Key Takeaways

- A full commercial lawn care setup, mowers, trailers, trimmers, blowers, can cost $80,000 or more, making financing an operational necessity rather than a luxury for most businesses.

- Standard equipment lenders require a minimum credit score of 620–650, but subprime lenders approve borrowers down to 500–580, and lease-to-own programs have no stated minimum.

- Sheffield Financial offers promotional rates as low as 0%–1.99% APR for borrowers with 660+ credit scores across 240+ brands, the most accessible path to low-cost dealer financing.

- Bad credit borrowers can improve approval odds by putting 20%–40% down and demonstrating $10,000+/month in business revenue, which many specialty lenders weigh heavily in their decisions.

- The 2025 Section 179 deduction limit is $2,500,000, meaning a landscaping business financing $80,000 in equipment can potentially deduct the full amount in year one instead of depreciating it over five years.

- Bonus depreciation sits at 40% in 2025 and can be stacked on top of Section 179, further reducing taxable income in the purchase year.

- Most lenders return lawn equipment financing decisions within 24 hours, and prequalification is available via soft pull, meaning you can shop rates without impacting your credit score.

A single zero-turn mower can cost $12,000. A full commercial setup with trailers, trimmers, and blowers can run $80,000 or more. For most lawn care businesses, paying cash upfront isn’t realistic, and that’s exactly where lawn equipment financing closes the gap.

This guide covers every financing option available, including paths to approval with bad credit, real credit score benchmarks, tax strategy, and a step-by-step application process.

What Is Lawn Equipment Financing?

Lawn equipment financing is a funding arrangement where a lender covers the upfront cost of your equipment and you repay it in fixed monthly installments over a set term. The equipment itself typically serves as collateral, which reduces lender risk and makes approval more accessible than unsecured business loans. To understand the foundational mechanics, see our complete beginner’s guide to equipment financing.

Financing lawn equipment at the commercial level is a different animal from consumer financing. Consumer programs target homeowners buying a single riding mower. Commercial and B2B financing structures are built for businesses managing fleets, seasonal cash flow gaps, and rapid scaling needs. That distinction matters.

The U.S. landscaping sector includes roughly 642,000 to 696,000 businesses generating over $153 billion in annual revenue, according to IBISWorld and Laurel Rock 2024 data. In a market that size, landscape equipment financing isn’t a convenience, it’s a core growth lever.

Types of Lawn & Landscaping Equipment You Can Finance

Landscaping equipment financing covers far more than just mowers. If it’s used in your operation, there’s likely a lender willing to fund it. Here’s what qualifies:

- Commercial zero-turn mowers: typically $10,000–$20,000+, the most common financed item

- Lawn tractors and riding mowers: mid-range pricing, popular for smaller crews

- Walk-behind mowers: lower ticket, but still financeable as part of a package

- Commercial trimmers and edgers: often bundled into fleet financing

- Leaf blowers and vacuums: backpack and wheeled commercial units

- Aerators and dethatchers: high-use seasonal equipment

- Skid steers: used for grading, mulching, and heavy landscape work

- Trailers and hauling equipment: enclosed and open trailers both qualify

- Snow removal attachments: plows, spreaders, and blowers for year-round revenue

- Irrigation systems: installation equipment and components

- Full fleet packages: financing multiple units under one agreement

Both new and used equipment qualifies for lawn equipment financing. Used gear typically means slightly higher rates, but approval requirements are often more flexible. If you’re buying pre-owned, read our guide to used equipment financing before you apply.

Outdoor power equipment financing can also cover software, attachments, and maintenance packages when bundled with primary equipment purchases.

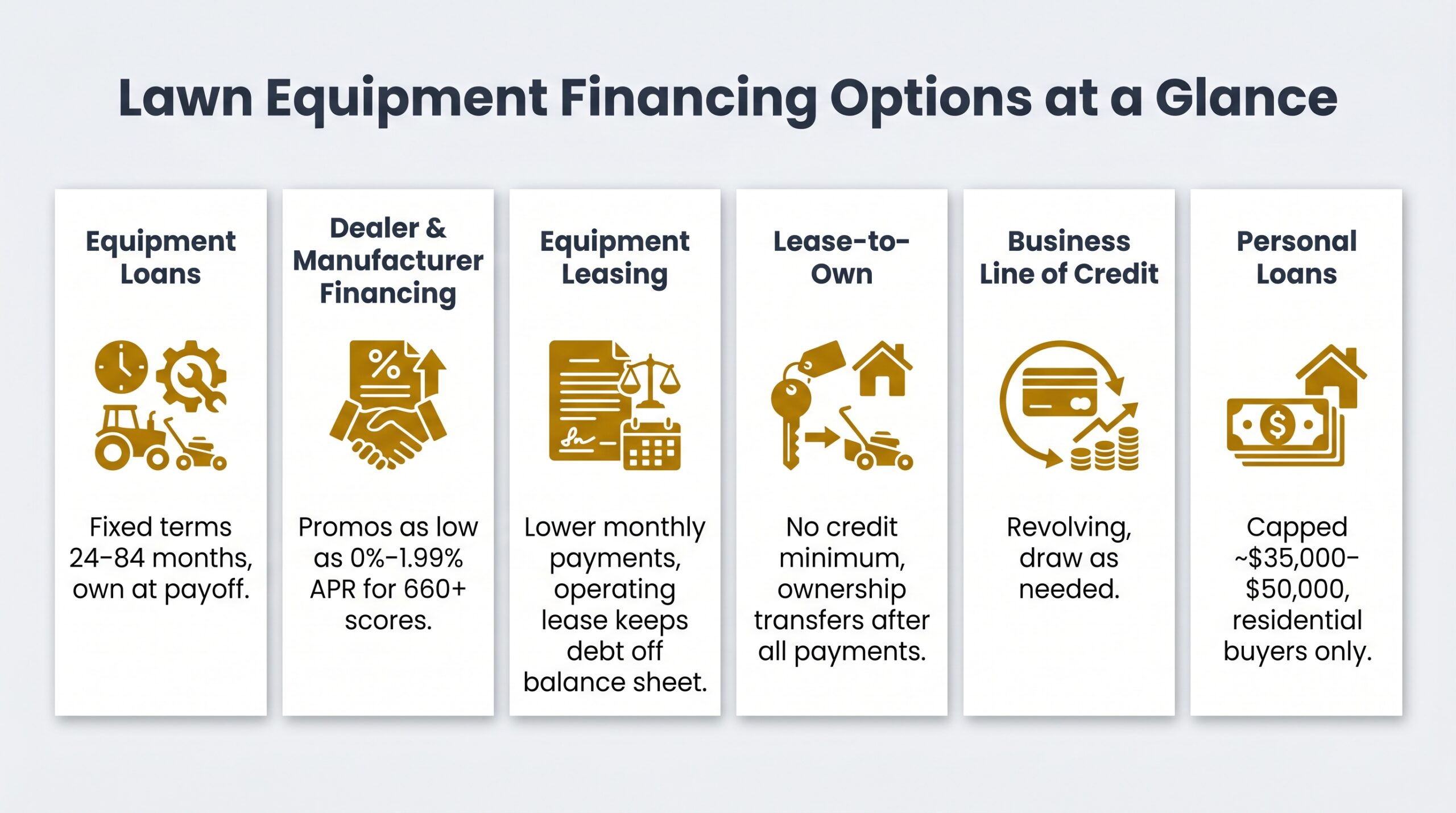

Lawn Equipment Financing Options

There’s no single way to finance landscaping equipment. Your best option depends on your credit profile, how long you’ve been in business, and whether you want ownership or flexibility. Here’s how each structure works.

Equipment Loans

This is the most common approach for commercial buyers. A lender funds the purchase, the equipment serves as collateral, and you repay over fixed terms ranging from 24 to 84 months. You own the equipment outright when the loan is paid off. For a full breakdown, see our complete guide to equipment financing for any type of business.

Dealer & Manufacturer Financing

Sheffield Financial covers financing across 240+ brands and offers promotional rates as low as 0%–1.99% APR for borrowers with 660+ credit scores. Husqvarna partners with Synchrony, typically requiring 550–660+ depending on the program. John Deere Financial evaluates applications holistically without a hard published cutoff.

These programs make lawn equipment financing fast and accessible when you buy through a dealer, and for well-qualified borrowers, they’re often the cheapest money on the table.

Equipment Leasing

Leasing delivers lower monthly payments than loans. An operating lease keeps debt off your balance sheet, which matters for businesses watching their financials. Compare leasing vs. financing here before you decide.

Lease-to-Own / Rent-to-Own

Lease-to-own is the go-to structure for bad credit financing for lawn equipment. You make regular payments, and ownership transfers once you’ve paid in full. Total cost runs higher, but credit requirements are far more lenient, and for some borrowers, it’s the most realistic path to getting equipment in their hands quickly.

Business Lines of Credit

A revolving credit line works well for ongoing equipment needs, repairs, or purchasing multiple smaller items over time. Draw what you need, repay it, and draw again. It’s flexible in a way that a fixed term loan isn’t.

Personal Loans (Residential Buyers)

Solo owner-operators buying a single residential mower can use personal loans, typically capped at $35,000–$50,000. Not practical for commercial fleets or financing landscaping equipment at scale.

Lawn Equipment Financing With Bad Credit

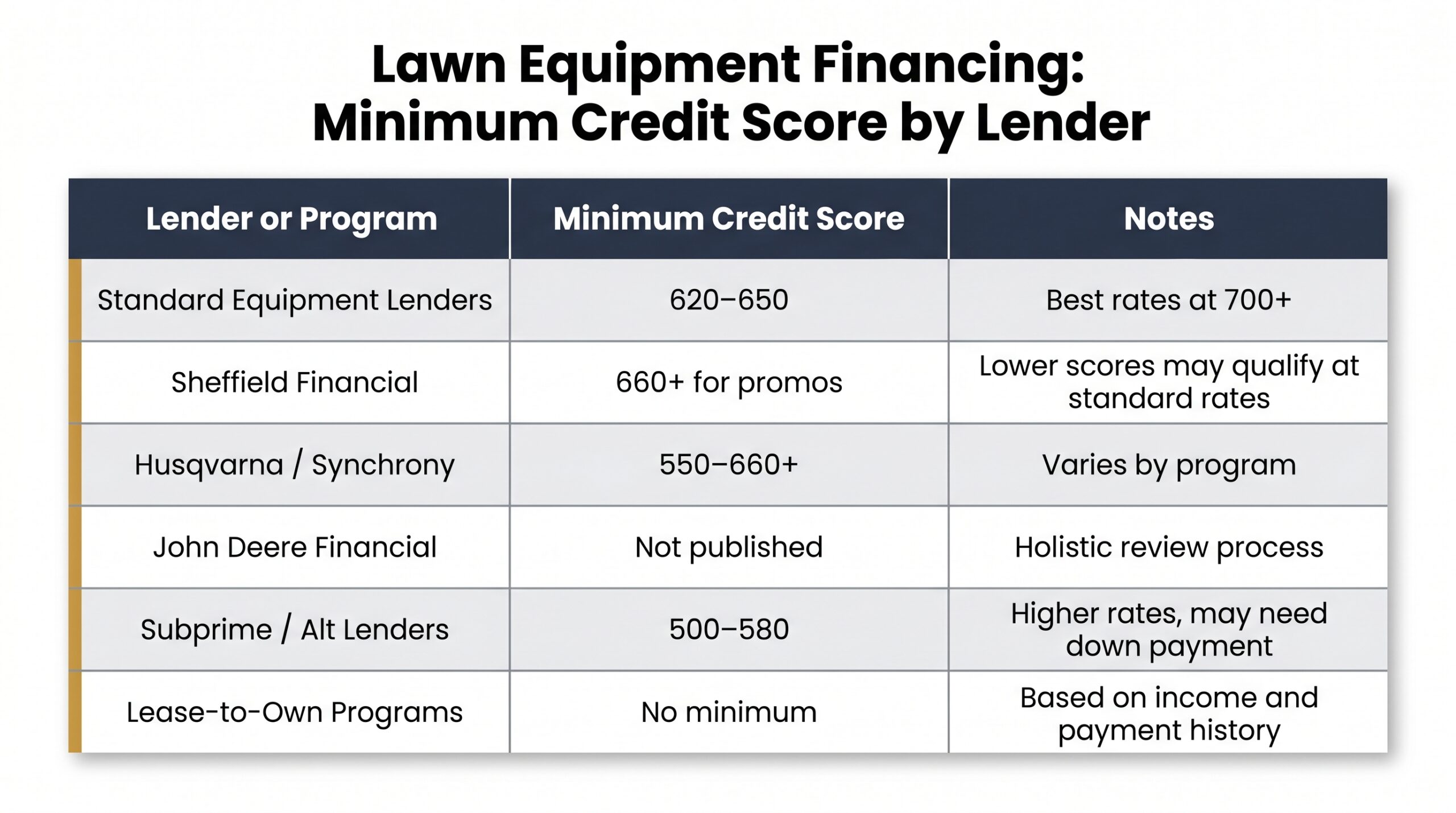

What Credit Score Do You Need for Lawn Equipment Financing?

Here’s what most guides skip: the published minimums aren’t the whole story. Most standard lenders require a minimum credit score of 620–650 for lawn equipment financing, with the best rates reserved for scores above 700. But subprime and specialty lenders approve borrowers down to 500–580, and lease-to-own programs have no stated minimum at all. Sources including Acorn Finance and Roadrunner Financial confirm these benchmarks across commercial equipment programs.

| Lender / Program | Min Credit Score | Notes |

|---|---|---|

| Standard Equipment Lenders | 620–650 | Best rates at 700+ |

| Sheffield Financial (via dealer) | 660+ for promos | Lower scores may qualify at standard rates |

| Husqvarna / Synchrony | 550–660+ | Varies by program |

| John Deere Financial | Not published | Holistic review process |

| Subprime / Alt Lenders | 500–580 | Higher rates, may require down payment |

| Lease-to-Own Programs | No minimum | Based on income and payment history |

How Bad Credit Affects Your Loan Terms

Sub-600 scores typically mean APRs of 18%–35% or higher. Beyond the rate, expect larger down payment requirements of 10%–40%, shorter repayment windows, and possible requests for a co-signer or additional collateral beyond the equipment itself.

Tips to Get Approved With Bad Credit

Lawn equipment financing bad credit approvals are achievable with the right approach. For options with minimal credit requirements, also see no-credit-check equipment financing options.

- Put more down; a 20%–40% down payment significantly reduces lender risk

- Add a co-signer with stronger credit to unlock better terms

- Offer additional collateral beyond the financed equipment

- Show strong revenue; many specialty lenders want to see $10,000+/month in business income

- Apply with specialty equipment lenders rather than traditional banks

- Use lease-to-own while rebuilding your credit score for future financing

Commercial vs. Residential Lawn Equipment Financing

The financing process looks completely different depending on whether you’re running a landscaping business or buying a mower for your backyard. Which category you fall into changes everything, where you apply, what you’ll qualify for, and how much leverage you actually have.

Commercial Landscaping Businesses

Commercial borrowers are evaluated on business revenue, time in business, and cash flow, not just personal credit score. That’s a critical advantage.

A landscaping company with $20,000/month in revenue and a 580 personal credit score has more financing paths available than a consumer with the same score trying to buy a single mower. Loan amounts run higher, the equipment serves as collateral, and repayment terms stretch up to 84 months. For growing operations exploring all available structures, see our overview of business equipment financing options for companies of every size.

Commercial buyers also qualify for the Section 179 tax deduction, which lets you deduct the full cost of financed equipment in the year it’s placed in service. The 2025 deduction limit is $2,500,000, with phase-out beginning at $4,000,000 in total equipment purchases, according to Section179.org. Financing landscaping equipment and writing it off immediately is a legitimate cash flow strategy.

Residential / Consumer Buyers

Consumer lawn equipment financing is simpler but more limited. Lenders look almost exclusively at your personal credit score, and loan amounts are typically smaller. If you’re asking “can I finance a lawn tractor for home use?”, yes, through dealer programs like Sheffield or Synchrony-backed retail financing.

The short version: for home use, your personal credit drives approval. For business use, your financials do the heavy lifting.

Tax Benefits of Financing Lawn Equipment for Your Business

Most lawn care business owners focus entirely on monthly payments. The ones scaling faster are also thinking about what financing lawn equipment does to their tax bill. The numbers here can be meaningful.

Section 179 Deduction

In 2025, businesses can deduct up to $2,500,000 in equipment placed in service during the tax year. The deduction phases out once total equipment purchases exceed $4,000,000. That means a landscaping company financing $80,000 in mowers and trailers can potentially deduct the full amount in year one, not depreciate it over five years. For a growing business, that’s a real difference in cash position.

Bonus Depreciation

Bonus depreciation sits at 40% in 2025, down from the 100% that was available through 2022. It’s declining annually, but it’s still meaningful. You can stack bonus depreciation on top of Section 179 in many cases, further reducing your taxable income in the purchase year.

Deductible Interest and Lease Payments

Interest paid on equipment loans is generally deductible as a business expense. If you’re leasing instead, your full lease payments may be deductible. Either way, the IRS is effectively subsidizing part of your financing cost. To understand how rates affect your total loan cost before you factor in deductions, see our guide to equipment financing rates.

These rules change. Talk to a tax professional before making decisions based on deduction limits.

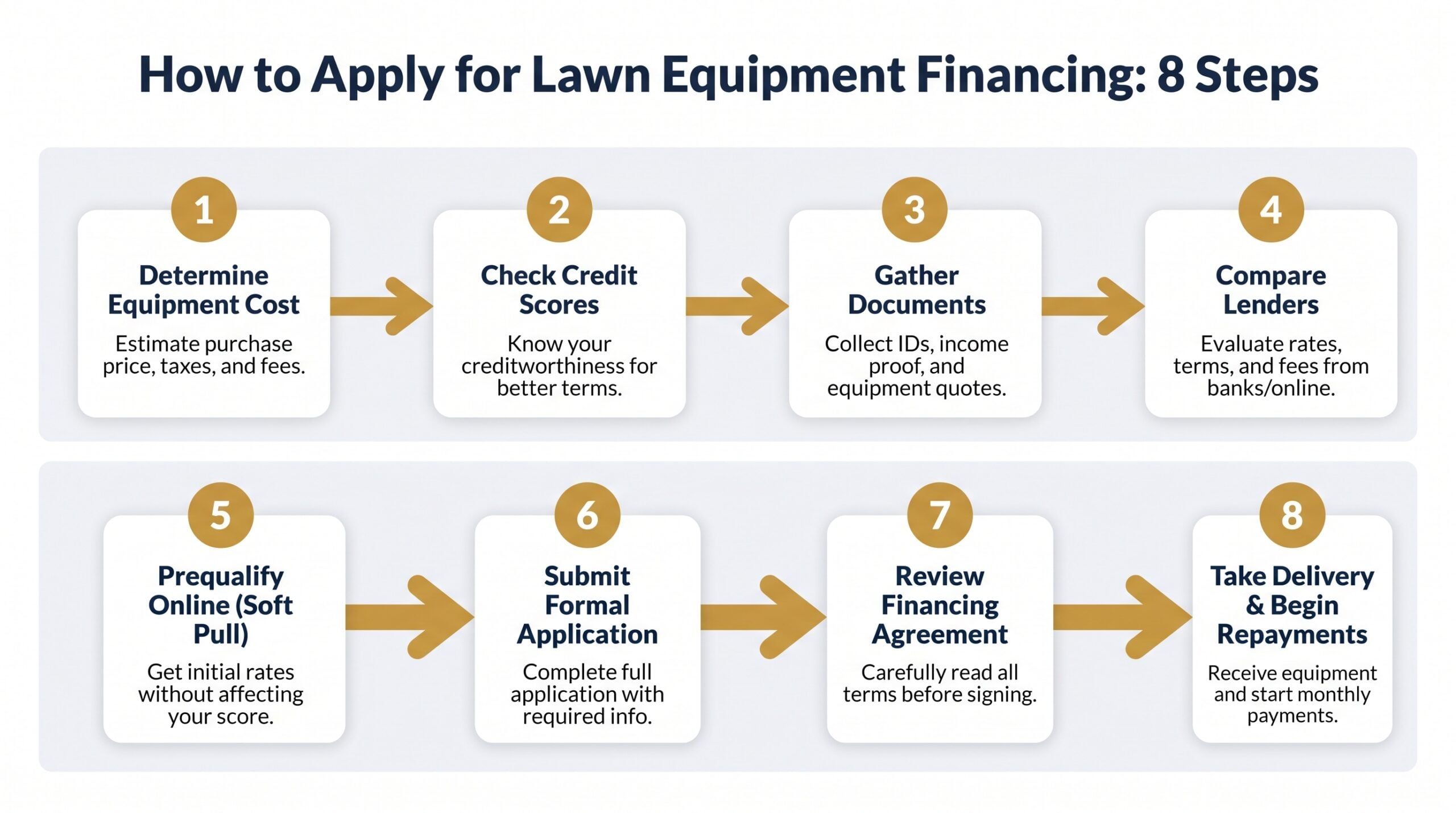

How to Apply for Lawn Equipment Financing

Many lenders offer same-day or next-business-day approval decisions. The process is straightforward when you know what’s coming.

- Determine your total equipment cost. Price out every piece of equipment you need, mowers, trailers, attachments. Use an equipment financing calculator to estimate your monthly equipment payments before you apply.

- Check your credit scores. Pull both your personal and business credit scores. Knowing where you stand lets you target the right lenders and avoid hard inquiries from lenders you won’t qualify with.

- Gather your documents. Most lenders want 3–6 months of business bank statements, recent tax returns, a business license, and an equipment invoice or dealer quote.

- Compare lenders. Dealer financing, direct equipment lenders, and specialty outdoor power equipment financing programs all have different approval criteria and rate structures. Don’t apply to just one.

- Prequalify online. Most lenders offer a soft-pull prequalification that won’t impact your credit score. Start here before submitting a formal application.

- Submit your formal application. Attach your documentation and submit. Landscape equipment financing decisions often come back within 24 hours.

- Review the financing agreement carefully. Check the APR, repayment term, prepayment penalties, and ownership terms before signing. See what to look for in an equipment financing agreement before you commit.

- Take delivery and begin repayments. Equipment ships or is available for pickup, and your repayment schedule starts per the agreement terms.

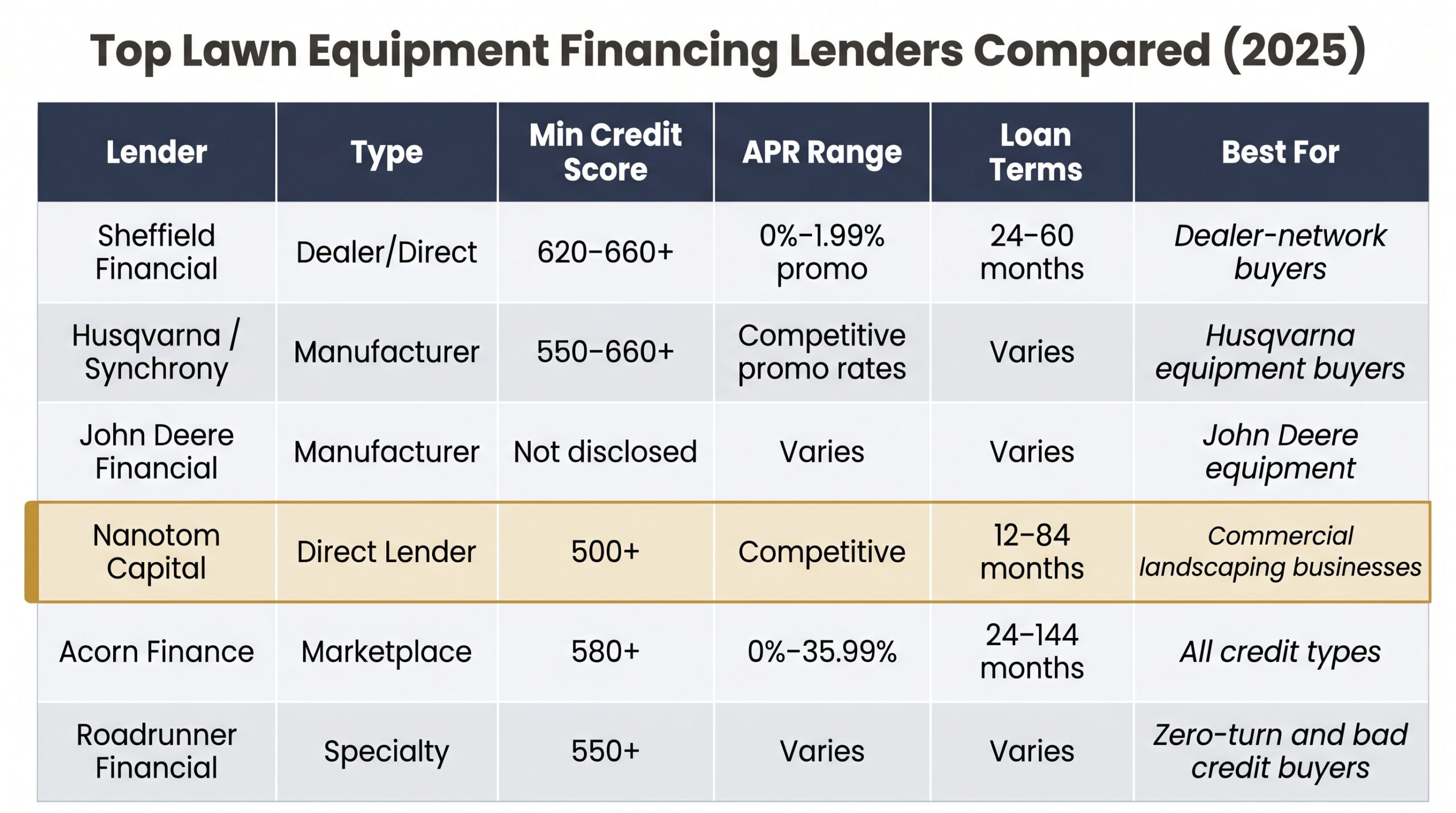

Top Lawn Equipment Financing Lenders Compared

The honest answer is that not every lender is built for every borrower, and applying to the wrong one wastes time and can cost you a hard inquiry. Here’s how the main players stack up for financing lawn equipment across different credit profiles and business types.

| Lender | Type | Min Credit Score | APR Range | Loan Terms | Best For |

|---|---|---|---|---|---|

| Sheffield Financial | Dealer/Direct | 620–660+ | Promos as low as 0%–1.99% | 24–60 months | Dealer-network buyers |

| Husqvarna / Synchrony | Manufacturer | 550–660+ | Competitive promo rates | Varies | Husqvarna equipment buyers |

| John Deere Financial | Manufacturer | Not disclosed | Varies | Varies | John Deere equipment |

| Nanotom Capital | Direct Lender | 500+ | Competitive | 12–84 months | Commercial landscaping businesses |

| Acorn Finance | Marketplace | 580+ | 0%–35.99% | 24–144 months | All credit types |

| Roadrunner Financial | Specialty | 550+ | Varies | Varies | Zero-turn and bad credit buyers |

Landscape equipment financing options have expanded significantly, meaning bad credit borrowers now have real alternatives beyond lease-to-own. For a deeper comparison of lenders across all equipment categories, see our full breakdown of the top equipment financing companies for 2025.

Frequently Asked Questions

What credit score do you need for a lawn mower?

Most dealer financing programs require 550–660+ depending on the lender and promotional offer. Standard equipment loans typically want 620–650 minimum, while lease-to-own programs have no stated minimum.

Can I finance a lawn tractor?

Yes. Both residential and commercial buyers can finance lawn tractors through dealer programs like Sheffield Financial, manufacturer financing through Husqvarna or John Deere, or direct equipment lenders. Commercial buyers have the most options.

What credit score do you need for equipment financing?

Most traditional lenders require 620–650 for standard lawn equipment financing. Specialty and subprime lenders approve borrowers down to 500–580, typically with higher rates and a down payment requirement.

What credit score is needed for John Deere financing?

John Deere Financial doesn’t publish a hard minimum. Applications are reviewed holistically, weighing credit history, income, and down payment together. A score of 650+ generally improves your odds for promotional rate programs.

Can I get lawn equipment financing with bad credit?

Yes. Lease-to-own programs, subprime equipment lenders, and specialty outdoor power equipment financing options all serve borrowers with damaged credit. Strong business revenue and a larger down payment significantly improve your approval odds.

Is lawn equipment financing tax-deductible for my business?

Loan interest is generally deductible as a business expense. Commercial buyers may also qualify for the Section 179 deduction as outlined by the IRS, allowing a full equipment cost deduction in the year it’s placed in service. Consult a tax professional for your specific situation.

What is the minimum down payment for lawn equipment financing?

Standard loans typically require 10%–20% down. Bad credit applicants should expect 20%–40%, as a larger down payment reduces lender risk and improves approval chances.

Ready to move forward? Whether you’re financing landscaping equipment for a growing commercial operation or replacing a single mower, the right lender exists for your credit profile and budget. Apply for lawn equipment financing today and get a decision as fast as the same business day.

Founder of Nanotom Capital & Nanotom Labs