Key Takeaways

- A fully equipped food truck costs $75,000–$175,000 new; financing covers 80–100% of the purchase price when the truck serves as collateral, making approval easier than a standard unsecured business loan.

- Credit scores as low as 550 can qualify with alternative lenders, but expect APRs of 12–20% versus 6–8% for borrowers at 720+, a difference that costs over $16,800 in extra interest on a $70,000 loan over five years.

- SBA Microloans (up to $50,000 at 8–13% APR, 7-year terms) are the strongest option for startups and credit-challenged borrowers; a detailed business plan can offset limited credit history with CDFI underwriters.

- On a $70,000 truck with a 5-year term, monthly payments range from ~$1,393 at 7% APR to ~$1,843 at 20% APR. Run your exact numbers before choosing a lender.

- Financing only covers hard assets (chassis, installed kitchen equipment, generators), permits, food inventory, and commissary fees must be funded separately through savings or a business line of credit.

- Buying beats leasing if you plan to operate three or more years, since you build equity and resale value; leasing makes more sense for testing the concept or upgrading within two years.

- Applying with at least three lenders in a short window minimizes credit score impact and gives you real leverage to negotiate. Online lenders approve food truck equipment financing in as little as 24–48 hours when documents are ready.

A fully equipped food truck costs $75,000 to $175,000 before you serve a single customer. That gap between the dream and the capital required stops most aspiring owners cold. Food truck equipment financing closes that gap by letting you spread costs over time while your truck generates revenue.

This guide covers lender comparisons, real payment estimates, bad-credit options, and a step-by-step application walkthrough, so you have everything in one place.

What Is Food Truck Equipment Financing?

Food truck equipment financing is a specialized form of equipment financing where the truck, trailer, and built-in kitchen equipment act as collateral for the loan. That’s a critical distinction from a general business loan, which is unsecured and harder to qualify for as a new operator.

Because the equipment secures the debt, lenders take on less risk. You get lower rates, longer terms, and a faster approval process than you’d see with a traditional business loan.

Food truck equipment financing can cover nearly every major cost on your list:

- Truck chassis and body

- Commercial kitchen build-out (fryers, grills, ventilation, refrigeration)

- Generators and power systems

- Vehicle wrap and branding

- POS systems and payment terminals

The U.S. food truck industry surpassed $2 billion in revenue in 2025, with 92,000+ trucks operating nationwide. Before diving into food-truck-specific details, it helps to understand the broader mechanics behind how equipment financing works.

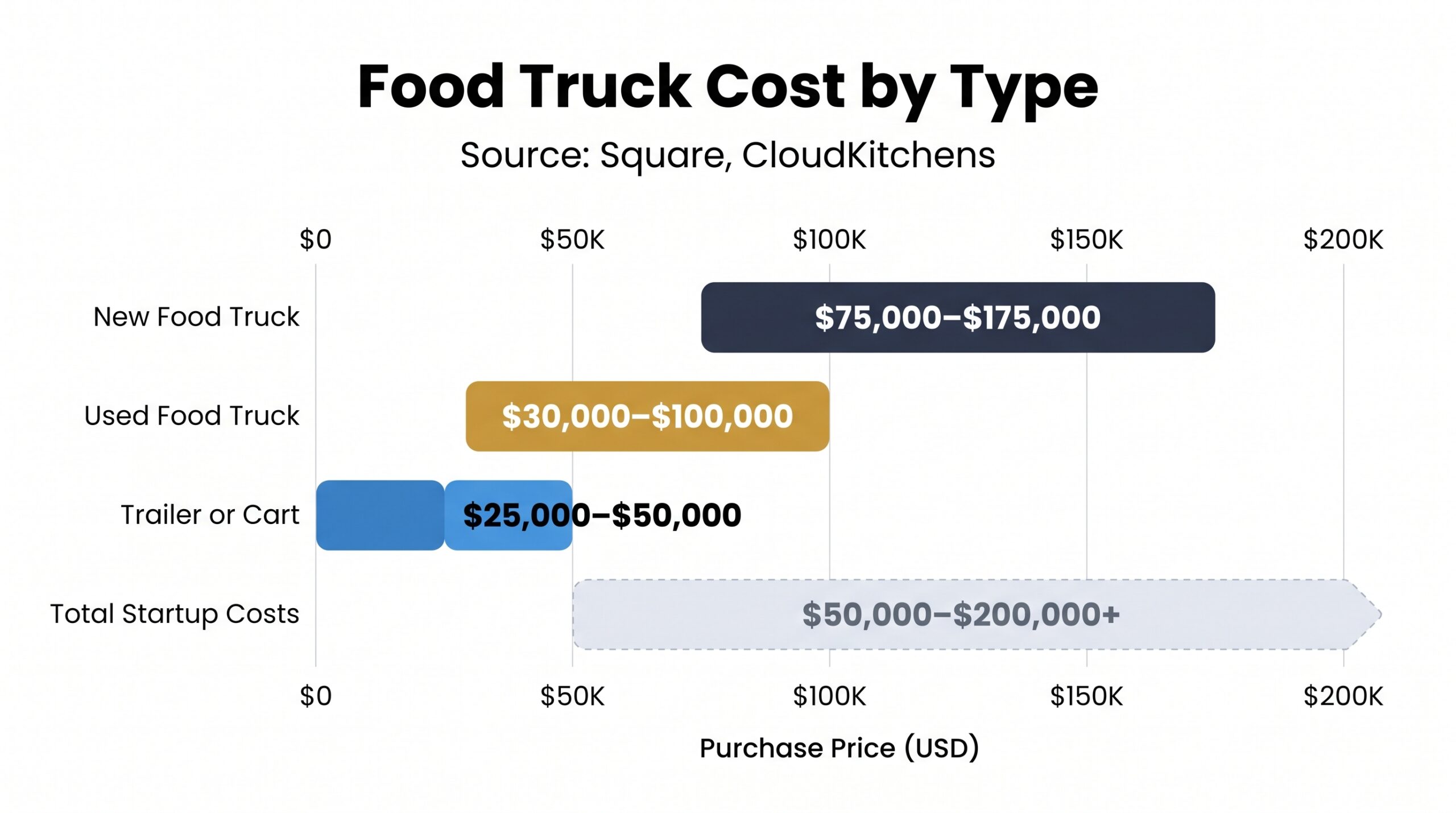

How Much Does a Food Truck Cost? (What Lenders Will Cover)

Before you apply, you need a realistic number. Costs vary widely depending on whether you’re buying new, used, or going the trailer route.

| Type | Price Range | Financing Notes |

|---|---|---|

| New Food Truck | $75,000 – $175,000 | Most lenders cover 80–100% of purchase price |

| Used Food Truck | $30,000 – $100,000 | Some lenders restrict age; trucks over 10 years may be ineligible |

| Trailer or Cart | $25,000 – $50,000 | Qualifies for food truck equipment financing but terms may be shorter |

According to CloudKitchens and Square, total startup costs including permits, licenses, initial inventory, and marketing typically run $50,000 to $200,000+.

What Lenders Will and Won’t Cover

Here’s what most guides skip: financing covers the vehicle and permanently installed kitchen equipment, not everything on your startup list. Fryers bolted to the floor? Covered. A crate of cooking oil? Not covered.

Expenses lenders typically exclude:

- Health permits and business licenses

- Initial food inventory

- Commissary kitchen fees

- Working capital and payroll

Plan to cover those soft costs with savings or a separate business line of credit. Food truck equipment financing is purpose-built for hard assets, not the operating expenses that follow.

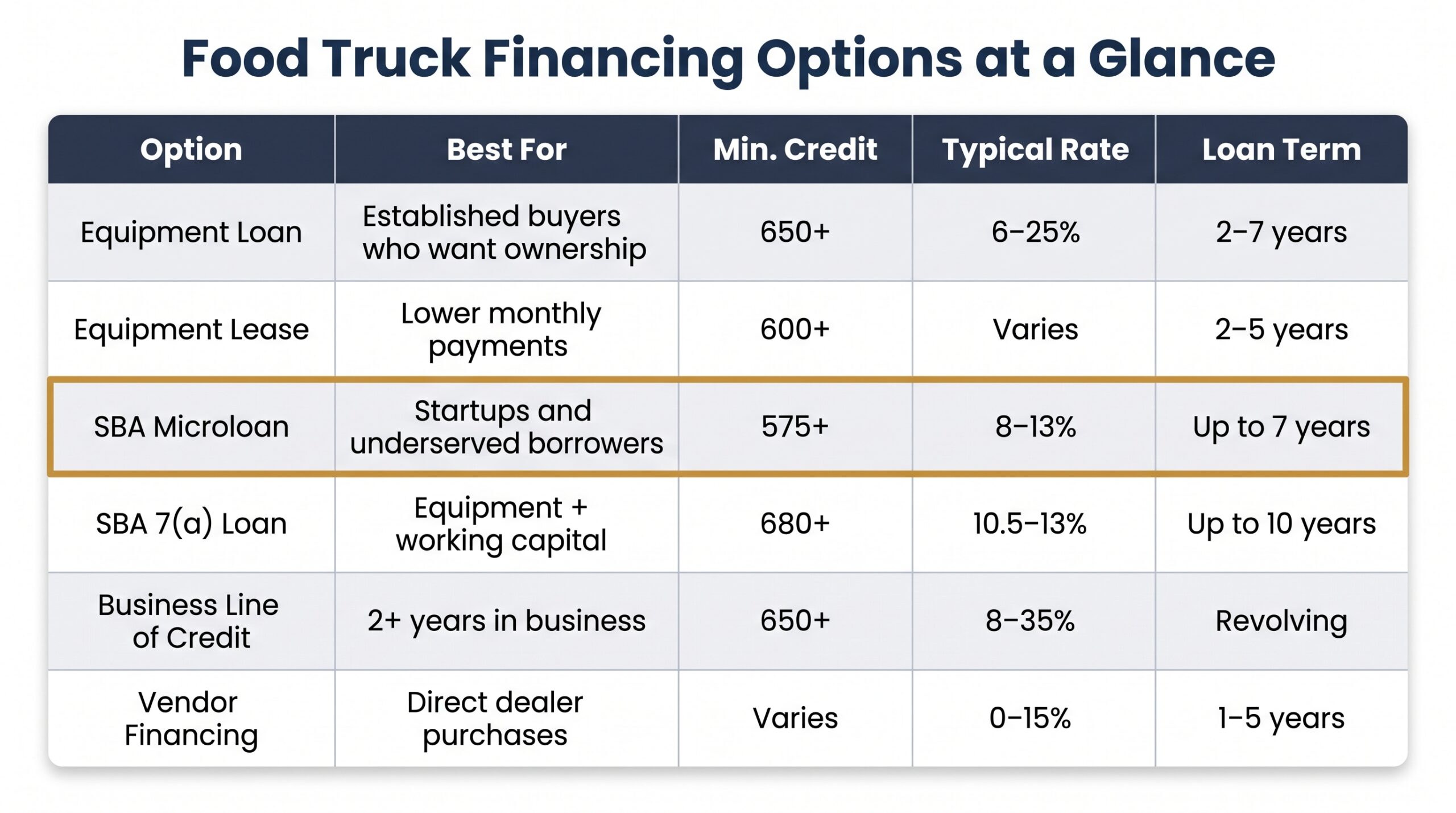

Types of Food Truck Equipment Financing

Not every funding option fits every operator. Here’s how each type works and who it’s actually built for.

| Option | Best For | Min. Credit | Typical Rate | Loan Term |

|---|---|---|---|---|

| Equipment Loan | Established buyers who want ownership | 650+ | 6–25% | 2–7 years |

| Equipment Lease | Operators who want lower monthly payments | 600+ | Varies by residual | 2–5 years |

| SBA Microloan | Startups and underserved borrowers | 575+ | 8–13% | Up to 7 years |

| SBA 7(a) Loan | Operators needing equipment + working capital | 680+ | 10.5–13% | Up to 10 years |

| Business Line of Credit | Established trucks with 2+ years revenue | 650+ | 8–35% | Revolving |

| Vendor Financing | Buyers purchasing directly from dealers | Varies | 0–15% | 1–5 years |

Equipment Loans

The truck serves as collateral, and you own it outright once the loan is paid. Most lenders require a 650+ credit score and 10–20% down. It’s the most straightforward form of food truck equipment financing for buyers with a decent credit history.

Equipment Leasing and Lease-to-Own

Leasing keeps monthly payments lower because you’re not financing the full purchase price. You don’t own the truck at term end unless you exercise a buyout option. If you’re weighing both paths, this breakdown of leasing vs. financing is worth reading before you commit.

SBA Microloans

SBA Microloans go up to $50,000 with rates between 8–13% and terms up to seven years. They’re one of the most startup-friendly food truck equipment financing options available, especially for borrowers with limited credit history. If you don’t have years of revenue behind you, this is often where to start.

SBA 7(a) Loans

SBA 7(a) loans go up to $5 million and can bundle equipment costs with working capital in a single loan. The tradeoff is a longer application process and stricter documentation requirements.

Business Line of Credit

A revolving credit line works well for ongoing equipment needs or repairs. Most lenders want two or more years in business and consistent revenue before approving one, so this isn’t typically a day-one option.

Vendor and Manufacturer Financing

Some truck builders and dealers offer in-house financing, occasionally with 0% promotional periods. Always read the fine print. Deferred interest structures can get expensive fast if you don’t pay off the balance in time.

Food Truck Financing Requirements: What Lenders Look For

Knowing the requirements before you apply saves you hard credit pulls and wasted time. Here’s what most lenders evaluate when reviewing a food truck equipment financing application.

Credit Score Requirements

Quick answer: traditional banks want 680+, online lenders accept 550–650, and SBA programs typically require 650–680.

Your credit score determines your rate as much as your eligibility. A 720 score might get you 7%. A 580 score could push that to 20% or higher. See how credit tiers affect interest rates on equipment financing before you lock in a lender.

Time in Business

SBA Microloans and many equipment-specific lenders will work with startups at zero months in business. Business lines of credit are a different story; most require two or more years of operating history. Food truck equipment financing is genuinely more accessible to new operators than most other loan types.

Revenue and Cash Flow

Established trucks should show three to six months of bank statements. Startups can often substitute a detailed business plan with financial projections. Some alternative lenders care more about your projected revenue than your current bank balance.

Down Payment Expectations

Down payments range from 0% to 20% depending on your credit profile and lender type. Strong credit with an established business? You may qualify for zero down. Thinner credit history usually means 10–15% upfront.

Required Documents

- EIN or tax ID

- Business bank account and voided check

- Business plan or revenue proof

- Equipment invoice or dealer quote

- Personal and business tax returns (last 1–2 years if applicable)

Having these ready before you apply speeds up food truck equipment financing approvals significantly. Some online lenders can approve in 24 hours when your documents are clean and complete.

How to Finance a Food Truck With Bad Credit

Bad credit doesn’t disqualify you from food truck equipment financing. It narrows your options and raises your rate, but there are real pathways forward. Scores below 650 can still qualify with alternative lenders, typically at 12–20% APR.

- Use the truck as collateral with an equipment-focused lender. Many alternative lenders accept 550+ scores specifically because the equipment secures the loan. The truck is their protection if you default, which makes them more flexible on credit.

- Apply through a CDFI for an SBA Microloan. Community Development Financial Institutions underwrite SBA Microloans with more flexibility than banks. A strong business plan can offset a weaker credit score here more than anywhere else.

- Add a co-signer. A co-signer with 680+ credit can unlock better rates and higher approval odds. Make sure they understand they’re fully liable if you don’t pay.

- Consider lease-to-own arrangements. Leasing has lower credit thresholds than purchasing. You build operating history and can refinance into an ownership loan later.

- Build business credit before you apply. Open a dedicated business bank account, get a secured business credit card, and establish vendor trade lines. Six months of consistent activity can meaningfully move your profile.

For operators with no credit history at all, explore no-credit-check equipment financing options or read up on startup equipment financing strategies built specifically for new businesses.

Food truck equipment financing is more accessible to credit-challenged borrowers than general business loans precisely because the asset backs the debt. Work that angle first.

How to Apply for Food Truck Equipment Financing (Step-by-Step)

The honest answer is that most delays in the application process come down to missing documents, not bad credit. Get your paperwork together before you approach a single lender and you’ll move significantly faster.

- Determine your total funding need. Add up the truck, kitchen build-out, vehicle wrap, and a buffer for permits and unexpected costs. Having a specific number makes your application stronger and prevents you from under-borrowing.

- Check your credit score and business credit report. Pull both before any lender does. Errors on your report are common and fixable, but only if you catch them first.

- Choose the right financing type. Match your option to your credit score, time in business, and loan amount using the comparison table in section three. Don’t apply for a bank loan with a 580 score.

- Gather your documents. EIN, three to six months of business bank statements, a business plan or revenue projections, and an equipment quote or invoice from your dealer.

- Compare at least three lenders. Get quotes from a traditional bank, an online lender, and an SBA intermediary if eligible. Rates and terms vary significantly across lender types.

- Submit your application. Online lenders typically approve food truck equipment financing applications within 24–48 hours. SBA loans take two to four weeks. Plan your timeline accordingly.

- Review the financing agreement before signing. Check the APR, total repayment amount, term length, and prepayment penalties. Read the full breakdown of what to look for in an equipment financing agreement before you sign anything.

Food truck equipment financing moves fast with online lenders. Having clean documents ready on day one is the single biggest factor in how quickly you get funded.

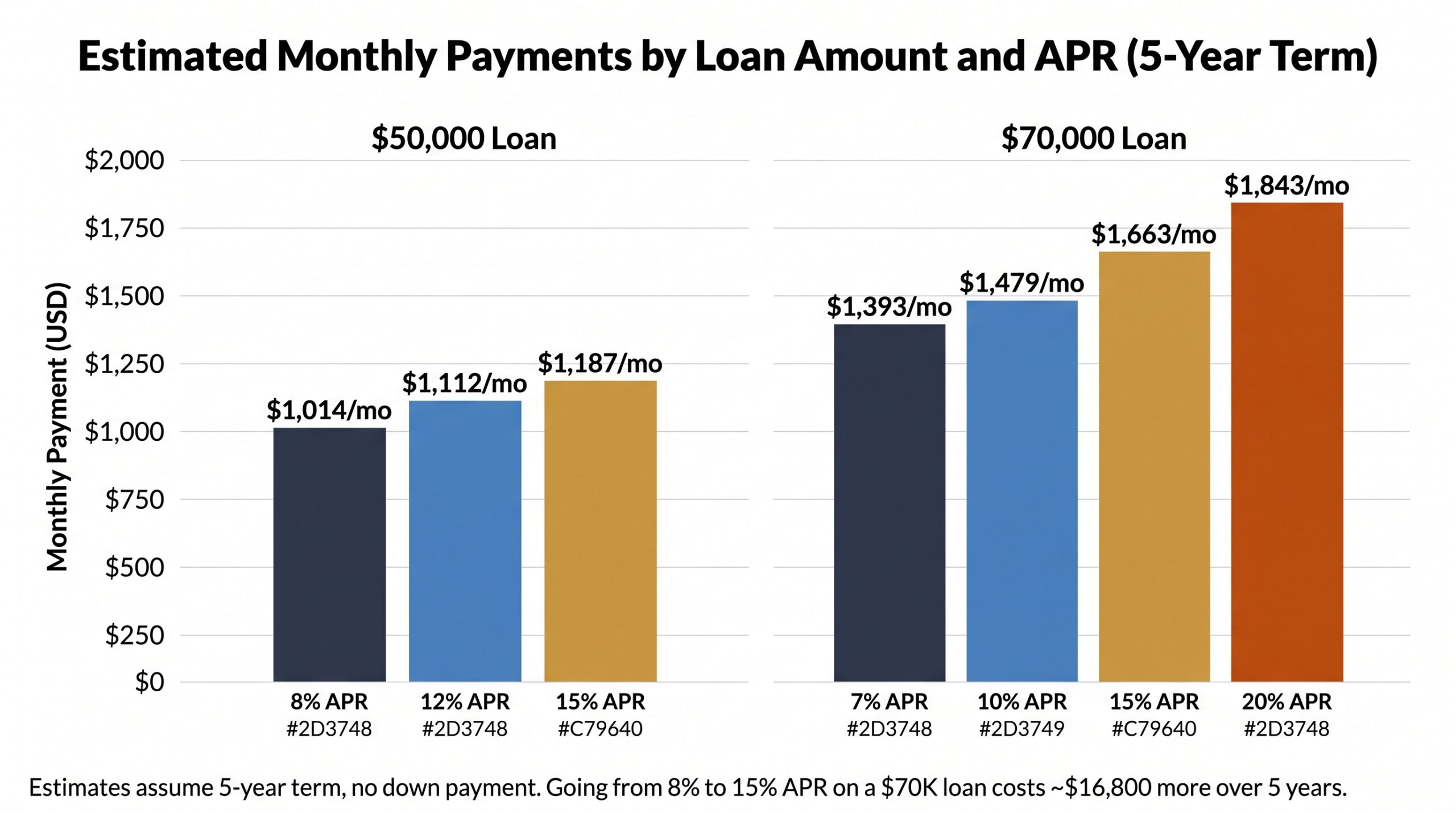

Food Truck Financing Payment Estimator

Before you commit to food truck equipment financing, you need to know what the monthly payment looks like against your projected revenue. These estimates assume a 5-year term with no down payment.

How Much Is the Monthly Payment on a $50,000 Business Loan?

| Loan Amount | APR | Term | Est. Monthly Payment |

|---|---|---|---|

| $50,000 | 8% | 5 years | ~$1,014/mo |

| $50,000 | 12% | 5 years | ~$1,112/mo |

| $50,000 | 15% | 5 years | ~$1,187/mo |

How Much Is a $70,000 Truck Payment?

| Loan Amount | APR | Term | Est. Monthly Payment |

|---|---|---|---|

| $70,000 | 7% | 5 years | ~$1,393/mo |

| $70,000 | 10% | 5 years | ~$1,479/mo |

| $70,000 | 15% | 5 years | ~$1,663/mo |

| $70,000 | 20% | 5 years | ~$1,843/mo |

Three factors move these numbers the most: your credit score, your loan term, and your lender type. Shortening to a 3-year term increases monthly payments but can cut total interest paid by 30–40%. Going from 8% to 15% APR on a $70K loan costs you an extra $16,800 over five years.

These are estimates. Your actual food truck equipment financing payment depends on your specific credit profile and lender terms. Use our equipment financing calculator to run your exact numbers before you apply.

Tips to Improve Your Approval Odds Before Applying

Most food truck equipment financing rejections are preventable. These steps won’t guarantee approval, but they meaningfully shift the odds in your favor before you submit a single application.

- Clean up your personal credit first. Pay down revolving credit card balances below 30% utilization and dispute any errors on your report. Even a 20-point score improvement can move you into a better rate tier.

- Open a dedicated business bank account. Keep three to six months of statements clean, consistent deposits, no overdrafts. This is the document lenders scrutinize most.

- Register your business properly. An LLC or sole proprietorship with an EIN signals legitimacy. Some lenders won’t process food truck equipment financing applications from unregistered businesses at all.

- Get a dealer quote before you apply. Lenders want to see a specific asset with a specific price. An equipment invoice or formal quote strengthens your application and speeds up underwriting.

- Prepare a one-page business plan. Include your target market, projected monthly revenue, and cost structure. Startups especially need this to offset limited operating history.

- Start with a smaller loan amount. Borrowing $40,000 instead of $70,000 increases your approval odds substantially. Build repayment history, then refinance into a larger amount later.

- Apply with multiple lenders. Rate shopping food truck equipment financing with two to three lenders in a short window minimizes credit score impact and gives you real leverage to negotiate.

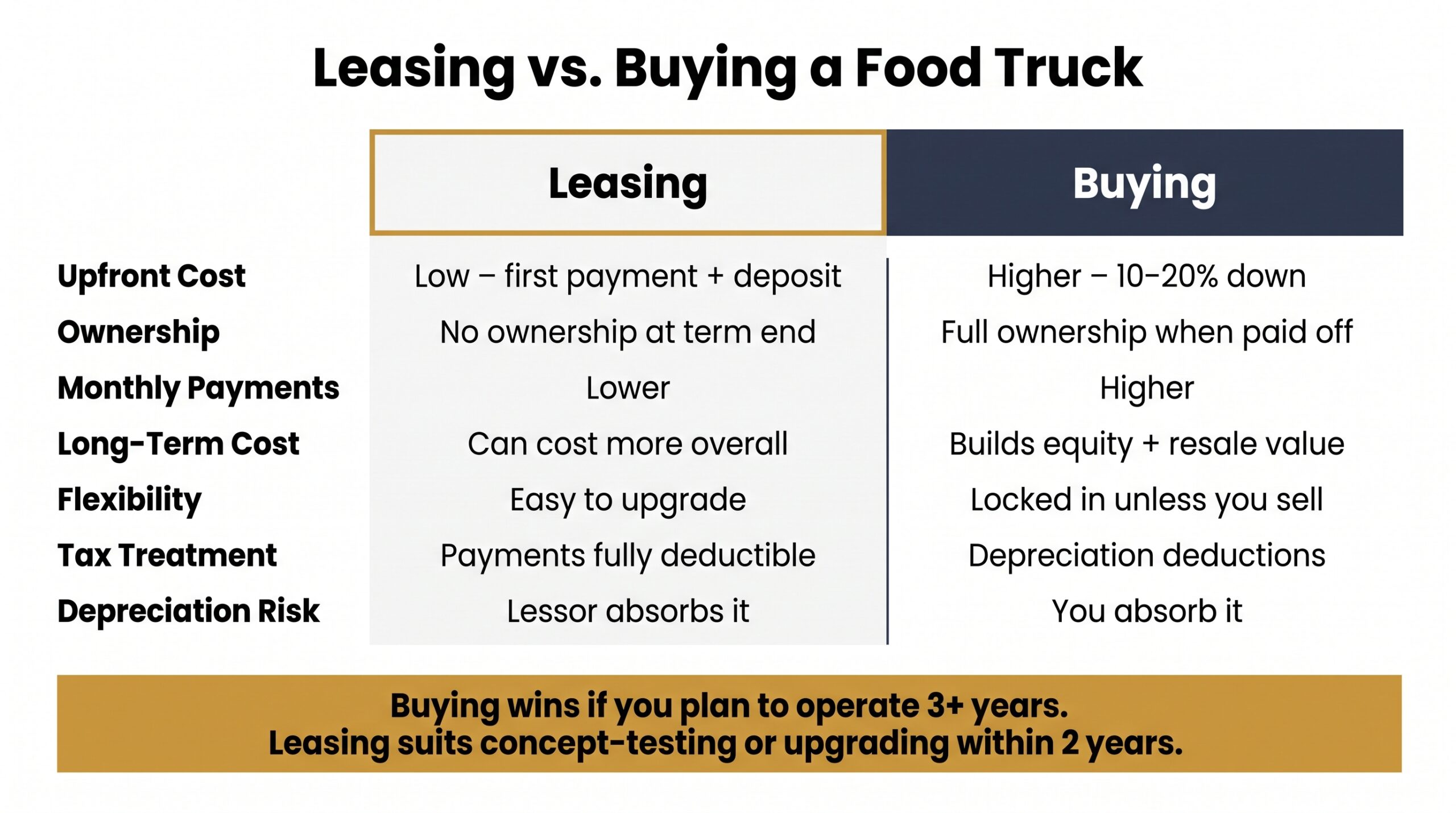

Leasing vs. Buying a Food Truck: Which Makes More Sense?

Your food truck equipment financing strategy changes significantly depending on whether you lease or buy. Here’s how the two paths compare directly.

| Leasing | Buying | |

|---|---|---|

| Upfront Cost | Low: first payment and security deposit | Higher: typically 10–20% down |

| Ownership | No ownership at term end (unless buyout) | Full ownership once paid off |

| Monthly Payments | Lower | Higher |

| Long-Term Cost | Can cost more overall | Builds equity and resale value |

| Flexibility | Easier to upgrade equipment | Locked in unless you sell |

| Tax Treatment | Payments fully deductible as operating expense | Depreciation deductions available |

| Depreciation Risk | Lessor absorbs it | You absorb it |

If you’re planning to operate the truck for three or more years, buying through food truck equipment financing builds equity and gives you an asset you can sell. If you’re testing the concept or expect to upgrade your setup within two years, leasing keeps your cash flexible.

Buying a used truck is a third option worth considering. It lowers your loan amount and monthly payment while still giving you full ownership. Read more about used food truck financing to see how that process works.

For a deeper breakdown of both paths, the full guide on equipment leasing vs. financing covers every scenario worth knowing.

Frequently Asked Questions

How hard is it to finance a food truck?

If your credit score is 650+ and you’re using the truck as collateral, it’s moderately straightforward. It gets harder for startups or borrowers with damaged credit, but SBA Microloans and alternative lenders make food truck equipment financing accessible even in those situations.

What credit score is needed for equipment financing?

Most lenders want 650 or higher. Traditional banks typically require 680+, while some alternative lenders will approve food truck equipment financing at scores as low as 550, with higher rates and stronger collateral requirements to match.

How much is the monthly payment on a $50,000 business loan?

On a 5-year term, expect roughly $1,014 per month at 8% APR up to $1,187 per month at 15% APR. Your actual rate depends on your credit score, lender type, and whether you put money down.

How much is a $70,000 truck payment?

On a 5-year term, monthly payments range from approximately $1,393 at 7% APR to $1,663 at 15% APR. Borrowers with weaker credit at 20% APR can expect around $1,843 per month.

Can I finance a food truck as a startup with no revenue?

Yes. SBA Microloans through CDFIs, equipment-specific lenders that use the truck as collateral, and some alternative lenders all work with startups. A solid business plan with revenue projections significantly improves your chances.

What is the typical loan term for food truck financing?

Most food truck equipment financing loans run 3 to 7 years. SBA Microloans max out at 7 years. Shorter terms mean higher monthly payments but less total interest paid over the life of the loan.

You now have everything you need to move forward confidently. Whether you’re a first-time operator with limited credit or an established business owner expanding your fleet, the right food truck equipment financing option exists for your situation. Compare lenders, run your numbers with our equipment financing calculator, and apply with your documents ready. Your mobile kitchen is closer than you think.

Founder of Nanotom Capital & Nanotom Labs