Key Takeaways

- Outfitting a full commercial gym costs $50,000 to $500,000 upfront; financing spreads that burden across 24 to 84 months so you open without draining capital.

- Business owners with a 650+ credit score and established history qualify for rates as low as 6% to 12%; bad credit borrowers (575+) can still get approved through lenders like National Funding and Triton Capital using asset-backed leases.

- The 2025 Section 179 deduction limit is $2,500,000; financed equipment qualifies, meaning you can deduct the full purchase price in Year 1 without paying cash upfront.

- Individuals financing home gym equipment can use BNPL providers like Affirm or Klarna, which together hold roughly 86% usage share among BNPL users, with 0% APR promotions available on purchases under $5,000.

- Buying used commercial equipment costs 30% to 50% less than new, cutting your financed amount and monthly payment nearly in half. A $4,000 used treadmill versus an $8,000 new one at the same rate makes a direct impact on cash flow.

- A $50,000 equipment loan at 7% over 60 months runs approximately $990/month; larger facilities crossing $100,000 should consider SBA 7(a) loans for terms up to 10 years and rates at prime plus 2.75% to 4.75%.

- Online lenders can approve and fund gym equipment financing the same business day; SBA loans take two to four weeks but deliver the lowest long-term rates for established operators.

Buying gym equipment outright is expensive. A single commercial treadmill runs $3,000 to $10,000, and outfitting a full facility can cost $50,000 to $500,000 before you open your doors. Gym equipment financing solves that by spreading costs over time, keeping cash in your business while you build revenue.

This guide covers every financing path available, whether you’re a gym owner equipping a 10,000-square-foot facility or an individual building a home gym on a budget.

What Is Gym Equipment Financing?

Gym equipment financing is any funding arrangement that lets you acquire fitness equipment now and pay for it over time through structured installments, leases, or revolving credit. Instead of depleting capital in one transaction, you preserve liquidity while gaining immediate access to the equipment you need.

Options exist for both ends of the market. Commercial gym owners can access SBA loans, equipment-specific term loans, and sale-leaseback programs. Individuals financing home gym gear can use personal loans, retailer installment plans, or buy-now-pay-later programs. The right structure depends on your purchase size, credit profile, and cash flow needs.

The scale of these decisions matters. According to Statista, the U.S. fitness industry generated roughly $41.8 billion in revenue in 2024 across more than 114,000 facilities, making workout equipment financing one of the most common capital decisions gym operators face. For foundational context on how these programs work, see what equipment financing is before diving into the specifics.

Gym Equipment Financing Options for Business Owners

Here’s what most guides skip: commercial operators actually have more financing paths available to them than most people realize. Here’s how each option works in practice.

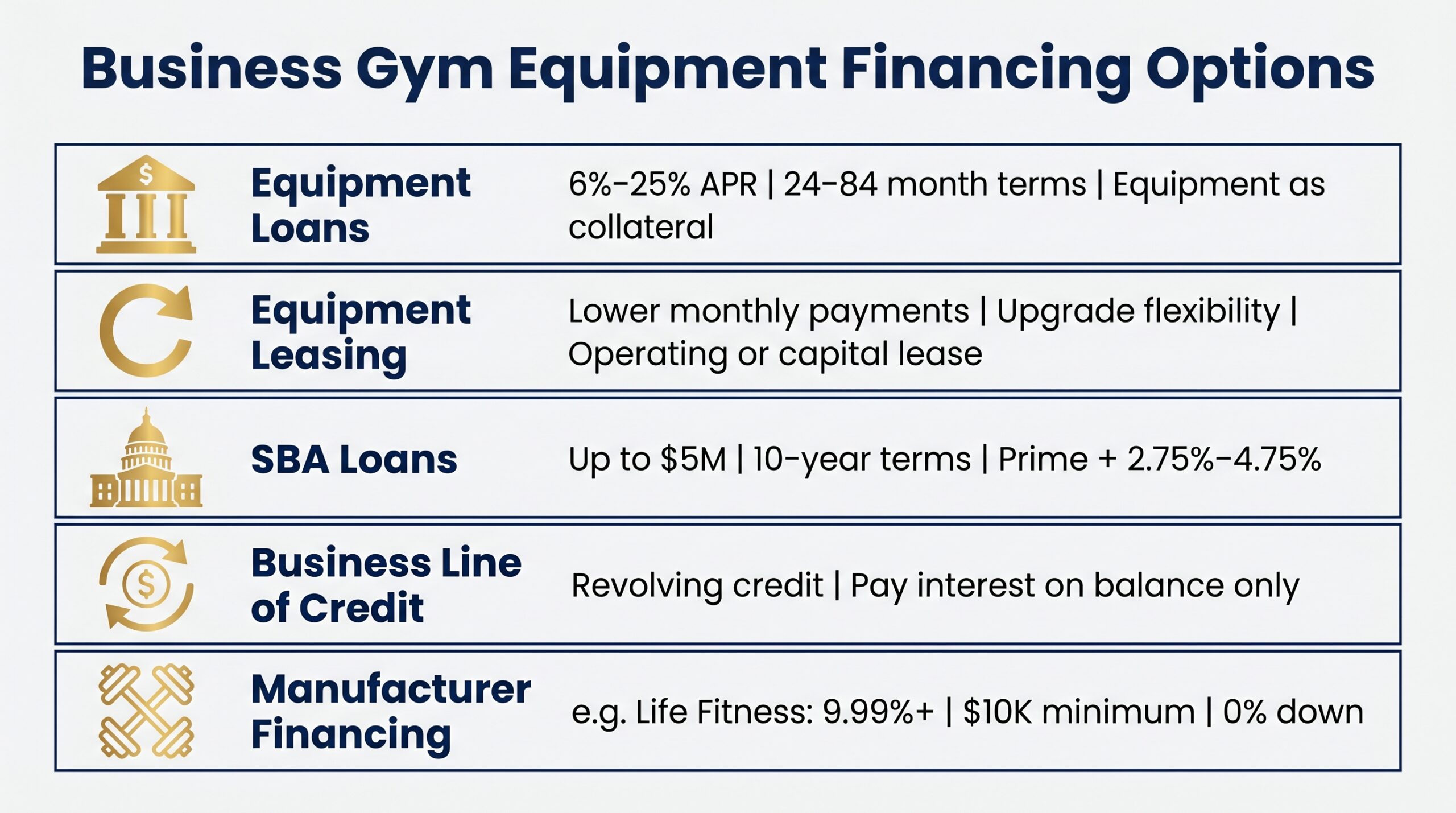

Equipment Loans

The equipment itself serves as collateral, which makes approval more accessible than unsecured lending. Terms run 24 to 84 months, with rates between 6% and 25% depending on your credit profile and time in business. See equipment financing explained for a full breakdown of the loan structure.

Equipment Leasing

Leasing keeps monthly payments lower and lets you upgrade cardio machines every few years without being stuck with depreciated assets. Operating leases keep equipment off your balance sheet; capital leases function more like ownership. Review equipment leasing vs. financing to determine which structure fits your tax situation.

SBA Loans

According to the SBA, 7(a) loans go up to $5 million with terms up to 10 years for equipment, at rates of prime plus 2.75% to 4.75%. The SBA 504 program also covers fixed asset purchases. To qualify, you’ll need to be a for-profit U.S. business that can’t obtain conventional credit on reasonable terms.

Business Lines of Credit

A revolving credit line works well for phased equipment purchases or ongoing replacements. You draw only what you need and pay interest on the balance, not the full limit.

Manufacturer Financing

Life Fitness offers in-house fitness equipment financing with rates starting at 9.99%, no money down, a $10,000 minimum, and a requirement that your business has been open at least two years. Rogue and similar brands typically route customers through third-party BNPL or lease partners.

Always compare manufacturer programs against independent lenders before signing. Manufacturer rates aren’t always the most competitive, and you won’t know that unless you shop around.

Gym Equipment Financing for Individuals

Most gym equipment financing guides stop at commercial options. That’s a mistake. Millions of people are financing home gym gear every year, and the options are genuinely good if you know where to look.

Personal Loans

Unsecured personal loans require no collateral, making them straightforward for home gym purchases ranging from $2,000 to $15,000. Terms run 12 to 84 months. Rates are higher than secured business loans (typically 8% to 36%), but approval is based primarily on your credit score and income. A 700+ credit score puts you in range for competitive rates.

Buy Now, Pay Later (BNPL)

Affirm and Klarna dominate the BNPL space, holding roughly 45% and 41% usage share among BNPL users respectively, according to LendingTree. Around 15% to 18% of BNPL users have financed fitness or sporting equipment this way. Promotional 0% APR periods make it a legitimate option for purchases under $5,000.

That said, treat BNPL like any other loan. Missed payments can damage your credit just as fast.

Credit Cards

Credit cards work well for smaller equipment purchases, especially with a 0% intro APR offer. Carrying a balance at a standard 20%+ APR turns a $1,500 weight set into a much more expensive purchase fast.

Retailer Financing Programs

Peloton, NordicTrack, and Bowflex all offer branded financing exercise equipment programs, most backed by Affirm, Klarna, or proprietary credit arms. These are convenient, but always compare the total repayment cost against a personal loan before committing. Retailer programs often carry deferred interest structures that can surprise you if the balance isn’t cleared before the promo period ends.

How to Qualify for Gym Equipment Financing

Qualification benchmarks vary significantly depending on whether you’re a business owner or an individual, and which financing type you’re pursuing. Here’s what lenders actually look for.

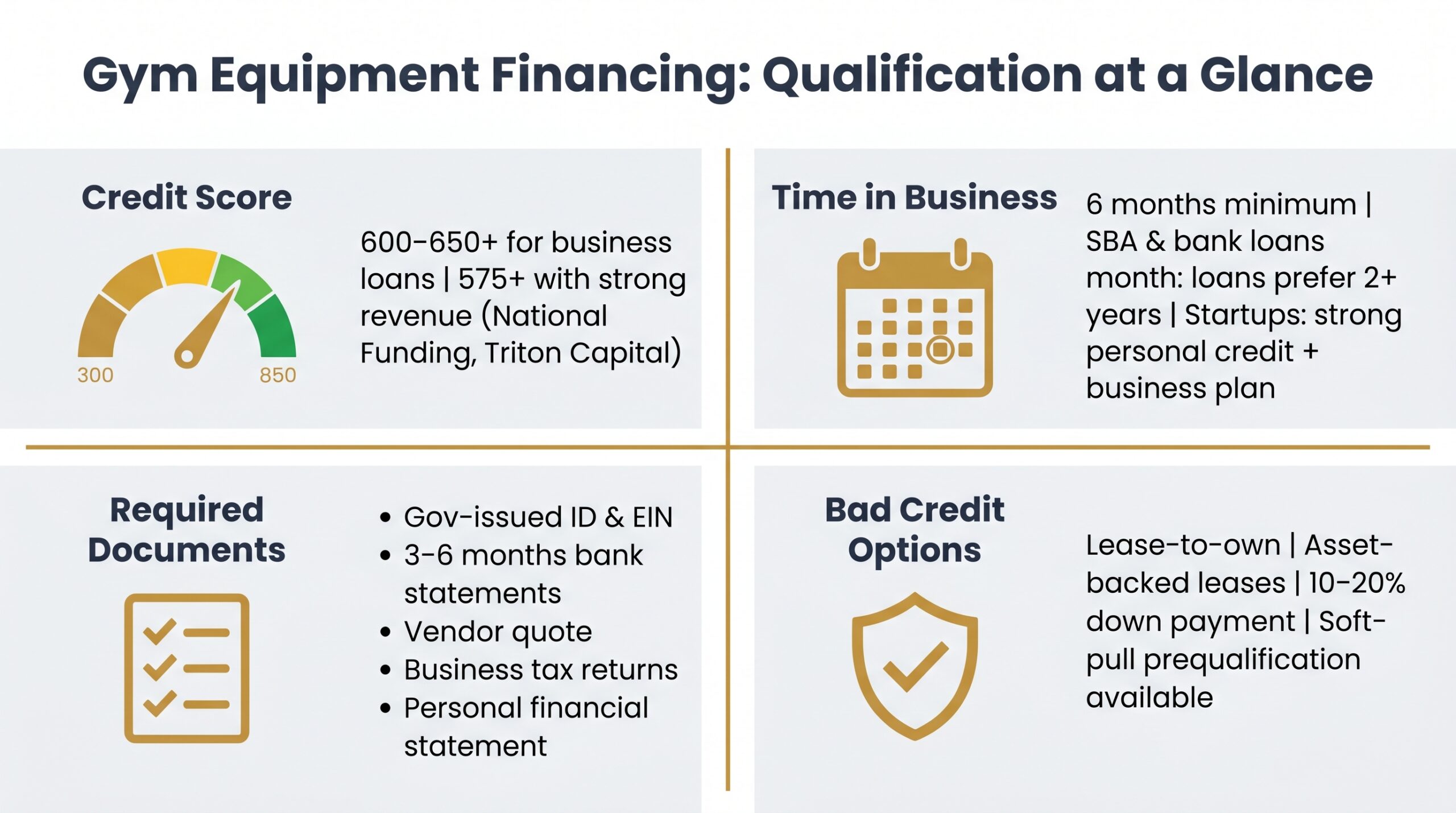

Credit Score Requirements

Most lenders require a 600 to 650 minimum FICO for business gym equipment financing. National Funding accepts scores as low as 575 with strong revenue and at least six months in business. Triton Capital works around 580. For personal loans and BNPL, requirements vary by provider, but 650 and above gets you the best rates.

Time in Business Requirements

Six months is the typical floor for business financing. SBA loans and bank programs generally prefer two or more years of operating history.

Startups aren’t automatically excluded, though. Strong personal credit and a detailed business plan can compensate for limited business history with the right lender.

Required Documentation

- Government-issued ID and EIN

- Three to six months of business bank statements

- Equipment vendor quote

- One to two years of business tax returns (larger loans)

- Personal financial statement

Bad Credit and Startup Gym Financing Options

Lease-to-own programs and asset-backed leases are the most accessible paths when credit is thin, since the equipment itself secures the deal. A 10% to 20% down payment can offset a weak credit profile significantly, and many vendors offer soft-pull prequalification that won’t hurt your score.

For more targeted guidance, see startup equipment financing and no credit check equipment financing options.

Gym Equipment Financing Rates and Terms

Rates vary widely based on credit profile, loan type, and lender. Here’s where you realistically land depending on your situation.

| Borrower Profile | Typical Rate Range | Typical Terms |

|---|---|---|

| Strong credit (650+), established business | 6% – 12% | 24 – 84 months |

| Weaker credit or startup | 12% – 25%+ | 12 – 60 months |

| SBA 7(a) loan | Prime + 2.75% – 4.75% | Up to 10 years |

| Manufacturer programs (e.g., Life Fitness) | 9.99%+ | Varies by program |

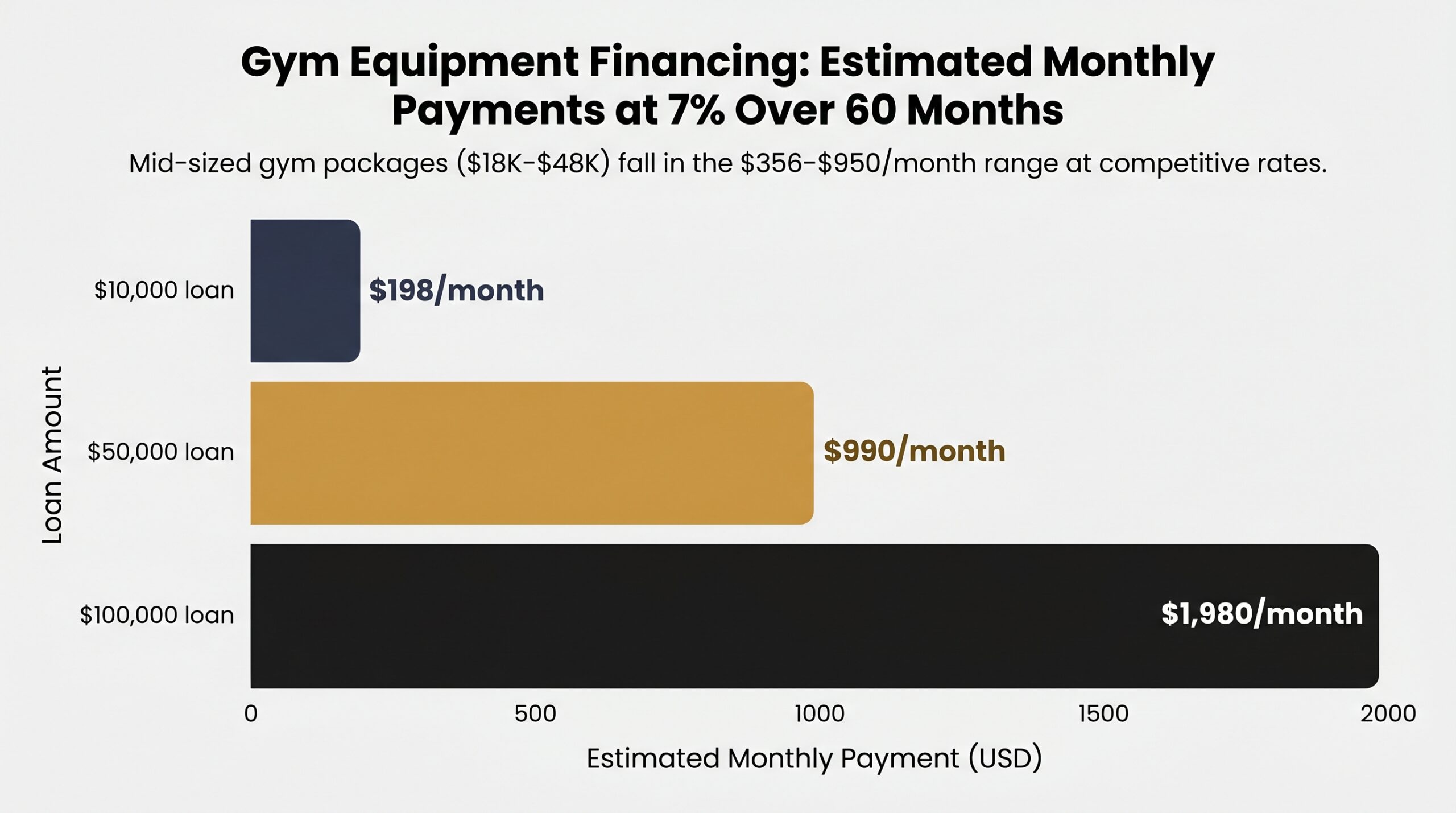

To put those rates in context, here’s what real-world fitness equipment financing payments look like at 7% over 60 months.

| Loan Amount | Rate | Term | Estimated Monthly Payment |

|---|---|---|---|

| $10,000 | 7% | 60 months | ~$198 |

| $50,000 | 7% | 60 months | ~$990 |

| $100,000 | 7% | 60 months | ~$1,980 |

Mid-sized commercial gym equipment packages typically run $18,000 to $48,000, putting most owners in the $356 to $950 monthly payment range at competitive rates. Larger facilities crossing $100,000 in equipment costs should strongly consider SBA financing for the longer terms and lower rates.

Use our equipment financing calculator to model your specific scenario, and review our equipment financing rates guide to understand what drives your rate up or down.

New vs. Used Gym Equipment Financing

Most lenders will finance both new and used equipment, but the terms aren’t identical. Used gym equipment financing typically carries slightly higher rates because lenders worry about residual value; a five-year-old commercial treadmill is harder to resell if you default than a brand-new one.

National Funding, for example, finances up to $150,000 on both new and used equipment with a vendor quote. The key requirement is that the equipment has verifiable value and a clear purchase source. Private-party purchases are harder to finance than used gear bought through a dealer or equipment reseller.

Leasing used equipment is less common. Lessors prefer assets with predictable resale value, which is why you’ll see operating lease programs almost exclusively on new commercial equipment from recognized brands.

The financial case for used is straightforward. A used commercial treadmill can cost 30% to 50% less than a new equivalent, directly reducing your financed amount and monthly payment. Financing a $4,000 used unit versus an $8,000 new one at the same rate cuts your monthly obligation nearly in half, that’s real cash flow you keep.

For a full breakdown of lender requirements and where to source pre-owned equipment, see our guide to used equipment financing.

Lease vs. Loan: Which Is Right for Your Gym?

Both are legitimate gym equipment financing paths. The honest answer is that there’s no universal winner; it comes down to how long you plan to keep the equipment and how much your monthly cash flow can absorb.

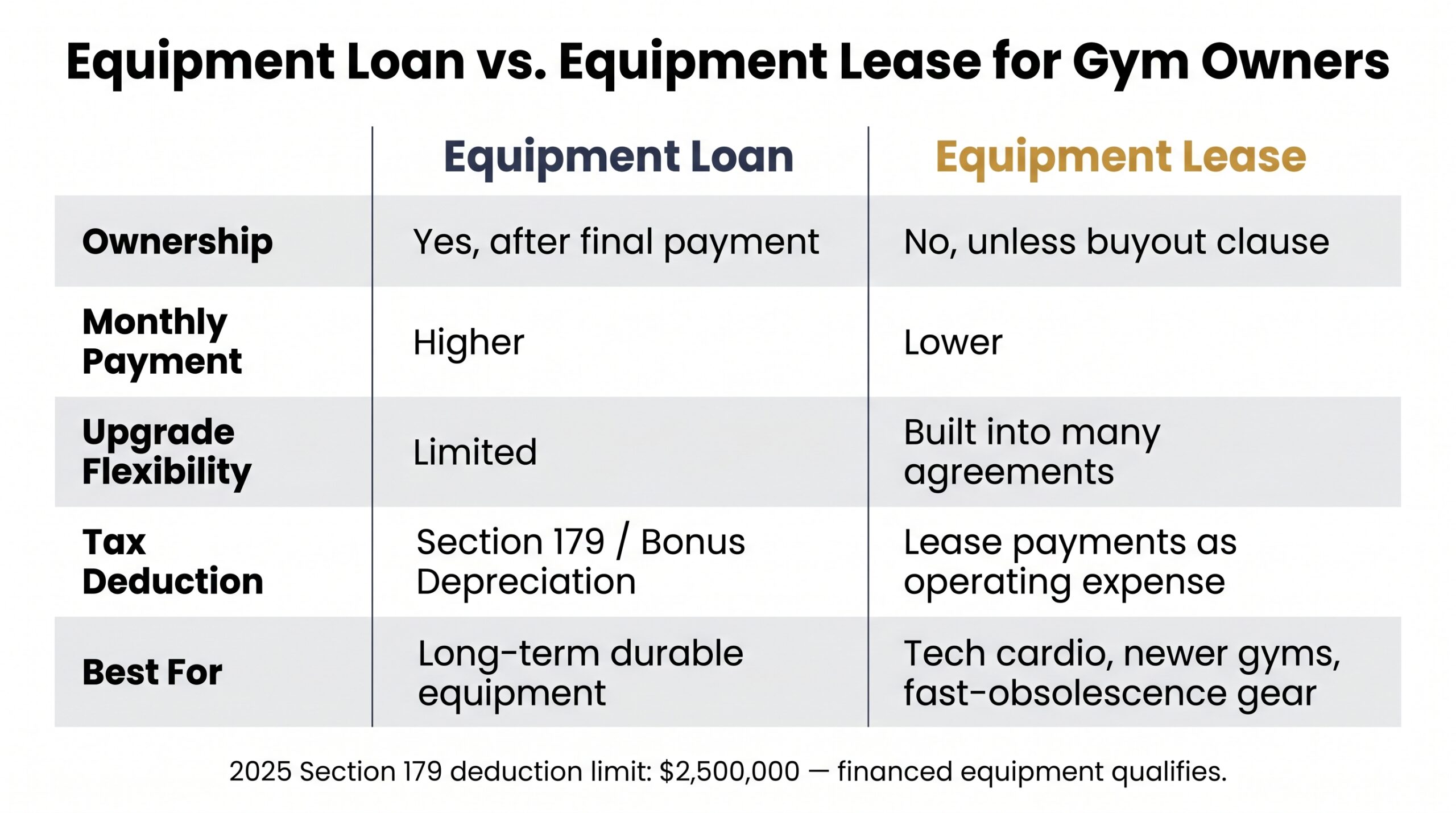

| Factor | Equipment Loan | Equipment Lease |

|---|---|---|

| Ownership | Yes, after final payment | No, unless buyout clause |

| Monthly Payment | Higher | Lower |

| Upgrade Flexibility | Limited | Built into many agreements |

| Tax Deduction Eligibility | Yes (Section 179 / bonus depreciation) | Yes (lease payments as operating expense) |

| Best For | Long-term ownership of durable equipment | Tech-integrated cardio, newer gyms, fast-obsolescence gear |

The Section 179 deduction is a major factor in this decision. According to IRS Publication 946, the Section 179 limit for 2025 is $2,500,000, meaning gym owners can potentially deduct the full purchase price of qualifying equipment in Year 1 rather than depreciating it over several years. Financed equipment qualifies; you don’t need to pay cash to claim the deduction. Certain lease structures may also qualify.

On a large equipment package, that deduction can save tens of thousands of dollars. Talk to a tax advisor before structuring your purchase so you don’t leave that on the table.

For a deeper side-by-side analysis, see equipment leasing vs. financing.

How to Apply for Gym Equipment Financing

The application process is straightforward once you know what to prepare. Online lenders can approve gym equipment financing the same day; SBA loans can take weeks. Here’s the full sequence.

- Determine your equipment needs and total budget. Price out specific units from vendors before approaching any lender. A vendor quote is required documentation for most financing applications anyway.

- Choose your financing type. Match the option to your situation. loan or SBA for established gyms buying long-term assets, lease for newer facilities or tech-heavy cardio, BNPL or personal loan for individual buyers.

- Gather your documentation. Government-issued ID, EIN, three to six months of bank statements, vendor quote, and one to two years of business tax returns for larger loan amounts.

- Compare lenders. Don’t stop at the first offer. Check rates, terms, origination fees, and prepayment penalties across at least three lenders before committing. If comparing multiple lenders feels overwhelming, an equipment financing broker can shop your application across dozens of lenders simultaneously, worth considering for larger financing gym equipment deals above $50,000.

- Submit your application. Online lenders often return decisions within hours. Bank and SBA programs move slower but typically offer better rates.

- Review the agreement carefully before signing. Watch for hidden fees, personal guarantee language, and buyout clauses in leases. Our equipment financing agreement guide walks through every clause worth scrutinizing.

- Equipment is funded and delivered. Repayment begins per your agreed schedule, typically within 30 days of funding.

Top Gym Equipment Financing Companies

Not all lenders treat gym equipment financing the same way. Some specialize in it; others treat it like any other equipment loan. Here’s how the major options stack up.

| Lender Type | Notable Provider | Min. Credit Score | Best For |

|---|---|---|---|

| Specialized Lender | Nanotom Capital | Flexible | Gym owners needing fast approvals and flexible fitness equipment financing terms |

| Online Equipment Lender | National Funding | 575+ | Established gyms, up to $150K, new or used equipment |

| Bad Credit Friendly | Triton Capital | ~580 | Startups and gym owners rebuilding credit |

| Manufacturer Program | Life Fitness Financial | Varies | Established facilities buying Life Fitness branded equipment |

| SBA-Approved Lenders | Various banks and CDFIs | 650+ | Larger purchases, lowest long-term rates, 2+ years in business |

Nanotom Capital is our top recommendation for gym owners. Fast approvals, flexible qualification criteria, and real experience with exercise equipment financing across both new and established facilities make it a strong first call before shopping elsewhere.

For a full breakdown of lender fees, terms, and approval requirements, see our best equipment financing companies guide.

Frequently Asked Questions About Gym Equipment Financing

Can I finance gym equipment with bad credit?

Yes. Lenders like National Funding and Triton Capital work with scores as low as 575 to 580. Asset-backed leases and lease-to-own programs are your most accessible options when credit is thin, since the equipment itself serves as collateral.

What credit score do I need for gym equipment financing?

Most lenders require 600 to 650 minimum for business financing. Strong revenue and six or more months in business can help you qualify on the lower end of that range.

Is gym equipment financing tax-deductible?

Yes. The Section 179 deduction allows business owners to deduct up to $2,500,000 in qualifying equipment costs in 2025. Both purchased and financed equipment can qualify, meaning you don’t need to pay cash to claim the deduction. Consult a tax advisor to confirm your specific situation.

Can I finance used gym equipment?

Yes. Most equipment lenders finance used gear as long as you provide a vendor quote and the equipment has verifiable value. Expect slightly higher rates than new equipment financing in some cases.

How long does it take to get approved for gym equipment financing?

Online lenders can approve and fund as fast as the same business day. SBA loans typically take two to four weeks or longer due to documentation requirements.

What is the minimum amount I can finance for gym equipment?

It varies by lender. Some online lenders start at $5,000. Life Fitness manufacturer financing requires a $10,000 minimum. Most bank and SBA programs are designed for larger amounts.

Can a startup gym get equipment financing?

Yes. Startups with strong personal credit of 600 or above and a solid business plan can qualify through several lenders. Lease-to-own and vendor financing programs tend to be the most startup-friendly paths.

Does financing gym equipment require a down payment?

Not always. Some programs offer 0% down for qualified borrowers. If your credit is weaker, a 10% to 20% down payment can significantly improve your approval odds and lower your rate.

Ready to move forward? Whether you’re outfitting a commercial facility or upgrading your home gym, the right financing gym equipment strategy depends on your credit profile, business stage, and how long you plan to keep the equipment. Nanotom Capital works with gym owners at every stage to find fast, flexible fitness equipment financing that fits the business, not just the numbers. Get your quote today and have your equipment funded in as little as 24 hours.

Founder of Nanotom Capital & Nanotom Labs