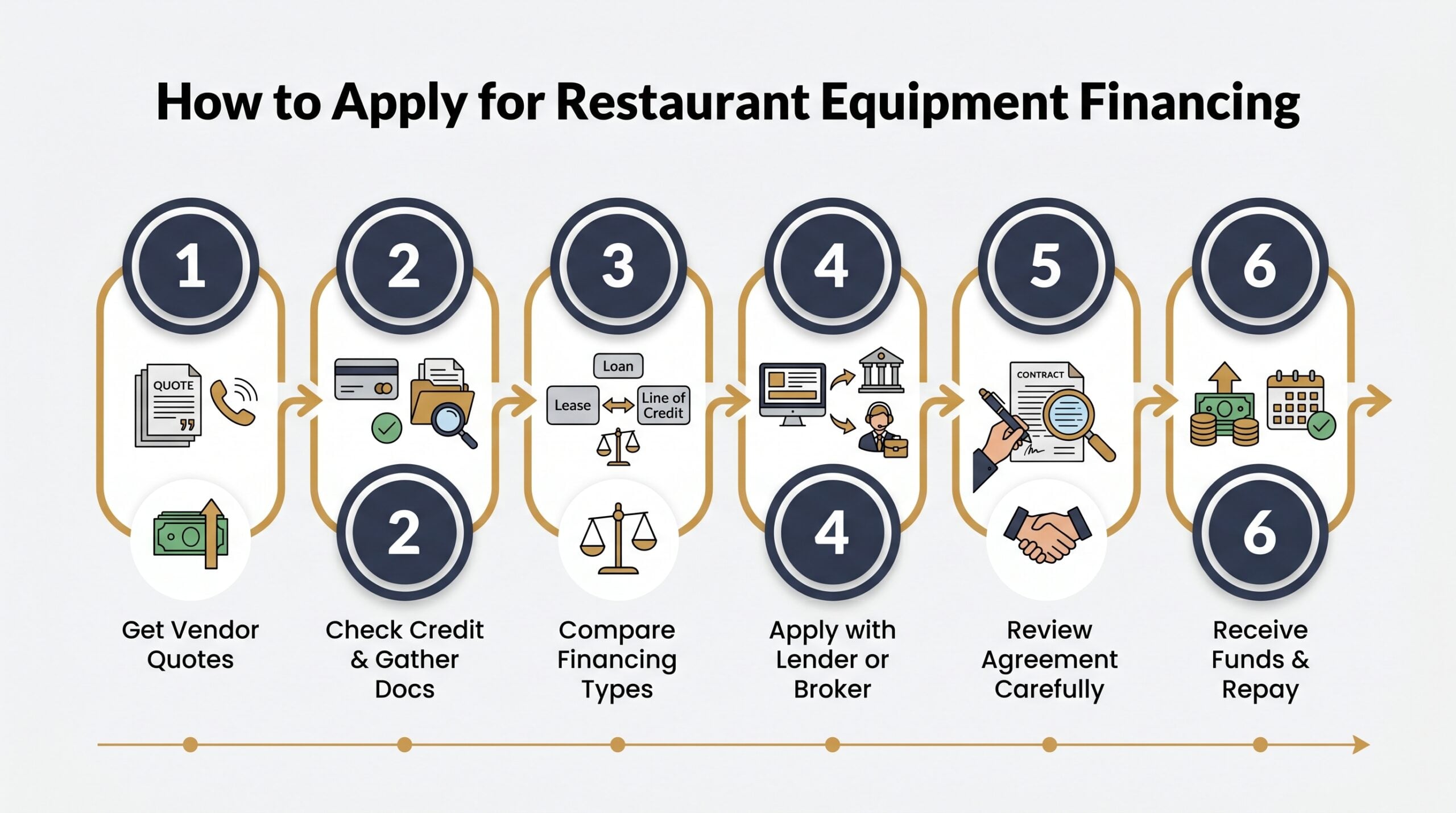

How to Apply: Step-by-Step Process

- Get vendor quotes for every piece of equipment you need. Know your exact number before you apply. Lenders want an invoice or quote, and you don’t want to underfinance and come back a second time.

- Check your credit score and gather your documents. Pull your business and personal credit reports. Assemble tax returns, bank statements, your business license, and your equipment quote; most lenders ask for all of these upfront.

- Compare financing types against your qualifications. Match your credit tier and cash flow to the right product. A strong-credit operator with two years of history should explore SBA before defaulting to an alternative lender.

- Apply with a lender or work through a broker. Online lenders can approve restaurant equipment financing same-day. SBA loans take 2–4 weeks minimum. An equipment financing broker can shop multiple lenders simultaneously if you want options fast.

- Read the financing agreement carefully before signing. Check the APR, all fees, prepayment penalties, and end-of-lease terms. Our equipment financing agreement guide walks through every clause worth scrutinizing.

- Receive funds and begin repayment. Most lenders pay the vendor directly. Your first payment typically hits 30 days after funding.

Restaurant Equipment Financing Rates and Costs: What to Expect

Interest Rates by Financing Type

| Financing Type | Typical Rate |

|---|---|

| Equipment Loan | 7.9%–34% APR |

| SBA 7(a) | ~9.75%–14.75% |

| SBA 504 | 5%–7% |

| Equipment Lease | Factor rate 1.10–1.50 |

| Merchant Cash Advance | Factor rate 1.10–1.50 |

| Line of Credit | Varies by lender and credit profile |

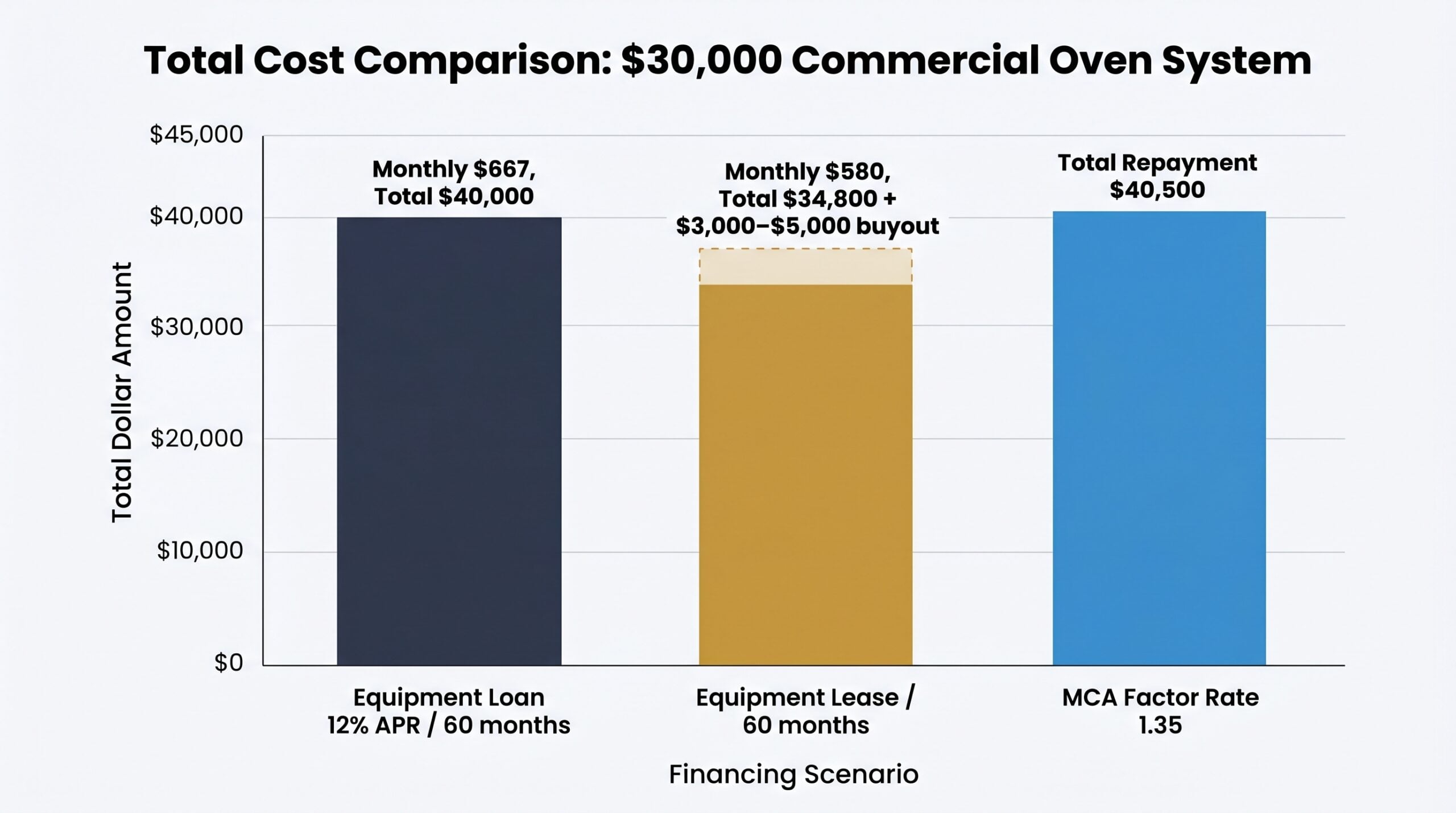

Total Cost Scenario: A Real-World Example

A restaurant finances a $30,000 commercial oven system three different ways:

- Equipment loan at 12% APR, 60 months: ~$667/month, ~$40,000 total; you own it outright

- Equipment lease, 60 months: ~$580/month, ~$34,800 total; but no ownership, plus a $3,000–$5,000 buyout if you want to keep it

- MCA at 1.35 factor rate: receive $30,000, repay $40,500; highest cost, fastest repayment drawn from daily card sales

Down payments for restaurant equipment financing loans typically run 10%–20%. Leases often require nothing upfront beyond first and last payment. Use an equipment financing calculator to model your specific scenario before applying.

Tax Benefits of Financing Restaurant Equipment

Financing restaurant equipment doesn’t just preserve cash flow; it can generate real tax advantages in the year you put the equipment in service.

Section 179 lets you deduct the full purchase price of qualifying equipment rather than depreciating it over years. According to IRS Publication 946, for 2025 the deduction limit is $1,250,000, with the phase-out beginning at $3,130,000 in total equipment purchases. A restaurant that finances a $30,000 oven system could potentially deduct the entire $30,000 in year one, even though they’re still making monthly payments on it.

Bonus depreciation sits at 80% in 2025, offering an additional write-down on equipment costs that exceed or fall outside Section 179 limits.

If you’re leasing, your monthly lease payments may be fully deductible as an ordinary business operating expense. Different mechanism, equally real benefit.

Talk to your accountant before making financing decisions based on tax treatment alone.

Pros and Cons of Restaurant Equipment Financing

| Pros | Cons |

|---|---|

| Preserves working capital for payroll, inventory, and operations | Total cost is always higher than paying cash outright |

| Access equipment immediately without waiting to save | Interest and fees accumulate over the full term |

| Fixed monthly payments make budgeting predictable | Payments are obligatory even when revenue slows |

| Section 179 and bonus depreciation can offset costs significantly | Leases can lock you into equipment that becomes outdated |

| Equipment serves as its own collateral in most cases | Startups face higher rates and stricter approval terms |

| Financing for restaurant equipment scales as your business grows | MCAs and high-rate options can strain daily cash flow |

Restaurant equipment financing makes the most sense when the equipment directly generates revenue, a commercial oven, refrigeration system, or POS setup that pays for itself over time. It makes less sense for low-use or decorative purchases where the interest cost won’t be offset by increased output.

Special Considerations for Startup Restaurants

Startups face the steepest climb when pursuing restaurant equipment financing. No business credit history, no revenue track record, and lenders who price that uncertainty into every offer they send you.

Here’s what startup operators typically run into:

- Down payment requirements of 20%–30% instead of the standard 10%–20%

- Higher APRs across the board

- Personal guarantee requirements on nearly every application

- Shorter approval windows from traditional banks, pushing many startups toward alternative lenders

Kitchen equipment for a new restaurant runs $40,000–$200,000 depending on concept and size. For most founders, financing restaurant equipment isn’t a preference; it’s the only realistic path to opening.

Your best options as a startup: leasing (easier qualification, lower upfront cost), SBA microloans (up to $50,000), vendor financing programs, or lenders who specialize in early-stage businesses. Strong personal credit above 680 helps significantly. See our full startup equipment financing guide for lender-specific options.

Operating a food truck instead? Financing needs and lender criteria differ meaningfully from a brick-and-mortar setup. Our food truck equipment financing guide covers that path separately.

Tips for Getting the Best Terms on Restaurant Equipment Financing

- Improve your credit before applying. A 20-point score increase can drop your rate by several percentage points. Even 60–90 days of credit cleanup is worth it on a $50,000 loan.

- Get multiple quotes. Never accept the first offer. Use an equipment financing broker or marketplace to compare at least three lenders side by side.

- Negotiate lease buyout terms upfront. End-of-lease purchase prices are often negotiable before you sign, not after.

- Match term length to your actual needs. Shorter terms cost less in total interest. Longer terms lower monthly payments but increase overall expense.

- Put more down if you can. A larger down payment reduces your financed amount and total interest paid on financing restaurant equipment.

- Time purchases around Section 179. Place equipment in service before December 31 to capture the deduction in that tax year.

- Ask about vendor financing. Some equipment suppliers offer 0% promotional financing. That’s the cheapest restaurant equipment financing available if you qualify.

Compare lenders directly in our best equipment financing companies roundup.

Frequently Asked Questions

What credit score do I need for restaurant equipment financing?

Most lenders approve at 550–600+. You’ll need 680+ to access the best rates and terms on financing restaurant equipment.

Can I finance used restaurant equipment?

Yes. Most lenders will finance used equipment, though they may require additional documentation, an equipment appraisal, and a larger down payment.

How much can I borrow for restaurant equipment?

Loan amounts range from a few thousand dollars up to $5 million through SBA programs. Most equipment loans fall between $10,000 and $500,000.

Do I need a down payment for restaurant equipment financing?

Loans typically require 10%–20% down. Leases often require little to nothing upfront beyond first and last payment.

Can a startup restaurant get equipment financing?

Yes. Specialized startup lenders, SBA microloans, and equipment leasing all serve new restaurants with limited credit history.

How long does it take to get approved?

Online lenders can approve same-day to 48 hours. SBA loans take 2–4 weeks or longer depending on documentation and lender volume.

Is it better to lease or finance restaurant equipment?

Finance if you want ownership and lower total cost. Lease if you need lower monthly payments, want flexibility to upgrade, or can’t qualify for a loan.

Are restaurant equipment loan payments tax deductible?

Loan interest is deductible, and Section 179 lets you deduct the full equipment cost in year one. Lease payments may qualify as deductible operating expenses.

Ready to move forward? Compare your options, pull your credit score, and get at least three quotes before signing anything. The right restaurant equipment financing structure can mean the difference between a kitchen that strains your cash flow and one that pays for itself. Start with our best equipment financing companies guide to find lenders worth your time.

Founder of Nanotom Capital & Nanotom Labs