Key Takeaways

- Farm equipment costs are massive; new tractors run up to $400,000 and combines can exceed $1 million, making financing a necessity for the vast majority of the 1.88 million U.S. farms.

- USDA FSA Direct Loans offer the lowest rates available (4.75% as of December 2024), with no hard credit score cutoff, yet remain the most underused financing option in agriculture.

- Agricultural lenders like AgDirect build payment schedules around harvest income, offering 90-day deferrals, annual payment options, and skip-payment months that standard business loans never provide.

- Section 179 lets you deduct up to $2.5 million on financed equipment in year one; you don’t need to pay cash to capture the full deduction, making financing more tax-efficient than paying outright in many cases.

- Bad credit doesn’t disqualify you, some online lenders approve scores as low as 550, and FSA loans evaluate overall repayment ability rather than credit score alone.

- Auction and private-party purchases are fully financeable: AgDirect requires a $25,000 minimum and application at least two business days before the auction date, with the lender paying the seller directly on private sales.

- Leasing beats buying for tech-heavy equipment with short useful lives; buying builds equity for machinery you’ll run for 10–15 years; the right structure depends entirely on how long you’ll use the asset.

A new tractor can cost $150,000. A combine harvester can run past $500,000. Most farmers can’t write that check, and they shouldn’t have to.

Farm equipment financing lets you acquire the machinery you need now and pay for it over time, preserving working capital for seeds, labor, and operating costs. It comes in several forms: term loans, equipment leases, and lines of credit.

This guide covers every financing path available to U.S. farmers, from USDA programs to bad-credit options to auction purchases.

What Is Farm Equipment Financing?

Farm equipment financing is a funding mechanism that allows farmers and agricultural businesses to purchase or lease tractors, combines, planters, and other machinery without paying the full cost upfront. The equipment itself typically serves as collateral, which keeps rates lower than unsecured business loans. For a deeper foundation on how this works across industries, see our complete beginner’s guide to equipment financing.

The scale of this market makes financing essential, not optional. The U.S. has approximately 1.88 million farms according to USDA ERS data, and the U.S. agricultural equipment market was valued at $70.91 billion in 2024 per Market Data Forecast. Very few of those operations buy equipment outright.

Agriculture equipment financing typically covers:

- Tractors and combines

- Planters, sprayers, and tillage equipment

- Irrigation systems and grain bins

- Livestock equipment and feeding systems

- Used and auction-purchased machinery

Financing for farm equipment is structured around agriculture’s seasonal cash flow. That means payment schedules often look very different from standard business loans, and we’ll get into that in detail below.

Types of Farm Equipment You Can Finance

Most lenders will finance any machinery that’s integral to farm operations. Here’s what that looks like across equipment categories.

Tractors

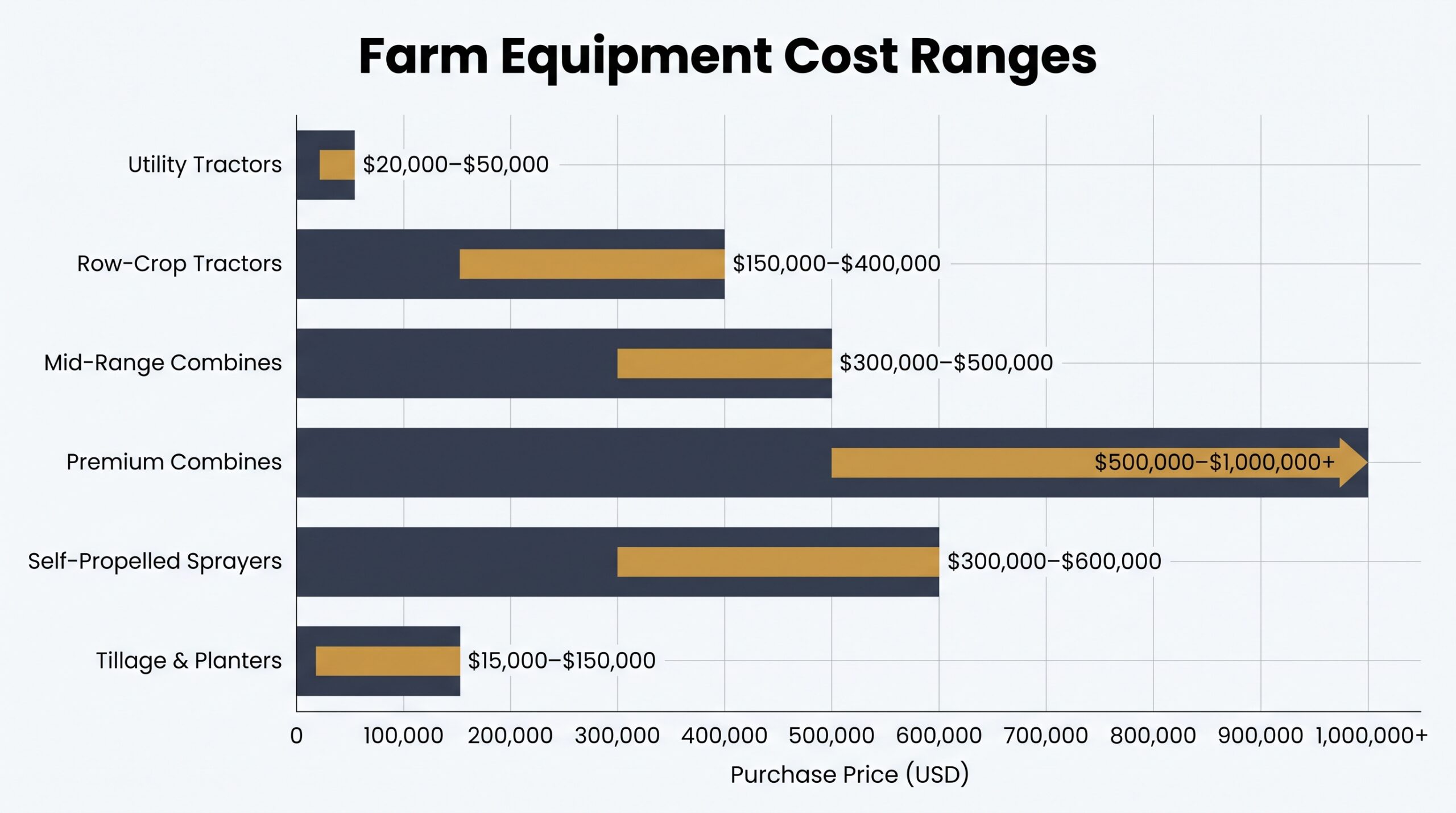

Small utility tractors start around $20,000–$50,000. Large row-crop tractors run $150,000–$400,000+. Farm equipment financing for tractors is the most common agricultural loan type, and most lenders treat them as straightforward collateral.

Combines and Harvesters

Mid-range combines run $300,000–$500,000. Premium models from John Deere or Case IH can exceed $1 million according to Hayden Outdoors. Agricultural equipment financing terms on combines typically stretch 5–7 years to keep payments manageable.

Irrigation Systems and Pivots

Center pivots and drip systems qualify for agriculture equipment financing, with lenders like AgDirect offering terms up to 10 years specifically for irrigation infrastructure.

Tillage and Planting Equipment

Planters, disc rippers, and strip-till machines range from $15,000 to $150,000+. These are commonly bundled into multi-equipment loans.

Sprayers and Applicators

Self-propelled sprayers run $300,000–$600,000. Pull-type models start around $20,000. Financing terms mirror tractor loans in structure.

Livestock and Specialty Equipment

Feeders, milking systems, poultry equipment, and greenhouse infrastructure all qualify. Specialty lenders often handle these better than traditional banks.

New vs. Used Farm Equipment

Used equipment typically carries higher interest rates and shorter terms. Here’s what most guides miss, though: Section 179 applies to used equipment too, as long as it’s new to your operation. Financing used farm equipment can deliver strong tax advantages at a lower purchase price.

Farm Equipment Financing Options

There’s no single best path. The right structure depends on your cash flow, tax situation, and how long you plan to keep the equipment.

Equipment Loans

You own the equipment from day one. The machinery serves as collateral, terms typically run 2–7 years, and most farm equipment financing loans carry fixed rates, giving you predictable payments across seasons.

Equipment Leasing

Lower monthly payments, easier qualification, and built-in upgrade flexibility. Leasing works especially well for tech-heavy equipment that depreciates fast. At lease end, you can buy, return, or upgrade. Compare leasing vs. financing before committing to either structure.

USDA Farm Service Agency (FSA) Loans

This is genuinely the most underused financing option in agriculture. The FSA offers three loan types worth knowing:

- Direct Farm Operating Loans: Up to $400,000 at 4.75% (as of December 2024)

- Guaranteed Farm Operating Loans: Up to $2.343 million for FY2025, issued through approved lenders

- Microloans: Up to $50,000, streamlined application, ideal for smaller operations and beginning farmers

FSA loans are designed for farmers who can’t qualify through conventional channels. Beginning farmers, veterans, and underserved producers get priority access.

Manufacturer and Dealer Programs

John Deere Financial offers promotional 0% APR for 36–72 months on select new equipment, though availability depends on model and timing. These programs are competitive but require strong credit and often push you toward newer, higher-priced inventory.

Refinancing Existing Farm Equipment

If you have paid-off or nearly paid-off equipment, refinancing lets you pull equity out for operating capital or upgrade purchases. It also lets you replace high-rate loans taken during tighter credit periods. Check current farm equipment financing rates before assuming your existing loan is still competitive.

Farm Equipment Financing Rates Explained

Your rate determines whether a purchase cash-flows or crushes you. Here’s what actually drives it, and what to expect by lender type.

What Drives Your Rate

Credit score, time in farming, loan-to-value ratio, equipment age, and loan term all factor in. Lenders also weigh your debt service coverage ratio, meaning how comfortably your farm income covers existing obligations plus the new payment.

Rate Ranges by Lender Type

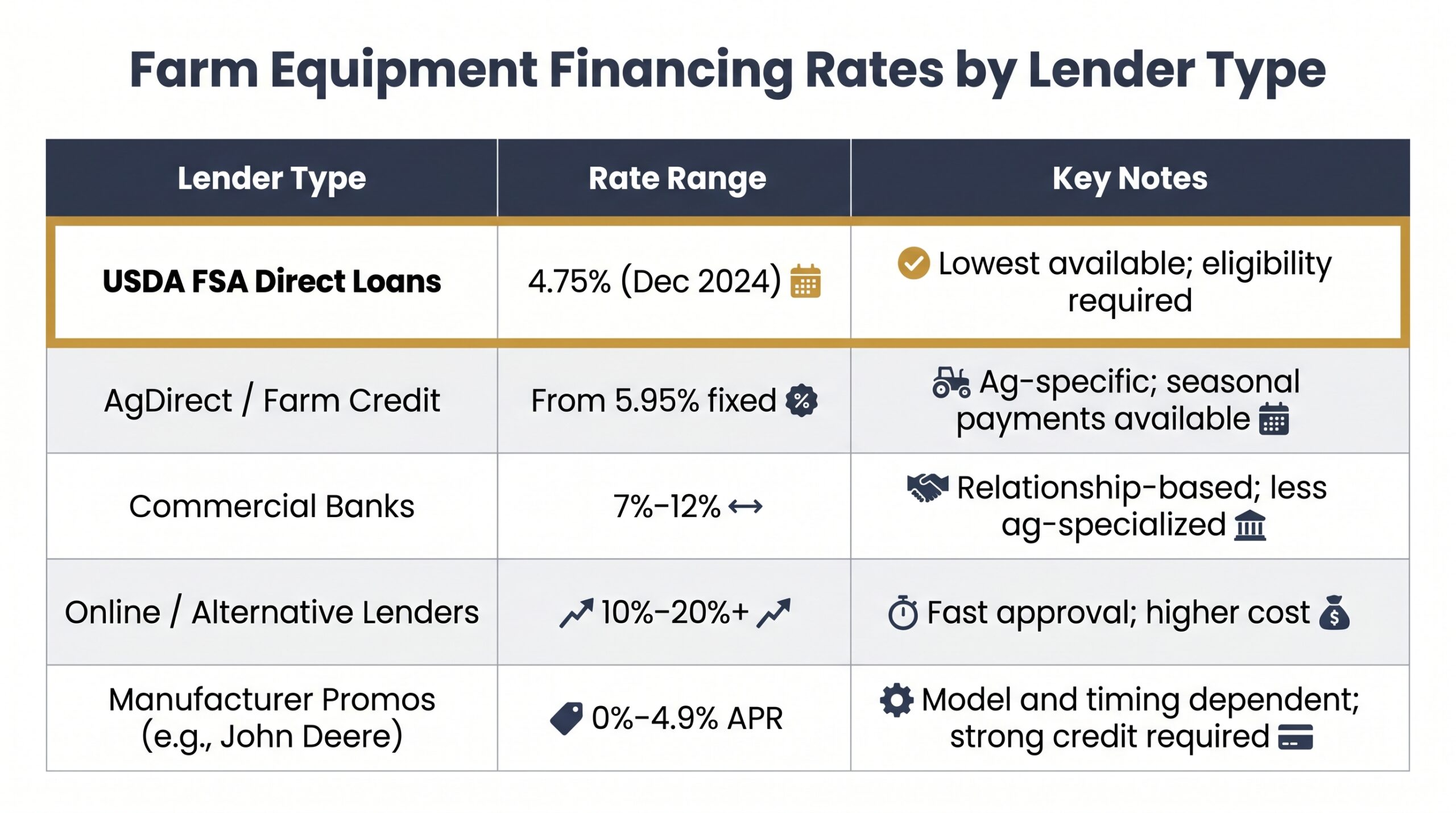

| Lender Type | Rate Range | Notes |

|---|---|---|

| USDA FSA Direct Loans | 4.75% (Dec 2024) | Lowest available; eligibility requirements apply |

| AgDirect / Farm Credit | Starting at 5.95% fixed | Agriculture-specific; competitive terms |

| Commercial Banks | 7%–12% | Varies by relationship and creditworthiness |

| Online/Alternative Lenders | 10%–20%+ | Faster approval, higher cost |

| Manufacturer Promos (e.g., John Deere) | 0%–4.9% APR | Model and timing dependent; strong credit required |

Fixed vs. Variable Rates

Fixed rates lock your payment for the loan term. For large equipment purchases over $100,000, that predictability is worth paying a slight premium. Variable rates start lower but can climb if the prime rate rises, which adds real risk to already thin margins.

Seasonal and Deferred Payment Options

This is where agricultural equipment financing differs sharply from standard business lending. Most ag-focused lenders offer payment structures built around harvest income, including:

- 90-day payment deferrals at loan origination

- Annual or semiannual payment schedules timed to crop sales

- Skip-payment options during low-income months

- Step-up structures that increase payments as the operation grows

Seasonal payment structures can mean the difference between a loan that works with your cash flow and one that fights it every single month.

How to Qualify for Farm Equipment Financing

Qualification requirements vary significantly by lender type. Here’s what each tier actually looks for.

Credit Score Requirements

Most standard farm equipment financing requires a 650+ credit score. You’ll unlock better rates at 670+, and the lowest advertised tiers typically require 720 or above. FSA and manufacturer programs have their own criteria that don’t always follow these benchmarks.

Down Payment Requirements

Down payments range from 0% to 20% depending on your credit profile and lender. AgDirect advertises 0% down options for qualified borrowers. Weaker credit usually means a larger down payment requirement to offset lender risk.

Revenue and Business History

Lenders review two to three years of farm income tax returns, your debt-to-income ratio, and cash flow consistency across seasons. A profitable operation with variable income still qualifies, but you’ll need documentation that shows the full picture of your farm’s financial health.

Financing with Bad Credit or Limited History

The honest answer is that bad credit doesn’t automatically disqualify you. Several paths remain open:

- USDA FSA loans: No hard credit score cutoff; lenders evaluate overall creditworthiness and repayment ability

- Online alternative lenders: Some approve scores as low as 550, with higher rates reflecting the risk

- Dealer captive programs: Manufacturer financing arms sometimes approve borrowers banks won’t touch, especially on high-value equipment

- Co-signers: A creditworthy co-signer can unlock standard financing rates even with a thin or damaged credit file

- Additional collateral: Land, existing equipment, or other assets can substitute for credit strength

Beginning farmers with no credit history face a different challenge than those with damaged credit. Equipment financing with no credit check options exist, though they come with tradeoffs worth understanding before you apply.

Where to Get Farm Equipment Financing

Your lender choice affects your rate, your payment structure, and which equipment qualifies. See our full comparison of the best farm equipment financing companies across all lender types. Here’s how each channel compares.

Agricultural Lenders (Farm Credit System, AgDirect)

These are purpose-built for farming operations. AgDirect offers rates starting at 5.95%, seasonal payment structures, and financing across tractors, combines, irrigation, and specialty equipment. The Farm Credit System operates as a borrower-owned cooperative, meaning profits return to members over time.

Equipment Dealers and Manufacturers

John Deere Financial, Case IH Financial, and AGCO Financial are the major players. Promotional 0% APR offers make these attractive for new equipment buyers with strong credit. The tradeoff is that you’re often steered toward higher-priced inventory to access the best terms.

Banks and Credit Unions

Relationship lenders can be competitive, especially if you’ve banked with them for years. They lack the agricultural specialization of Farm Credit lenders, though, and their payment structures rarely account for seasonal cash flow.

Online Lenders and Brokers

Faster approvals, more flexible credit requirements down to 550, and rates that typically run 10%–20%+. These lenders are best used when speed matters or conventional lenders have declined. Equipment financing brokers can shop multiple online lenders simultaneously, which saves significant time on rate comparisons.

Financing at Auctions and Private Party Purchases

Here’s what most financing guides skip entirely: both auction and private-party purchases are fully fundable through ag lenders.

For auction purchases, AgDirect requires you to apply at least two business days before the auction date, with a minimum purchase of $25,000. Approval is secured before you bid, so you’re not scrambling for funds after the hammer falls.

For private party purchases, the lender pays the seller directly. You’ll need a bill of sale, and the lender will run a lien search on the equipment before funding. It works like a standard loan, just with an individual seller instead of a dealership.

Tax Benefits of Financing Farm Equipment

Most farmers zero in on the rate. Fair enough, but the tax side of farm equipment financing can matter just as much, and sometimes more.

Section 179 Deduction

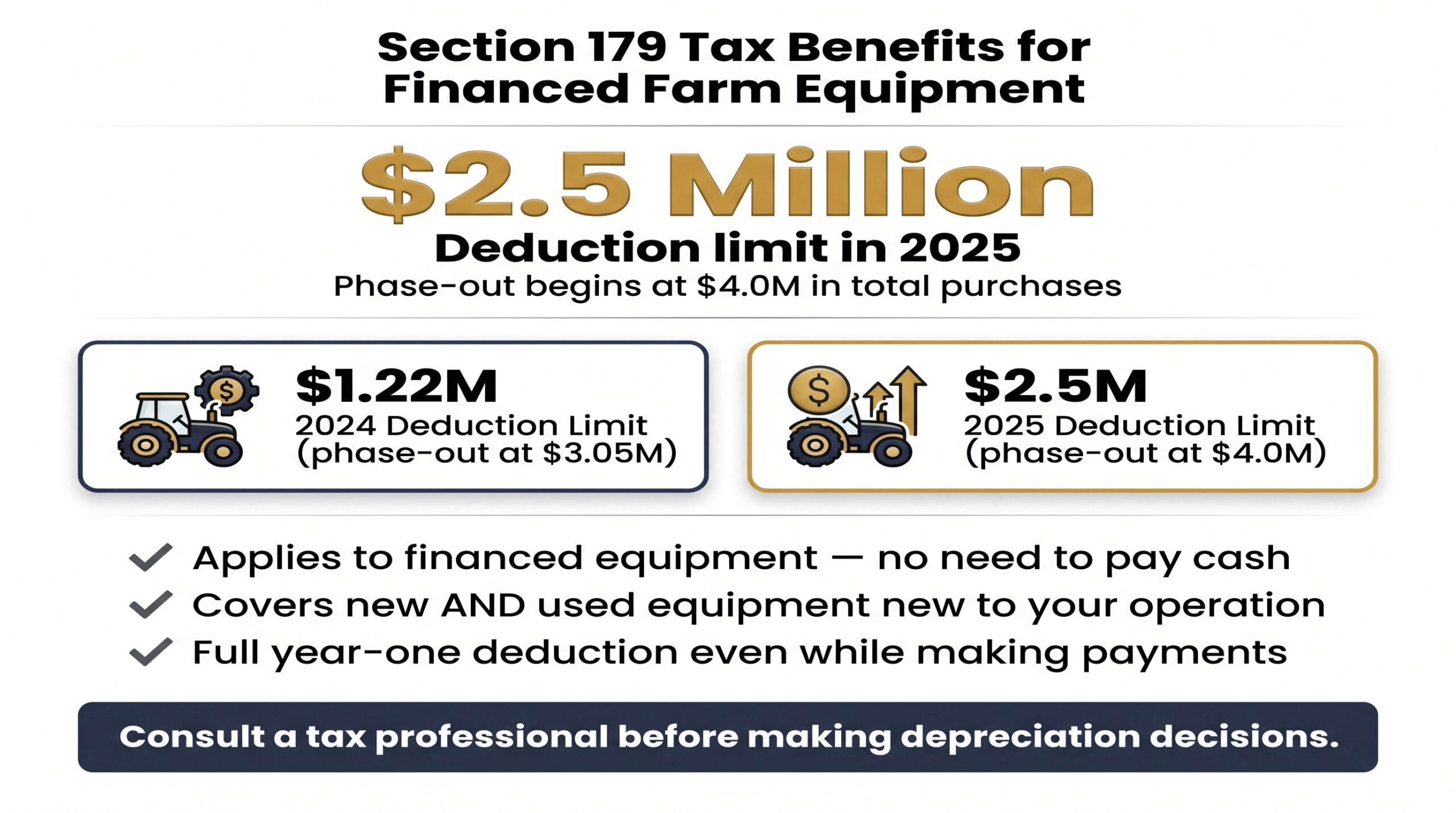

In 2025, farmers can deduct up to $2.5 million on qualifying equipment purchases per Section179.org, with the phase-out beginning at $4.0 million in total purchases. The 2024 limit was $1.22 million, with phase-out starting at $3.05 million.

Here’s the part that changes the financing calculation entirely: Section 179 applies to financed equipment. You can deduct the full purchase price in year one even if you’re still making monthly payments. You don’t need to pay cash to capture the full deduction.

A few rules that matter:

- Equipment must be placed in service during the tax year you claim the deduction

- Applies to both new and used equipment, as long as it’s new to your operation

- Cannot exceed your taxable business income for the year

- Works on tractors, combines, irrigation systems, and most qualifying farm machinery

This makes a strong argument for financing over paying cash. You preserve working capital, keep cash liquid for inputs and operations, and still capture the full year-one deduction.

Bonus Depreciation

Bonus depreciation allows an additional first-year deduction on top of Section 179. The rate was 60% in 2024 and continues phasing down under current law. Unlike Section 179, bonus depreciation can generate a net operating loss, which may carry forward to future tax years.

Tax strategy around agricultural equipment financing is genuinely complex. Always work with a tax professional who understands farm operations before making decisions based on depreciation schedules.

How to Apply for Farm Equipment Financing

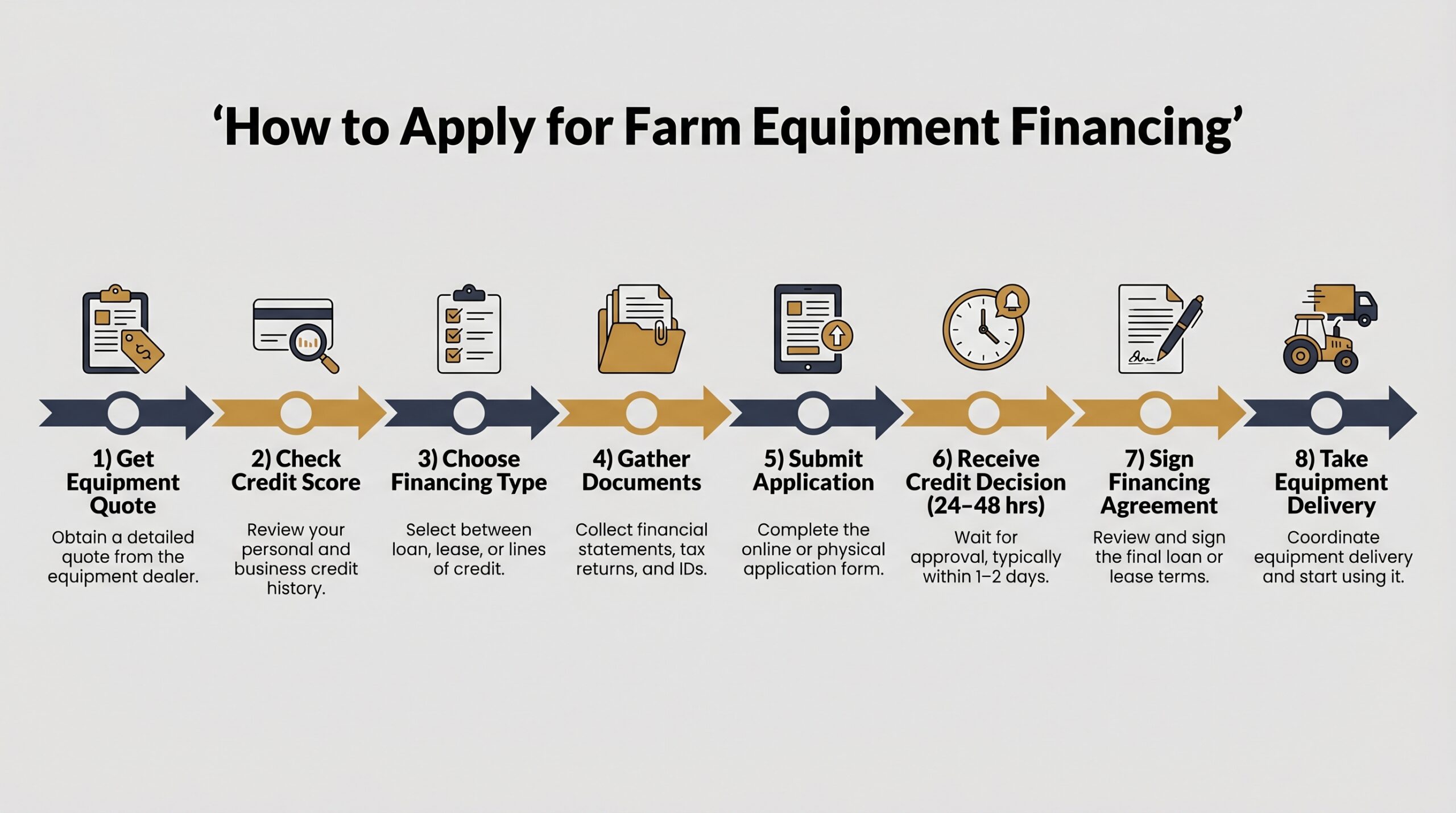

The process is straightforward when you know what to prepare. Here’s the full sequence from decision to delivery.

- Identify the equipment and get a price quote. For dealer purchases, request a formal quote. For auctions, get an estimate of expected sale price before you apply.

- Check your credit score. Aim for 650+ for standard farm equipment financing approval. Below that, explore USDA FSA loan options or alternative lenders before applying through conventional channels.

- Choose your financing structure. Decide between a loan, lease, USDA program, or manufacturer promotional offer based on your cash flow needs and tax situation.

- Gather your documents. Most lenders require government-issued ID, two to three years of farm tax returns or revenue records, and equipment details including make, model, serial number, and condition. Have a purchase agreement or auction invoice ready.

- Submit your application. Apply through an agricultural lender, equipment dealer, or online platform. For auction financing, submit at least two business days before the auction date.

- Receive your credit decision. Agricultural and online lenders typically respond within 24–48 hours. FSA direct loans take longer due to manual review processes.

- Review and sign the financing agreement. Read the equipment financing agreement carefully, paying attention to prepayment penalties, late fees, and payment schedule structure.

- Take delivery and begin payments. The lender funds the seller directly. Your payment schedule starts per the agreed terms, whether monthly, semiannual, or harvest-aligned.

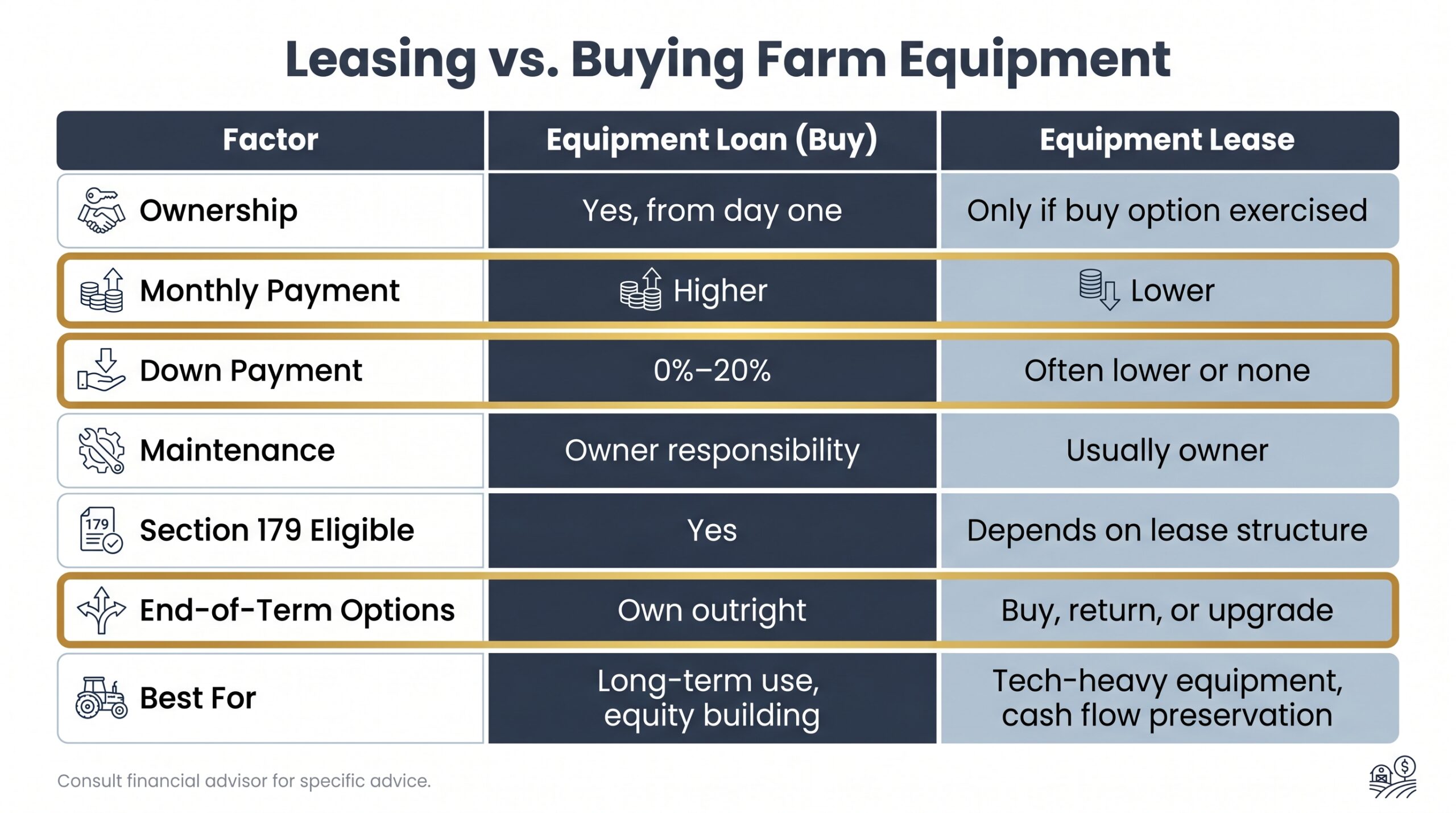

Leasing vs. Buying Farm Equipment: A Side-by-Side Comparison

Neither option is universally better. The right choice depends on what you’re buying, how long you’ll use it, and what your cash flow looks like at signing.

| Factor | Equipment Loan (Buy) | Equipment Lease |

|---|---|---|

| Ownership | Yes, from day one | Only if you exercise buy option at end of term |

| Monthly Payment | Higher | Lower |

| Down Payment | 0%–20% | Often lower or none |

| Maintenance Responsibility | Owner | Usually owner |

| Section 179 Eligible | Yes | Depends on lease structure |

| End-of-Term Options | Own outright | Buy, return, or upgrade |

| Best For | Long-term use, stable equipment, equity building | Tech-heavy equipment, cash flow preservation, frequent upgrades |

Buying makes sense when you plan to run the equipment for its full useful life and want to build equity. A tractor you’ll use for 15 years is a buy. A precision ag system that’ll be outdated in five years is a lease candidate.

Leasing preserves working capital and keeps you on newer equipment, but you’re not building any asset value unless you purchase at term end. For a deeper breakdown of how each structure affects your total cost of ownership, see our full equipment leasing vs. financing comparison.

Farm Equipment Financing Calculator

Before you apply, run the numbers. Knowing your estimated monthly payment before you walk into a lender conversation gives you a stronger negotiating position.

Use our farm equipment financing calculator to estimate your payment in under a minute. You’ll need four inputs:

- Equipment cost: Full purchase price or auction estimate

- Down payment: Enter 0% if you’re pursuing a no-down-payment option

- Interest rate: Use the rate ranges from the lender comparison table above

- Loan term: Typically 36–84 months for farm equipment financing

As a real example: a $150,000 tractor financed at 6.5% over 60 months with 10% down produces an estimated monthly payment of roughly $2,607. Extend that to 84 months and the payment drops to around $1,960, but total interest paid increases significantly.

Running multiple scenarios before you apply helps you match the loan term to your actual cash flow, not just the lowest possible payment. Seasonal payment structures can shift these numbers further, so confirm with your lender how a post-harvest schedule affects your total cost.

Frequently Asked Questions

Can I get a loan for farm equipment?

Yes. Farm equipment financing is available through agricultural lenders like Farm Credit and AgDirect, USDA FSA programs, equipment dealers, banks, and online lenders. New, used, auction, and private-party purchases all qualify through the right lender.

What credit score is needed to finance a tractor?

Most lenders prefer 650+. You’ll get better rates at 720+. USDA FSA loans have no hard credit score cutoff and evaluate overall creditworthiness instead, making them a strong option for borrowers below conventional thresholds.

What credit score is needed for equipment financing?

The common floor is 620–650. A score of 680+ improves both approval odds and your rate. The lowest advertised tiers typically require 720 or above.

How hard is it to get farm equipment financing?

For farmers with decent credit and documented income, it’s straightforward, especially through ag-specialized lenders. Bad credit makes it harder but not impossible. USDA FSA loans and online lenders approve applicants that conventional banks decline.

What is the minimum amount for farm equipment financing?

Most lenders start at $5,000. AgDirect requires a $25,000 minimum for auction and private-party purchases specifically.

Does Section 179 apply to financed farm equipment?

Yes. You can claim the full Section 179 deduction in year one even if the equipment is financed and you’re still making payments. You don’t need to pay cash to capture the deduction.

Whether you’re financing a $30,000 tractor through a dealer promo or funding a $400,000 combine through AgDirect, the right structure saves you real money. Compare your lender options, run your payment scenarios, and apply with confidence. See our top-rated farm equipment financing lenders to find the best fit for your operation.

Founder of Nanotom Capital & Nanotom Labs