Key Takeaways

- New semi-trucks cost $130,000–$275,000; used units run $60,000–$160,000; trucking equipment financing spreads those costs over 24–84 months, with 60-month terms being most common.

- Rates range from 4%–8% at traditional banks to 8%–35% at online lenders; anything under 10% is considered a strong rate in trucking, and a 670+ credit score is the key threshold to get there.

- Most lenders cap used Class 8 semi financing at 10 years old and 700,000 miles; exceed either limit and specialty trucking lenders become your only realistic option.

- The 2025 Section 179 deduction limit is $2,500,000, and most Class 6, 7, and 8 trucks qualify for the full deduction; financing instead of paying cash delivers the same tax benefit while keeping $50,000–$150,000 liquid in your business.

- Owner-operators are underwritten primarily on personal FICO score (580+ minimum), while fleet operators must show a debt service coverage ratio (DSCR) of at least 1.25x to get approved.

- Startups can still qualify through specialty lenders with no time-in-business requirement; CDL experience, a 25%+ down payment, and signed freight contracts are the strongest compensating factors.

- According to the American Trucking Associations, 91.5% of U.S. trucking carriers operate 10 or fewer trucks, meaning most lenders , especially specialty trucking lenders, are built to underwrite small operators, not just large fleets.

Most trucking businesses don’t fail because of bad routes or slow freight markets. They fail because they can’t afford the equipment to run. Trucking equipment financing solves that problem by putting trucks and trailers in your hands now, with payments spread over time.

This guide covers everything from rate ranges and lender requirements to tax strategies and application steps. Nothing’s left out.

What Is Trucking Equipment Financing?

Trucking equipment financing is a category of business lending where the truck, trailer, or heavy equipment itself serves as collateral. That’s the key difference from a general business loan. Lenders are securing their risk against a physical asset, which typically means easier approvals and better rates than unsecured borrowing.

The need is real. According to the American Trucking Associations (ATA, 2024), trucking moves 72.7% of all U.S. freight by weight and generates $906 billion in annual revenue. Fleet access isn’t a luxury. It’s an operational requirement.

New semi-trucks run $130,000–$275,000+. Used units still range from $60,000–$160,000. For most operators, truck equipment financing isn’t just practical; it’s the only viable path to growth. If you’re new to asset-based lending, start with our equipment financing basics guide before going deeper.

Types of Trucking Equipment You Can Finance

Trucking equipment financing covers a wide range of assets. Here’s what most lenders will fund and what each category typically costs.

Semi-Trucks and Tractor-Trailers

This is the core of most fleets. New units run $130,000–$275,000 depending on make, spec, and configuration. Used semi-trucks fall in the $60,000–$160,000 range, though age and mileage restrictions apply with most lenders.

Flatbed and Specialty Trailers

Lower cost than power units, but critical for load flexibility. Flatbeds, step-decks, and lowboys typically run $20,000–$80,000. Truck equipment financing for trailers alone is common and straightforward to qualify for.

Refrigerated (Reefer) Units

Reefer trailers cost more upfront, $40,000–$100,000+, and carry higher maintenance needs due to the cooling systems. Lenders factor that in. Rates can run slightly higher to offset residual value risk.

Vocational and Work Trucks

Dump trucks, tankers, and tow trucks serve specific industries and are often easier for startups to finance. Their purpose-built nature makes collateral valuation simpler. If your work crosses into construction, our heavy equipment financing guide covers overlapping asset types.

Best Trucking Equipment Financing Options

There are six main trucking equipment financing options: equipment loans, equipment leasing (operating or lease-to-own), equipment refinancing, equipment debt consolidation, working capital loans, and accounts receivable financing. Each serves a different stage and cash flow situation.

Equipment Loans

The most straightforward structure. You borrow against the truck’s value, make fixed monthly payments, and own it outright at payoff. Terms typically run 24–84 months, and rates start around 5.5% for strong credit.

This works for both new and used equipment financing, though lenders impose age and mileage caps on older units.

Equipment Leasing: Operating vs. Lease-to-Own

Most guides treat leasing as one product. It’s not.

Operating lease: You use the truck, return it at term end. Lower monthly payments. The full payment is deductible as an operating expense, and there’s no depreciation on your books.

Finance lease (lease-to-own): Treated like ownership from day one. You claim depreciation and interest deductions, it’s Section 179 eligible, and it ends with a $1 buyout. Best for operators who want ownership benefits without a large down payment upfront.

See our full equipment leasing vs. financing comparison to pick the right structure.

Equipment Refinancing

Already own trucks with equity? Refinancing pulls cash out or lowers your rate. It’s especially useful when rates drop or your credit profile has improved significantly since the original loan closed.

Equipment Debt Consolidation

Multiple truck payments across different lenders create cash flow chaos. Consolidation rolls them into one payment, often at a lower blended rate. Fleet operators with 5+ units use this regularly.

Working Capital Loans

Truck equipment financing covers the asset. Working capital covers everything else: fuel, insurance, driver payroll, repairs. Terms are shorter (6–24 months) and rates higher, but approval is fast.

Accounts Receivable Financing

Freight brokers pay slow. AR financing (or factoring) advances 80–95% of your outstanding invoices immediately, no new debt on the balance sheet. It’s common among owner-operators waiting 30–60 days on broker payments.

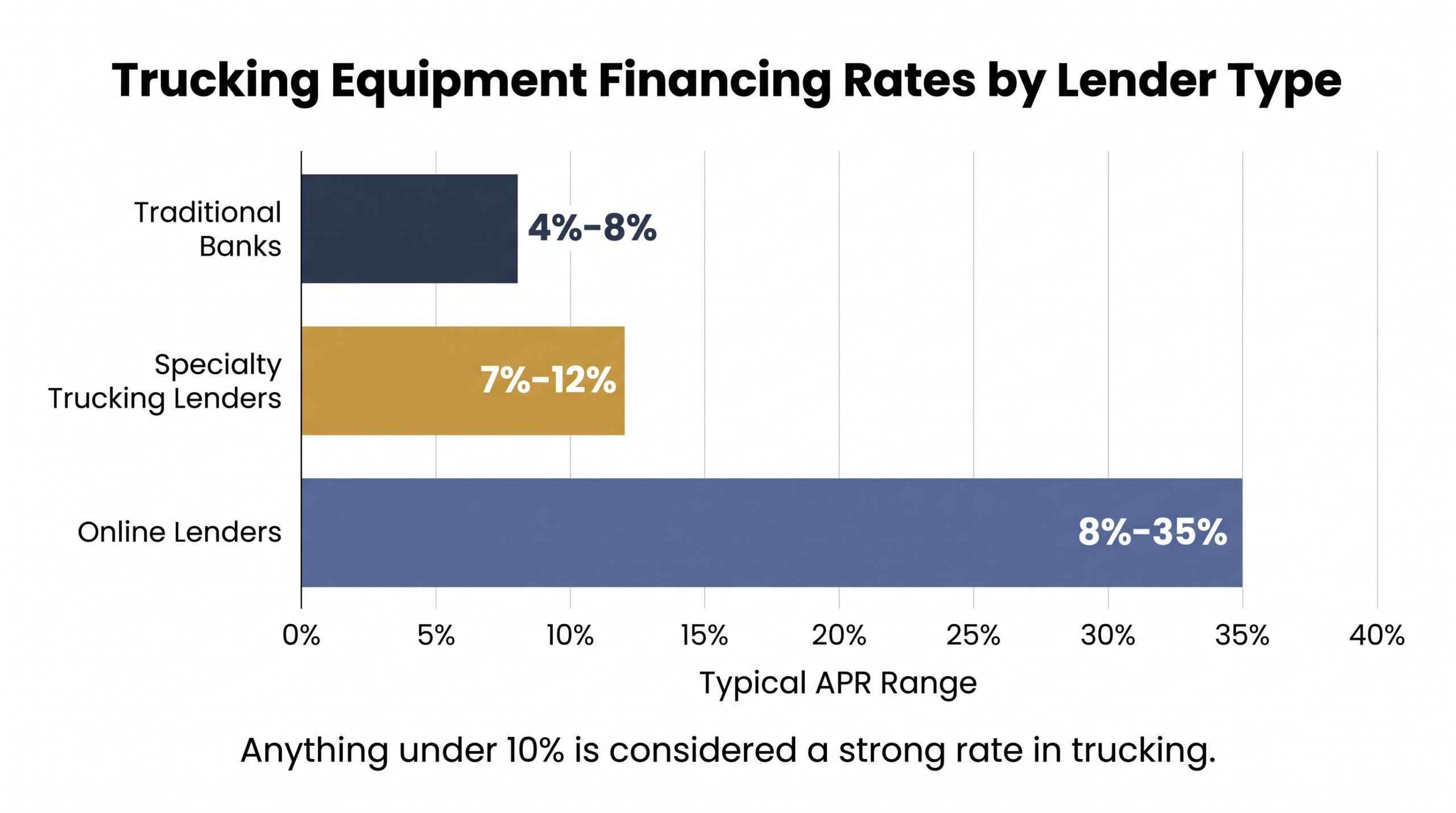

Trucking Equipment Financing Rates: What to Expect

Here’s what most guides won’t tell you: most competitors won’t publish real rate ranges. Here’s what the market actually looks like for truck equipment financing in 2024 (sources: Bankrate, Crestmont Capital, Bay Street Lending).

| Lender Type | Typical APR | Best For |

|---|---|---|

| Traditional Banks | 4%–8% | Established fleets, strong credit |

| Specialty Trucking Lenders | 7%–12% | Owner-operators, 2+ years in business |

| Online Lenders | 8%–35% | Startups, lower credit profiles |

New truck loans for well-qualified borrowers run 5%–12%. Used truck loans carry more risk for lenders, pushing rates to 7%–18%. Anything under 10% is a strong rate in trucking.

Four factors drive your rate more than anything else:

- Credit score: 670+ unlocks sub-10% rates. Below 620, expect 12%–25%.

- Time in business: 2+ years gets you significantly better terms than a startup.

- Down payment: 10%–20% is standard. Put more down, get a lower rate.

- Truck age and condition: Older, higher-mileage units mean higher lender risk and higher rates.

For a deeper breakdown on rate strategy, see our equipment financing rates guide.

New vs. Used Truck Financing: What to Know

The new vs. used decision isn’t just about price. It affects your rate, down payment requirement, and which lenders will even talk to you.

New trucks are the easier finance path. Rates run 5%–12%, down payments start at 10%, and you get full Section 179 eligibility. Lenders love new collateral.

Used trucks are where most operators actually shop, and where trucking equipment financing gets more complicated. Expect 7%–18% APR and down payment requirements of 15%–25%. Most major lenders cap used Class 8 semis at 10 years old and 700,000 miles. Go beyond those thresholds and traditional banks will decline outright.

Specialty trucking lenders may stretch to 15–20 years, but they’ll want larger down payments and tighter terms to offset the risk. Practical rule: if the truck is older than 7 years or past 500,000 miles, skip the banks entirely. Specialty lenders built their truck equipment financing products for exactly that scenario.

For a full breakdown on financing pre-owned assets, our used equipment financing guide covers everything lenders look at before approving older units.

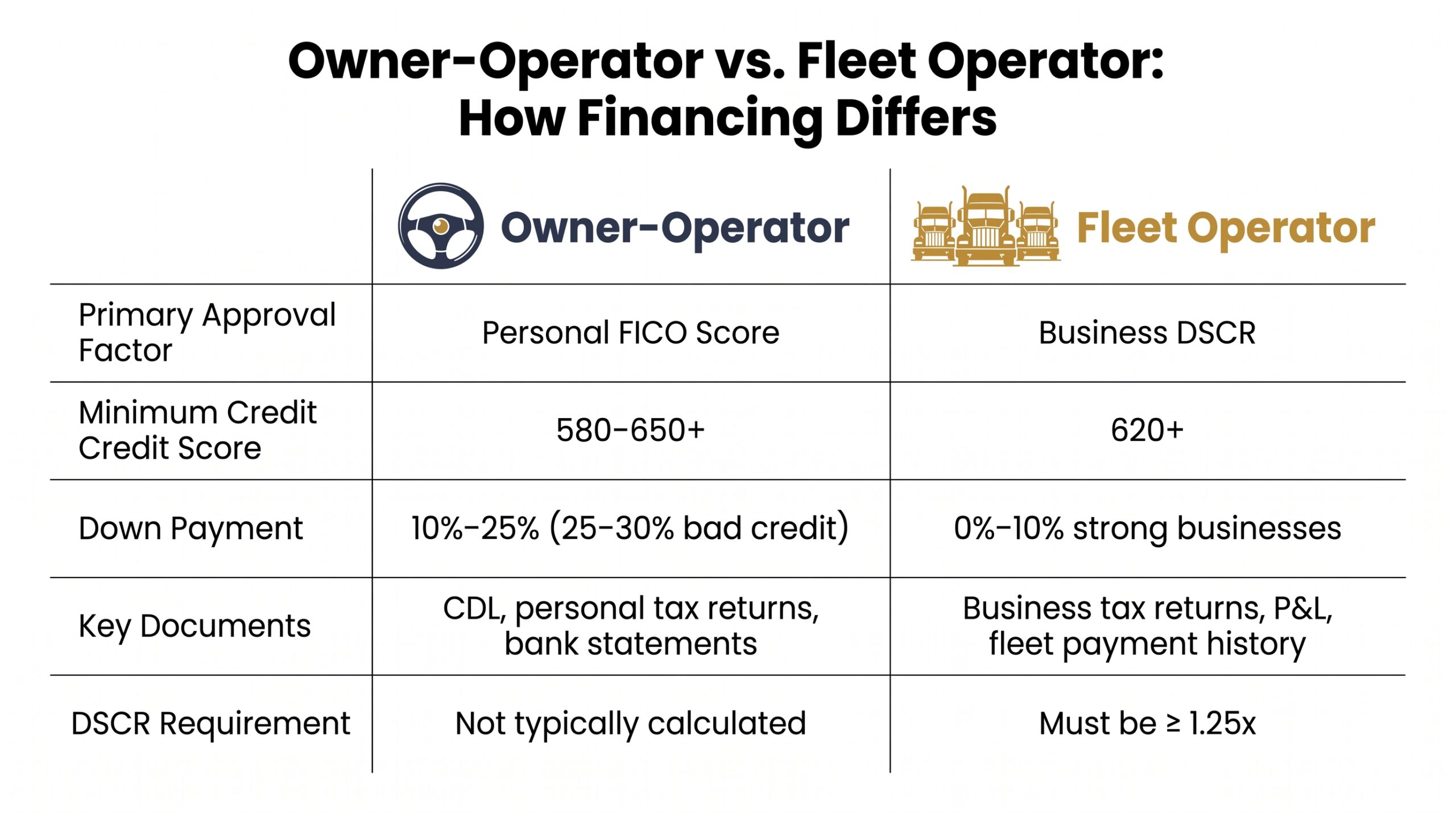

Owner-Operators vs. Fleet Operators: How Financing Differs

Trucking equipment financing isn’t one-size-fits-all. How lenders underwrite your deal depends almost entirely on which category you fall into.

| Requirement | Owner-Operator | Fleet Operator |

|---|---|---|

| Primary approval factor | Personal FICO score | Business financials (DSCR) |

| Minimum credit score | 580–650+ depending on lender | 620+ (business credit weighted) |

| Down payment | 10%–25% (25%–30% for bad credit) | 0%–10% for strong businesses |

| Key documents | CDL, personal tax returns, bank statements | Business tax returns, P&L, fleet payment history |

| DSCR requirement | Not typically calculated | Must be ≥ 1.25x |

Owner-operators: Your CDL tenure matters more than you might expect. Lenders treat driving experience like business experience; two or more years behind the wheel improves approval odds significantly, even with a mid-range credit score.

Fleet operators: Your existing fleet’s payment history is a major approval signal. Clean payment records on current truck equipment financing agreements tell lenders you manage asset debt responsibly. A DSCR below 1.25x will stall most fleet-level applications regardless of revenue.

How to Qualify for Trucking Equipment Financing

91.5% of U.S. trucking carriers operate 10 or fewer trucks (ATA, 2024). Most applicants are small operators, not corporations. Lenders know this, and qualification requirements reflect it.

Credit Score Requirements

580+ gets you in the door with specialty trucking lenders. 650+ is the threshold for banks and SBA programs. Hit 670+ and you’re competing for sub-10% rates. Below 580, expect significant down payment requirements or a co-signer conversation.

Time in Business and Revenue

Two or more years is the conventional standard. Under a year is still possible through specialty lenders who underwrite on CDL experience and equipment value rather than business history.

See our startup equipment financing guide if you’re a new carrier. Fleet operators need a DSCR of 1.25x or higher.

Down Payment Requirements

Good credit: 10%–20%. Bad credit or short history: 20%–30%. Some strong fleet operators qualify for 0% down. Higher down payments directly reduce your rate and monthly payment.

Documents You’ll Need

- 3–6 months business bank statements

- 2 years business tax returns

- Profit and loss statement

- Equipment invoice or purchase agreement

- CDL and driver history (owner-operators)

Bad Credit and Startup Trucking Financing Options

The honest answer is that conventional lenders aren’t your only path. Specialty trucking lenders like CAG Truck Capital and Taycor Financial approve credit scores as low as 550 with no time-in-business minimum. Rates will be higher (15%–30%) and terms shorter, but trucking equipment financing is still accessible.

Lenders in this space compensate for weak credit by leaning on other approval factors:

- Larger down payment: 25%+ signals commitment and reduces lender risk immediately.

- Strong bank statements: 3–6 months of consistent deposits matter more than your score alone.

- Signed freight contracts: Proof of future revenue is a powerful compensating factor.

- CDL experience: Years behind the wheel substitute for years in business.

- Vocational truck type: Dump trucks, tankers, and tow trucks are easier to approve than OTR sleepers for startups.

If your credit situation is severe, explore our no credit check equipment financing options for alternative structures that don’t rely on FICO at all.

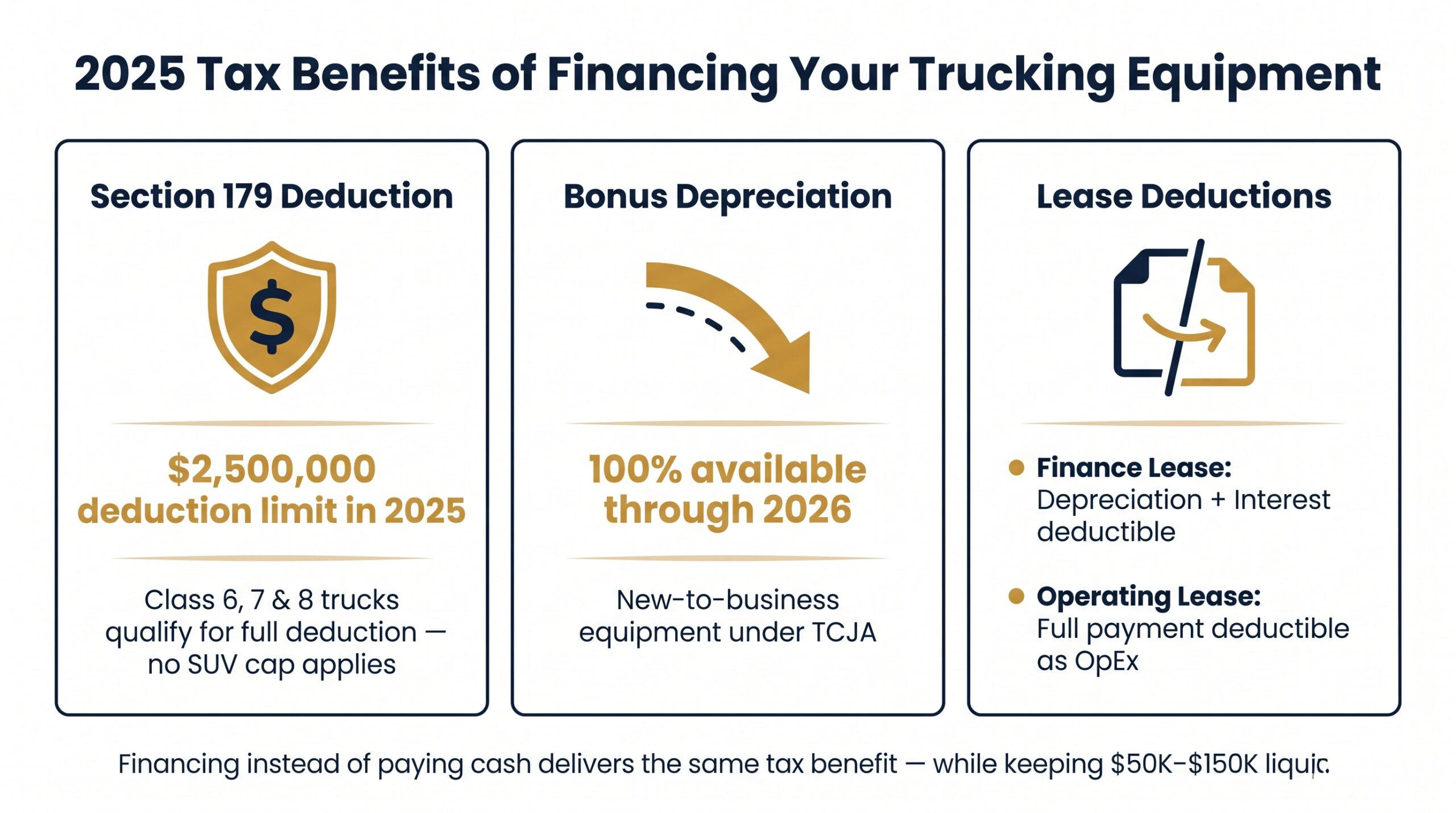

Tax Benefits of Financing Your Trucking Equipment

Here’s what most guides skip entirely: financing your truck instead of paying cash can deliver identical tax benefits while keeping $50,000–$150,000 liquid in your business. That’s not a small thing.

Section 179 Deduction

According to Section179.org, the 2025 Section 179 limit is $2,500,000 for qualifying property. Heavy commercial trucks over 14,000 lbs GVWR are not subject to the $31,300 SUV cap, and most Class 6, 7, and 8 trucks qualify for the full deduction. The truck must be placed in service by December 31, 2025.

Bonus Depreciation

Under the Tax Cuts and Jobs Act, 100% bonus depreciation remains available through 2026 for new-to-business equipment. Stack this with Section 179 strategically and you can write off a significant portion of your truck’s cost in year one.

Lease Deductions

Finance leases allow depreciation plus interest deductions. Operating leases let you deduct the full payment as an operating expense. Either way, trucking equipment financing preserves working capital while still generating the write-off.

Always verify specifics with a qualified tax professional (IRS Publication 946). For a broader overview of how asset financing works, see our equipment financing explained guide.

Real-World Example: Choosing the Right Financing for Your Fleet

The following is an illustrative scenario based on typical borrower profiles and current market rates.

Meet Maria. Owner-operator, 660 credit score, 3 years in business, $180,000 annual revenue. She wants to add a second truck, a 2019 Freightliner Cascadia priced at $120,000.

Here’s how her trucking equipment financing deal looks:

- Best product: Equipment loan (she wants ownership, not a lease)

- Estimated APR: 7%–12% (660 score + specialty lender = mid-range rate)

- Down payment: 10%–15% = $12,000–$18,000

- Monthly payment: ~$2,490/month ($120,000 at 9% over 60 months)

- Tax play: 2019 truck qualifies for Section 179 if under lender age thresholds

- Lender recommendation: Specialty trucking lender, not a bank

Maria’s $2,490 monthly payment needs to be covered by the revenue the second truck generates. If her lanes produce $6,000–$8,000/month per truck, the math works comfortably.

Want to run your own numbers? Use our equipment financing calculator to model any truck equipment financing scenario before you apply.

How to Choose the Right Trucking Financing Partner

Not all lenders understand trucking. Choosing the wrong one costs you time, money, and sometimes the deal entirely.

| Lender Type | Rate Range | Best For |

|---|---|---|

| Banks | 4%–8% | Strong credit, established businesses |

| Credit Unions | 5%–9% | Members with good credit |

| Specialty Trucking Lenders | 7%–12% | Most operators, faster decisions |

| OEM Financing (Kenworth, Paccar) | Promotional to 10% | New truck buyers, manufacturer deals |

| Online Lenders | 8%–35% | Fast approvals, broader credit acceptance |

For most operators, specialty trucking lenders are the default recommendation. They understand seasonal cash flow, mileage-based depreciation, and used truck collateral in ways banks simply don’t.

When you’re evaluating any truck equipment financing partner, look for 24–48 hour approval timelines, transparent fee structures, no harsh prepayment penalties, and loan terms that don’t outlast the equipment’s useful life.

Compare top lenders in detail via our best equipment financing companies guide, or learn how equipment financing brokers can shop multiple lenders simultaneously on your behalf.

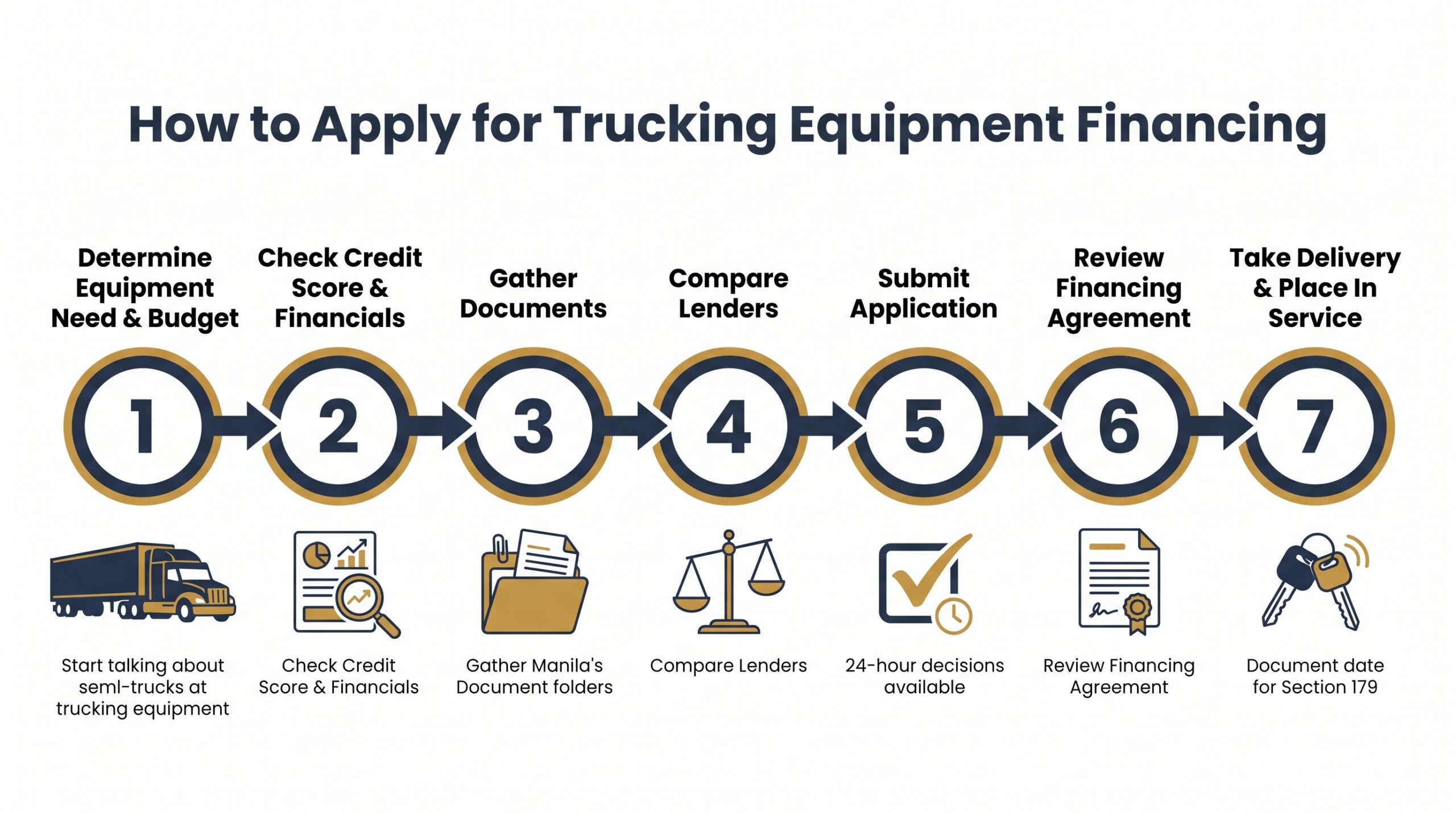

How to Apply for Trucking Equipment Financing: Step-by-Step

- Determine your equipment need and budget. New vs. used, truck type, and price range. These decisions shape which lenders and products are even relevant to you.

- Check your credit score and business financials. Know your FICO, DSCR, and time in business before any lender sees them. No surprises.

- Gather your documents. 3–6 months of bank statements, 2 years of tax returns, equipment invoice, and CDL records if you’re an owner-operator.

- Compare lenders based on your profile. Strong credit goes to banks. Newer business or lower score goes to specialty trucking lenders or online lenders.

- Submit your application. Many specialty lenders offer same-day or 24-hour decisions on truck equipment financing.

- Review the financing agreement carefully. Fixed vs. variable rate, total cost of capital, prepayment penalties, balloon payment terms, read our equipment financing agreement guide before signing anything.

- Take delivery and place equipment in service. Document the date for Section 179 deduction purposes; the IRS requires the asset be in service by December 31.

Trucking Equipment Financing: Frequently Asked Questions

What credit score do I need for truck financing?

580–650 minimum depending on lender type. Specialty lenders start at 580; banks and SBA programs want 650+. Hit 670+ and you’re unlocking sub-10% rates.

Can I finance a used semi-truck?

Yes. Most lenders cap used Class 8 trucks at 10 years old and 700,000 miles. Specialty lenders are more flexible on both thresholds if the collateral value supports it.

How much is a down payment on a semi-truck?

10%–20% for good credit. 20%–30% if you have bad credit or limited business history. Some strong operators qualify for 0% down.

Can a startup trucking company get equipment financing?

Yes, through specialty lenders with no time-in-business requirement. Expect higher rates (15%–30%) and larger down payments. CDL experience and signed freight contracts help significantly.

Is it better to lease or buy a semi-truck?

Operating leases offer lower payments and flexibility. Finance leases and loans build equity and unlock Section 179 depreciation deductions. Most owner-operators who want long-term ownership are better served by a loan.

What is the typical loan term for trucking equipment financing?

24–84 months is the standard range. 60-month terms are most common for semi-trucks. Longer terms lower monthly payments but increase total interest paid.

Can I deduct financed truck payments on my taxes?

Loan interest is deductible. Financed equipment is eligible for Section 179 up to $2,500,000 in 2025, regardless of whether you paid cash or financed. Operating lease payments are fully deductible as a business expense.

Ready to move forward? Nanotom Capital works with owner-operators, small fleets, and growing carriers at every stage of the financing process. Whether you’re buying your first truck or adding your tenth, we’ll match you with the right truck equipment financing structure for your credit profile, cash flow, and long-term goals. Apply today and get a decision in as little as 24 hours.

Founder of Nanotom Capital & Nanotom Labs