Key Takeaways

- Equipment financing rates range from 4% to 25% APR in 2026. Your credit score is the single biggest lever, with 700+ unlocking the 4%–8% tier and below 650 pushing rates toward 20%–25%.

- A $50,000 loan at 8% APR over 60 months costs $1,013.82 per month and generates $10,829 in total interest. Knowing this math before you meet a lender is a negotiating advantage.

- Jumping from 6% to 15% APR on a $100,000 loan adds over $400 per month, totaling nearly $25,000 in extra interest over a 60-month term.

- Longer loan terms lower your monthly payment but dramatically increase total cost. A $75,000 loan at 10% over 36 months costs ~$8,600 in interest; stretch it to 72 months, and that climbs to ~$17,500.

- Section 179 allows businesses to deduct up to $1,250,000 in qualifying equipment purchases in 2026, potentially saving $25,000 in taxes on a $100,000 purchase at a 25% effective tax rate.

- Pre-qualification uses a soft credit pull with zero impact on your score. A hard pull only triggers when you formally apply and can temporarily lower your score by up to 5 points.

- Startups and credit-challenged businesses should budget for 20%–35% down regardless of lender type, while excellent-credit borrowers can often secure 100% financing on new equipment.

Most businesses burn hours shopping for equipment loans without knowing what they can actually afford. An equipment financing calculator solves that problem immediately; it gives you a real monthly payment estimate before you talk to a single lender. Use the tool below, then keep reading to understand exactly what drives your number and how to get the best rate possible. If you’re new to the topic, start with our explainer on what equipment financing is before diving into the numbers.

How to Use the Equipment Financing Calculator

This equipment financing calculator runs on the standard amortization formula and produces your estimated monthly payment in seconds. Four inputs. No signup required.

Step 1: Enter Your Equipment Cost

Type in the total purchase price of the equipment. If you’re making a down payment, subtract that amount first and enter only what you plan to finance.

Step 2: Input Your Estimated Interest Rate

Use your best current estimate. Most equipment loans run between 6% and 30% APR depending on your credit profile and lender type. Not sure where you’ll land? Start with 10% as your baseline.

Step 3: Select Your Loan Term

Choose how many months you want to repay the loan. Terms typically range from 24 to 84 months. Longer terms lower your monthly payment but increase total interest paid; we’ll get into exactly how much that difference adds up to shortly.

Step 4: Read Your Estimated Monthly Payment

The financing equipment calculator displays your monthly payment instantly. That figure becomes your baseline for budgeting, lender comparisons, and Section 179 tax planning. Real numbers, real fast.

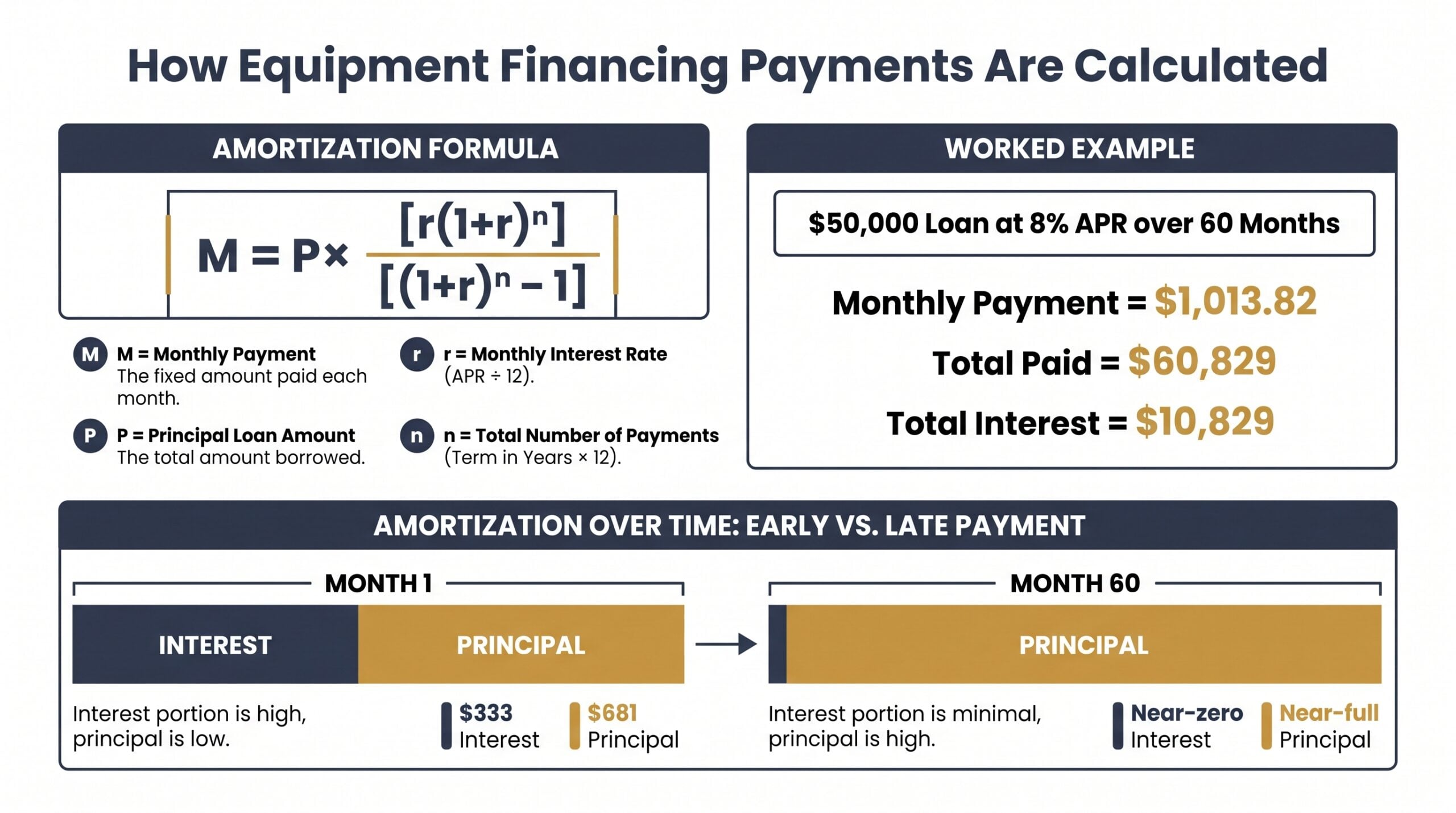

How Equipment Financing Payments Are Calculated

An equipment financing calculator estimates your monthly payment based on three inputs: loan amount, annual interest rate, and loan term. A $50,000 equipment loan at 7% interest over 60 months produces an estimated monthly payment of approximately $990. Change any one of those three variables and your payment shifts accordingly.

The Loan Payment Formula

Every financing equipment calculator runs the same standard amortization formula under the hood:

M = P × [r(1+r)^n] / [(1+r)^n – 1]

- M = monthly payment

- P = principal (total loan amount)

- r = monthly interest rate (APR ÷ 12)

- n = total number of payments (loan term in years × 12)

Here’s a worked example. You’re financing $50,000 at 8% APR over 60 months. Your monthly rate is 8% ÷ 12 = 0.6667%. Plug those numbers in and your estimated monthly payment is $1,013.82.

Over the full term, you’ll pay roughly $60,829 total, meaning $10,829 goes purely to interest. That’s not a small number, and it’s exactly why running scenarios before you commit matters.

What Each Input Means for Your Business

Here’s what most guides skip: amortization isn’t linear. Your first payment on that $50,000 loan applies about $333 to interest and $681 to principal. By month 60, nearly the entire payment is principal. This is why paying off equipment loans early saves real money; you’re cutting off the interest-heavy end of the schedule.

Knowing this math means you’re not guessing when you sit across from a lender. Use the equipment financing calculator above to test different rate and term combinations before you commit to anything.

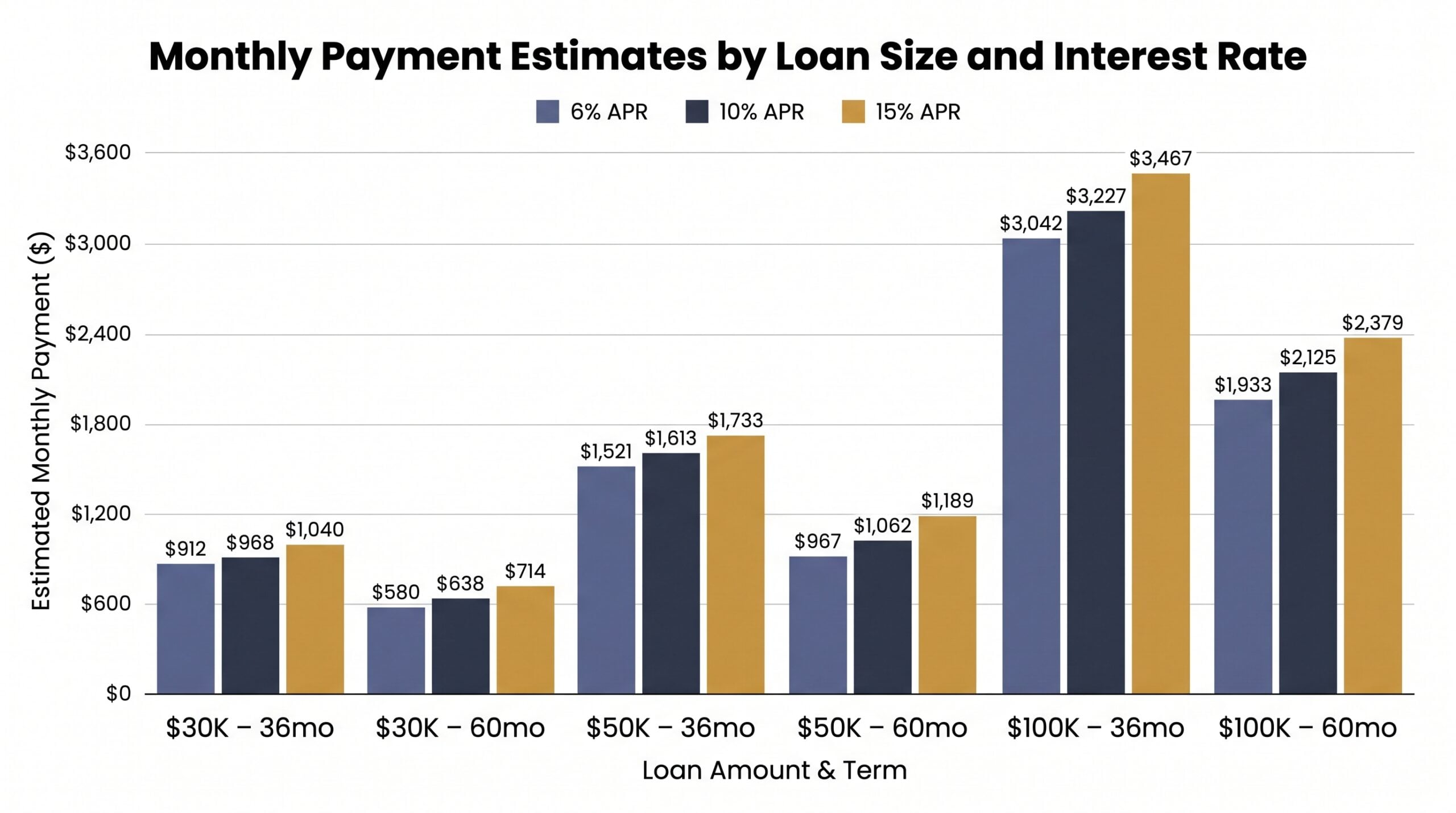

Sample Monthly Payment Estimates

The tables below give you real payment benchmarks across common loan sizes, rate tiers, and terms. All figures use the standard amortization formula.

Your actual rate depends on your credit profile, lender, and equipment type, so treat these as informed starting points rather than guarantees.

$30,000 Equipment Loan Payment Examples

| Interest Rate | 36-Month Term | 60-Month Term |

|---|---|---|

| 6% APR | $912/mo | $580/mo |

| 10% APR | $968/mo | $638/mo |

| 15% APR | $1,040/mo | $714/mo |

$50,000 Equipment Loan Payment Examples

| Interest Rate | 36-Month Term | 60-Month Term |

|---|---|---|

| 6% APR | $1,521/mo | $967/mo |

| 10% APR | $1,613/mo | $1,062/mo |

| 15% APR | $1,733/mo | $1,189/mo |

$100,000 Equipment Loan Payment Examples

| Interest Rate | 36-Month Term | 60-Month Term |

|---|---|---|

| 6% APR | $3,042/mo | $1,933/mo |

| 10% APR | $3,227/mo | $2,125/mo |

| 15% APR | $3,467/mo | $2,379/mo |

Notice how jumping from 6% to 15% on a $100,000 loan adds over $400 per month at the 60-month term. That’s nearly $25,000 extra over the life of the loan. Rate shopping isn’t optional; it’s one of the highest-leverage decisions you’ll make in this process.

Need a figure that isn’t in these tables? The equipment financing calculator at the top of this page handles any combination instantly. Plug in your exact numbers and get a custom estimate in seconds.

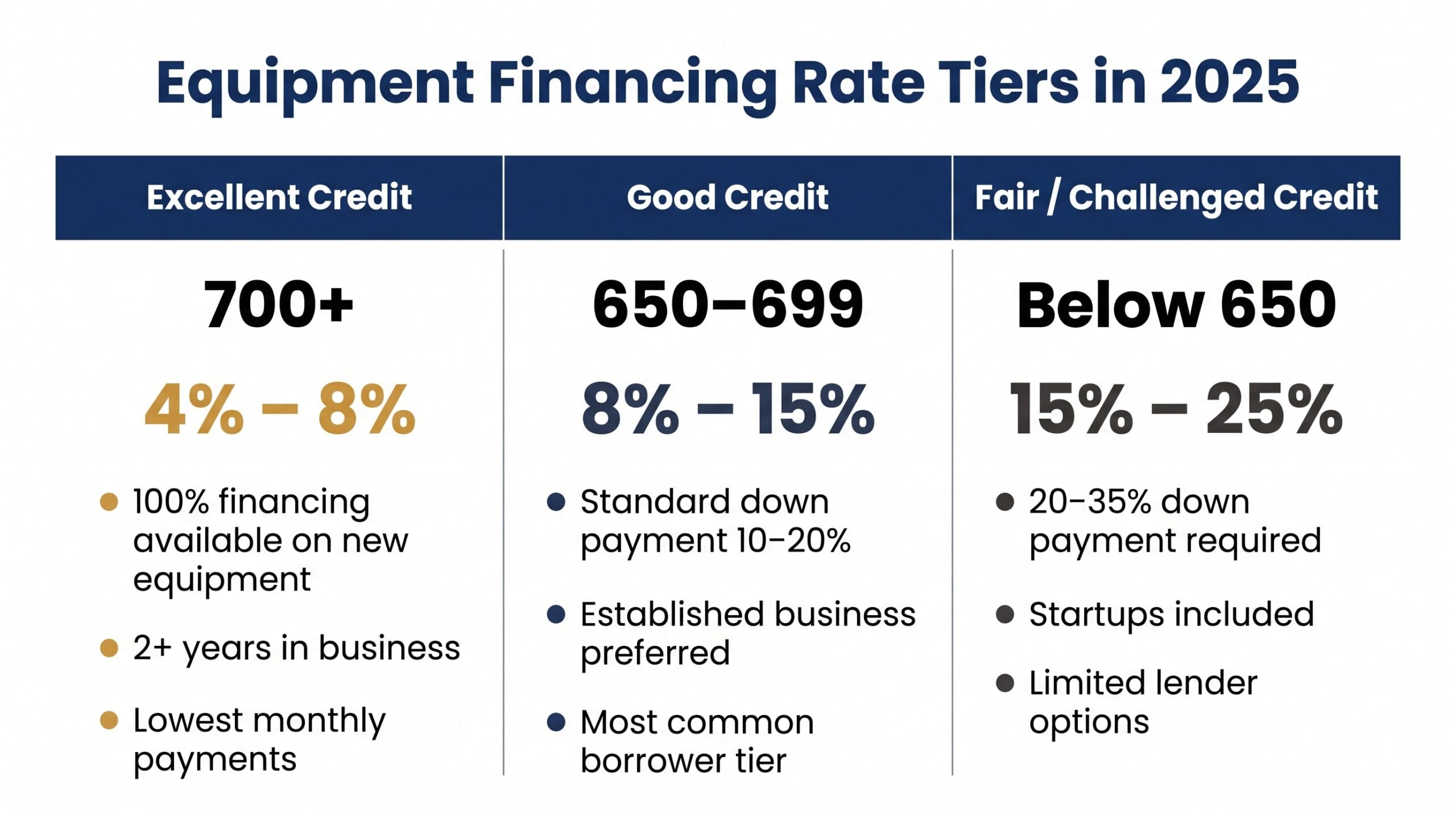

Equipment Financing Rates: What to Expect

Equipment financing rates in 2025 range from 4% to 25% APR, according to Biz2Credit’s equipment financing rate data. That’s a massive spread, and it’s driven almost entirely by your credit profile, business history, and the lender you choose. Running your numbers through an equipment financing calculator before approaching lenders puts you in a stronger negotiating position from the start.

Typical Rate Ranges in 2025

| Credit Profile | Credit Score | Typical APR Range |

|---|---|---|

| Excellent | 700+ | 4% – 8% |

| Good | 650 – 699 | 8% – 15% |

| Fair / Challenged | Below 650 | 15% – 25% |

Most established businesses with two or more years of operating history land in that 8%–15% range. Startups and businesses with credit blemishes should budget toward the higher end when using a financing equipment calculator to stress-test affordability.

What Affects Your Rate

Lenders weigh several factors when pricing your loan, and each one can move your rate meaningfully in either direction.

- Credit score: The single biggest lever. Below 650 and your options narrow fast.

- Time in business: Two years is the standard threshold. Under that, expect higher rates or stricter terms.

- New vs. used equipment: New equipment typically secures better rates since it holds collateral value longer.

- Loan amount and term: Larger loans with shorter terms often attract lower rates.

- Lender type: Banks offer the lowest rates but the strictest approval criteria. Online lenders move faster but charge more.

For a deeper breakdown of current market rates by lender and equipment category, see our equipment financing rates guide. Then come back and run your realistic rate through the equipment financing calculator above to see what it actually costs monthly.

Factors That Affect Your Equipment Financing Rate

The rate table above gives you a starting point. These are the variables that actually move you up or down within those ranges, and a few of them might surprise you.

Credit Score and Business History

Most lenders want a 650+ credit score at minimum. Hit 700+ and you’re competing for the best rates on the market. Drop below 600 and your lender pool shrinks significantly, with rates climbing toward 20–25% APR.

Time in business matters just as much as your score. Two years is the standard cutoff. Startups typically face higher rates and steeper down payment requirements (often 20–35% upfront) to offset lender risk. Newer businesses should review our dedicated guide to startup equipment financing for options tailored to early-stage companies.

Equipment Type: New vs. Used

New equipment frequently qualifies for 100% financing at rates between 5–8% APR because it holds strong collateral value. Used equipment is a different story.

Expect rates starting around 6–8.5% for recent models, with lenders requiring 15–35% down on equipment more than 10 years old. If you’re evaluating older or pre-owned machinery, our used equipment financing guide covers the full approval picture. Use the financing equipment calculator to compare new versus used payment scenarios side by side.

Loan Amount and Term Length

The honest answer on loan terms is that longer almost always costs you more; the monthly savings are real, but so is the interest you’re adding. A $75,000 loan at 10% over 36 months costs roughly $8,600 in interest. Stretch that to 72 months and you’re paying closer to $17,500.

Run both scenarios through the equipment financing calculator before deciding. Seeing the actual dollar difference tends to sharpen the decision quickly.

Lender Type: Banks, Credit Unions, and Online Lenders

Banks offer the lowest rates but require strong financials, clean credit, and patience. Credit unions sit in the middle, often offering competitive rates to members with solid profiles. Online lenders approve faster and work with lower credit scores, but their rate ceilings are higher. See how leading providers stack up in our roundup of the top equipment financing lenders.

Down payment expectations follow the same pattern. Excellent credit borrowers often put 0–10% down. Standard applicants budget 10–20%. Startups and credit-challenged businesses should plan for 20–35% regardless of lender type.

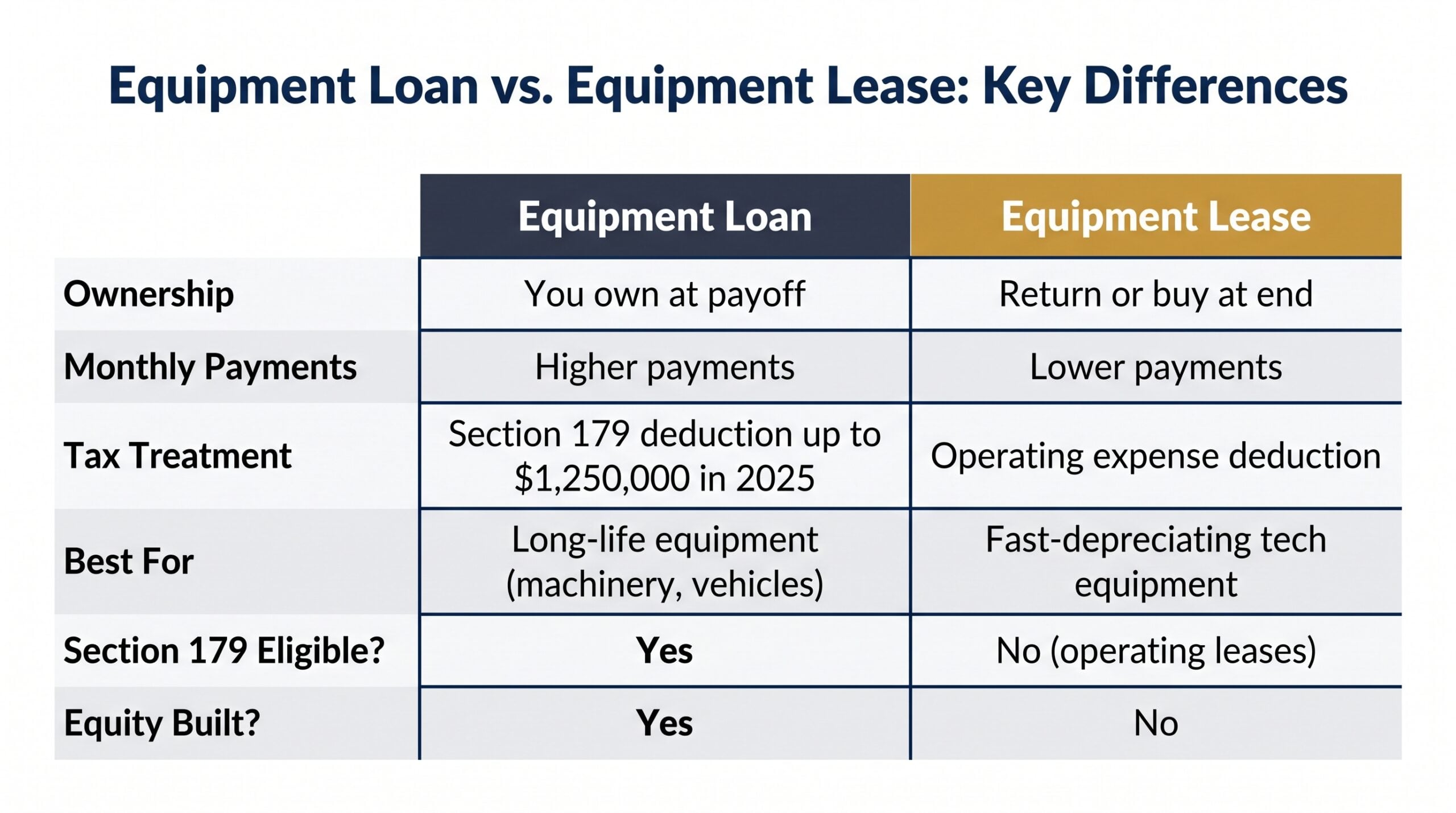

Equipment Loan vs. Equipment Lease: Which Is Right for You?

Your monthly payment is only part of the decision. Whether you finance or lease changes what you own, what you can deduct, and what flexibility you have when the term ends. These aren’t minor differences; they can reshape the total cost of the equipment significantly.

When to Choose a Loan

A loan makes sense when the equipment has a long useful life, holds residual value, or sits at the core of your operations. You own it outright at payoff, build equity, and can sell or trade it later. Heavy machinery, vehicles, and manufacturing equipment typically fall into this category.

When to Choose a Lease

Leasing works better for technology equipment that depreciates fast. Monthly payments are lower, you treat payments as an operating expense, and upgrading at lease-end is straightforward. The tradeoff is real though; you’re building no equity and returning the equipment when the term ends.

For a full side-by-side breakdown, see our equipment leasing vs. financing guide. Both options have genuine merit, and the right answer depends heavily on your cash flow and tax situation.

Section 179 Tax Deduction Advantage for Equipment Buyers

This is where financing beats leasing on paper for many businesses. Under Section 179, businesses that purchase and finance equipment may deduct up to $1,250,000 in qualifying equipment purchases in tax year 2025, according to Section179.org. That deduction applies in the year the equipment is placed in service, not spread over years of depreciation.

A $100,000 equipment purchase at a 25% effective tax rate produces a $25,000 tax savings, effectively dropping your real equipment cost to $75,000. Run that adjusted figure through the equipment financing calculator to see how dramatically your true cost of ownership shifts.

One important caveat: Section 179 applies to purchases, not operating leases. And every business situation is different, so talk to a tax professional before making decisions based on this deduction.

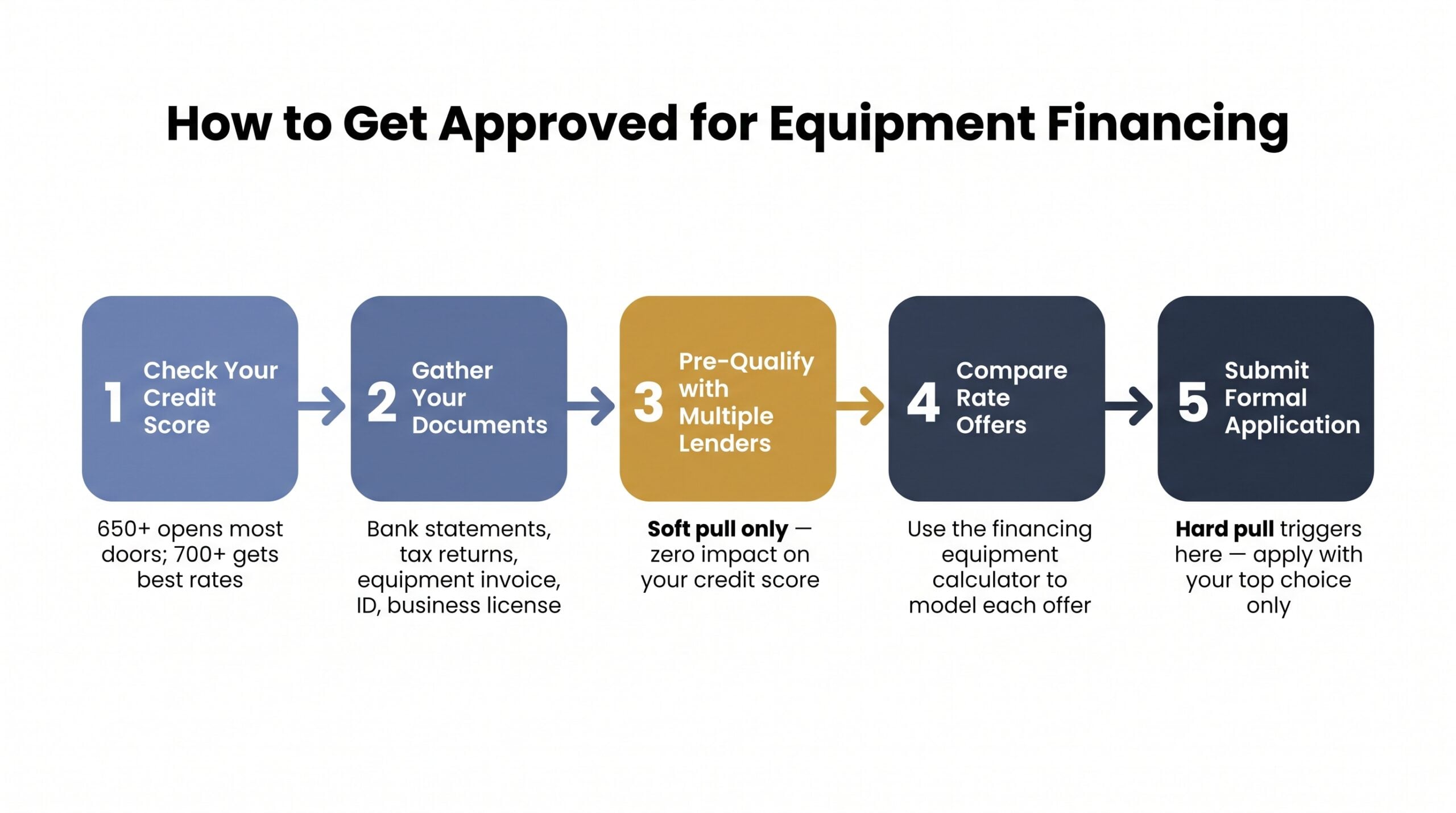

How to Get Approved for Equipment Financing

Knowing your estimated monthly payment from the equipment financing calculator is step one. Getting approved is a different exercise, and it helps to understand what lenders are actually evaluating before you walk in.

What Lenders Look For

Every lender weighs roughly the same set of factors, just with different thresholds.

- Credit score: Both personal and business credit get reviewed. 650+ opens most doors; 700+ gets you the best terms.

- Time in business: Two years is the standard minimum. Under that, expect additional scrutiny.

- Annual revenue: Most lenders want to see revenue that comfortably covers the new payment obligation.

- Equipment details: Type, age, and estimated value all factor in. Newer equipment with strong resale value is easier to finance.

- Down payment: Having 10–20% ready signals financial stability and reduces lender risk.

Soft Pull vs. Hard Pull: How Lenders Check Your Credit

Most lenders run a soft credit pull during pre-qualification. Soft pulls don’t affect your credit score at all, which means you can shop rates across multiple lenders at this stage without any penalty. That’s exactly what you should do before committing to anything.

A hard pull only happens when you formally apply and authorize it. According to the Consumer Financial Protection Bureau, hard inquiries can lower your score by up to 5 points temporarily, so apply with one lender at a time once you’ve narrowed your options down.

If your credit situation is complicated, our equipment financing with no credit check guide covers alternative approval paths worth knowing about.

Documents You’ll Typically Need

Getting these ready before you apply speeds up approval significantly, and it signals to lenders that you’re organized and serious.

- Three months of recent business bank statements

- Business tax returns (last 1–2 years)

- Equipment invoice or purchase quote

- Government-issued ID

- Business license or formation documents

Having a purchase quote in hand also means you’re entering accurate numbers into the financing equipment calculator, so your payment estimates reflect reality rather than guesswork. Before you sign anything, make sure you understand your equipment financing agreement in full.

Frequently Asked Questions

What is the interest rate for equipment financing?

Equipment financing rates typically range from 4% to 25% APR in 2025. Borrowers with 700+ credit scores and two or more years in business generally qualify for 4%–8%. Most established businesses land in the 8%–15% range. Credit-challenged applicants or startups should budget for 15%–25%.

How much is the monthly payment on a $50,000 business loan?

At 7% APR over 60 months, a $50,000 equipment loan runs approximately $990 per month. At 10% APR over the same term, that rises to roughly $1,061 per month. Use the equipment financing calculator above to run your exact rate and term combination.

How much is a $30,000 loan over 5 years?

A $30,000 equipment loan at 8% APR over 60 months produces a monthly payment of approximately $608. At 6% APR the payment drops to around $580, and at 15% APR it climbs to roughly $714. The financing equipment calculator handles any rate variation instantly.

How much should I put down on equipment financing?

Down payment requirements depend heavily on your credit profile. Excellent-credit borrowers often put 0–10% down, and some lenders offer 100% financing on new equipment. Standard applicants typically put 10–20% down. Startups and credit-challenged businesses should plan for 20–35% upfront regardless of lender type.

Does applying for equipment financing hurt my credit score?

Pre-qualification uses a soft credit pull, which has zero impact on your score. You can compare rates across multiple lenders at this stage without any penalty. A hard pull only occurs when you formally submit an application and authorize it, typically lowering your score by fewer than 5 points temporarily.

Still have questions about your specific situation? The equipment financing calculator at the top of this page is the fastest way to get a personalized payment estimate. Plug in your loan amount, the rate you expect to qualify for based on your credit profile, and your preferred term length, you’ll have a real monthly figure in seconds, without filling out an application or triggering a credit pull.

When you’re ready to move forward, compare at least two to three lenders using soft-pull pre-qualification before committing to any offer.

Founder of Nanotom Capital & Nanotom Labs