Key Takeaways

- Outfitting a laundromat from scratch costs $200,000–$500,000, making equipment financing the default path for most of the 29,500 laundromat locations operating across the U.S.

- Six financing structures exist; equipment loans, leases, SBA 7(a), SBA 504, manufacturer programs, and lines of credit, each with meaningfully different rates, terms, and ownership implications.

- On a $120,000 equipment purchase, total repayment ranges from ~$137,040 (manufacturer program at 6.75% over 48 months) to ~$151,536 (SBA 7(a) at 7% over 84 months), the lowest monthly payment is not the lowest total cost.

- Section 179 lets you deduct up to $1.25 million in qualifying equipment for 2025, and the deduction applies to financed equipment, you don’t need to buy outright to capture the tax benefit.

- Card-based payment systems produce auditable transaction records that reduce lender friction and can improve your financing terms compared to coin-only operations.

- Soft costs; installation, delivery, and plumbing hookups, can often be bundled directly into your financing agreement, reducing out-of-pocket expenses at closing.

- Alternative lenders approve and fund in 1–5 business days with credit scores as low as 550; SBA loans require 650+ and take 2–8 weeks but offer rates as low as 6%–7% APR.

Outfitting a laundromat from scratch costs anywhere from $200,000 to $500,000. That’s a serious capital commitment before you collect a single quarter. Laundromat equipment financing gives owners a way to acquire washers, dryers, and supporting infrastructure while keeping cash free for operations, marketing, and the repairs that always seem to come at the worst time.

This guide covers every financing path available, with real numbers and no manufacturer bias.

What Is Laundromat Equipment Financing?

Laundromat equipment financing is a commercial loan or lease used to acquire washers, dryers, vending units, payment systems, and related infrastructure, without paying the full cost upfront. Repayment typically spans 3 to 10 years at fixed or variable rates, depending on the lender and your credit profile.

Common structures include traditional equipment loans, operating leases, SBA 7(a) or 504 loans, and manufacturer-sponsored programs. Each carries different ownership, tax, and cash flow implications, all covered in detail below.

The U.S. laundromat industry generates roughly $6.8 billion in annual revenue across approximately 29,500 locations nationwide. Most operators simply can’t fund that equipment bill out of pocket. That’s exactly why understanding equipment financing options is the first real step toward opening or upgrading a laundromat, financing isn’t the fallback plan here, it’s the standard one.

How Much Does Laundromat Equipment Cost?

Before you can evaluate your financing options, you need a realistic number to work with. Costs vary significantly by machine type, capacity, and whether you’re buying new or used.

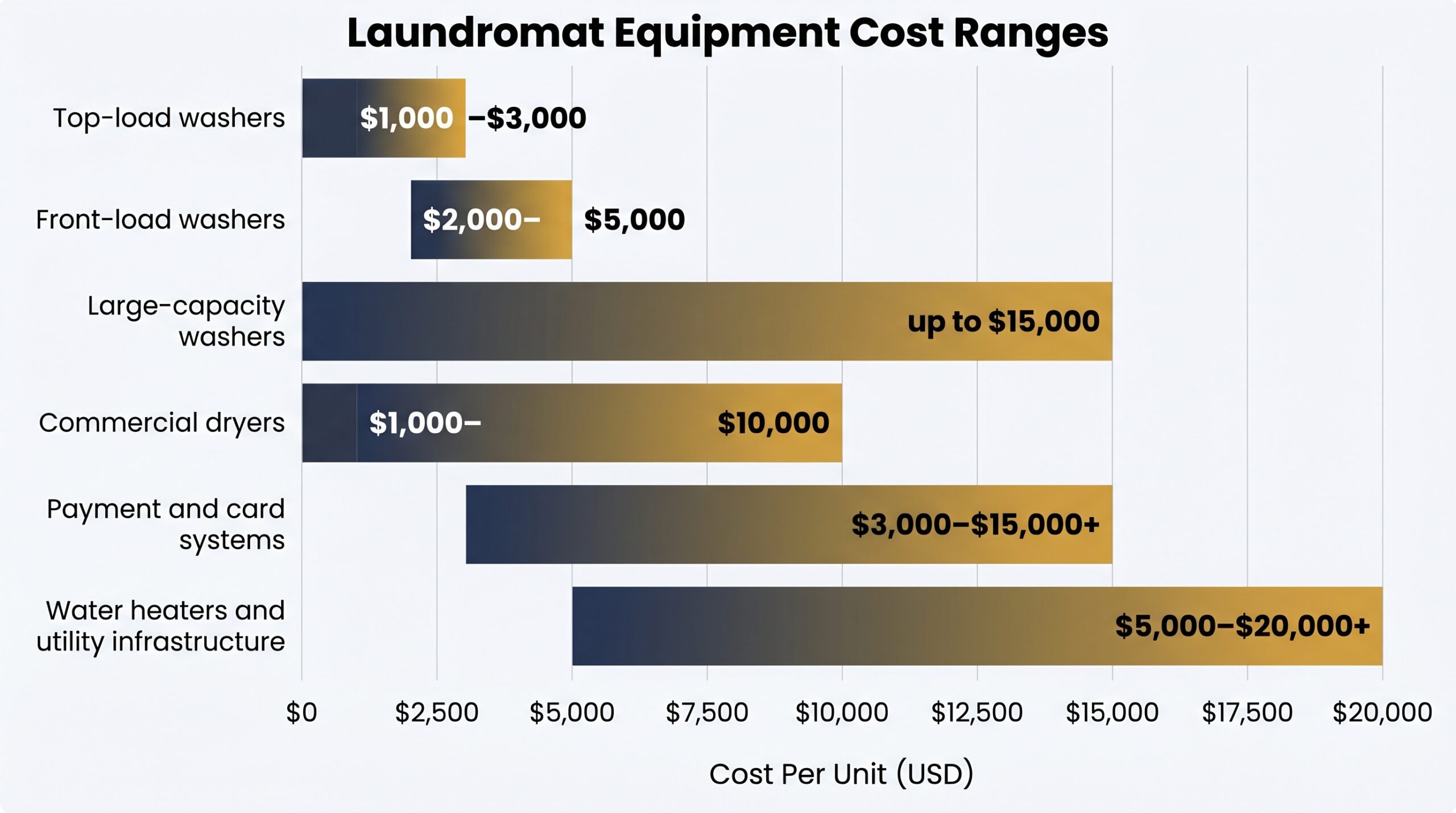

| Equipment Type | Cost Range (Per Unit) |

|---|---|

| Top-load washers | $1,000 – $3,000 |

| Front-load washers | $2,000 – $5,000 |

| Large-capacity washers | Up to $15,000 |

| Commercial dryers | $1,000 – $10,000 |

| Payment/card systems | $3,000 – $15,000+ |

| Water heaters and utility infrastructure | $5,000 – $20,000+ |

A small 15–20 machine location runs $40,000–$100,000 in equipment alone. A mid-size build pushes $100,000–$500,000+ once you factor in everything. Total startup costs for a new location typically land between $200,000 and $500,000.

Here’s what most financing guides skip: soft costs like delivery, installation, plumbing hookups, and venting can often be bundled directly into your financing agreement. That means less cash out of pocket at closing, not just on the machines themselves, but on the full project.

Card-based payment systems cost more upfront but signal stable, trackable revenue to lenders, which can meaningfully improve your financing terms. Use our equipment financing calculator to estimate monthly payments once you have a total project figure.

What Equipment Qualifies for Financing?

Most lenders cast a wide net. Qualifying assets for laundromat equipment financing typically include:

- Commercial front-load and top-load washers

- Stack dryers and high-capacity dryers

- Water heating systems

- Payment kiosks and card readers

- POS and management software systems

- Vending machines

- Folding tables, carts, and shelving

- Signage and security systems

New vs. Used and Refurbished Equipment

Used equipment is fully financeable. Lenders like Trust Capital and Western Equipment Finance routinely approve used equipment financing for laundromat operators, and pre-owned machines still qualify for Section 179 tax deductions.

Most lenders cap equipment age at 10–15 years and require proof of working condition. But buying refurbished can cut your upfront costs dramatically, so don’t dismiss it just because it’s not new.

Coin-Op vs. Card-Based Systems: What Lenders Actually Think

This distinction matters more than most owners realize. Coin-operated laundromats generate cash revenue that’s difficult to verify, which creates real friction during underwriting. Card-based systems produce digital transaction records lenders can actually audit, making income verification straightforward.

Hybrid operators running both systems typically present the strongest financing profile. You’re showing diversified revenue with at least partial documentation, which reduces perceived lender risk, and lower perceived risk usually translates to better terms.

Types of Laundromat Equipment Financing

There’s no single best structure. The right financing type depends on your credit profile, time in business, and whether you’re prioritizing ownership, cash flow, or flexibility.

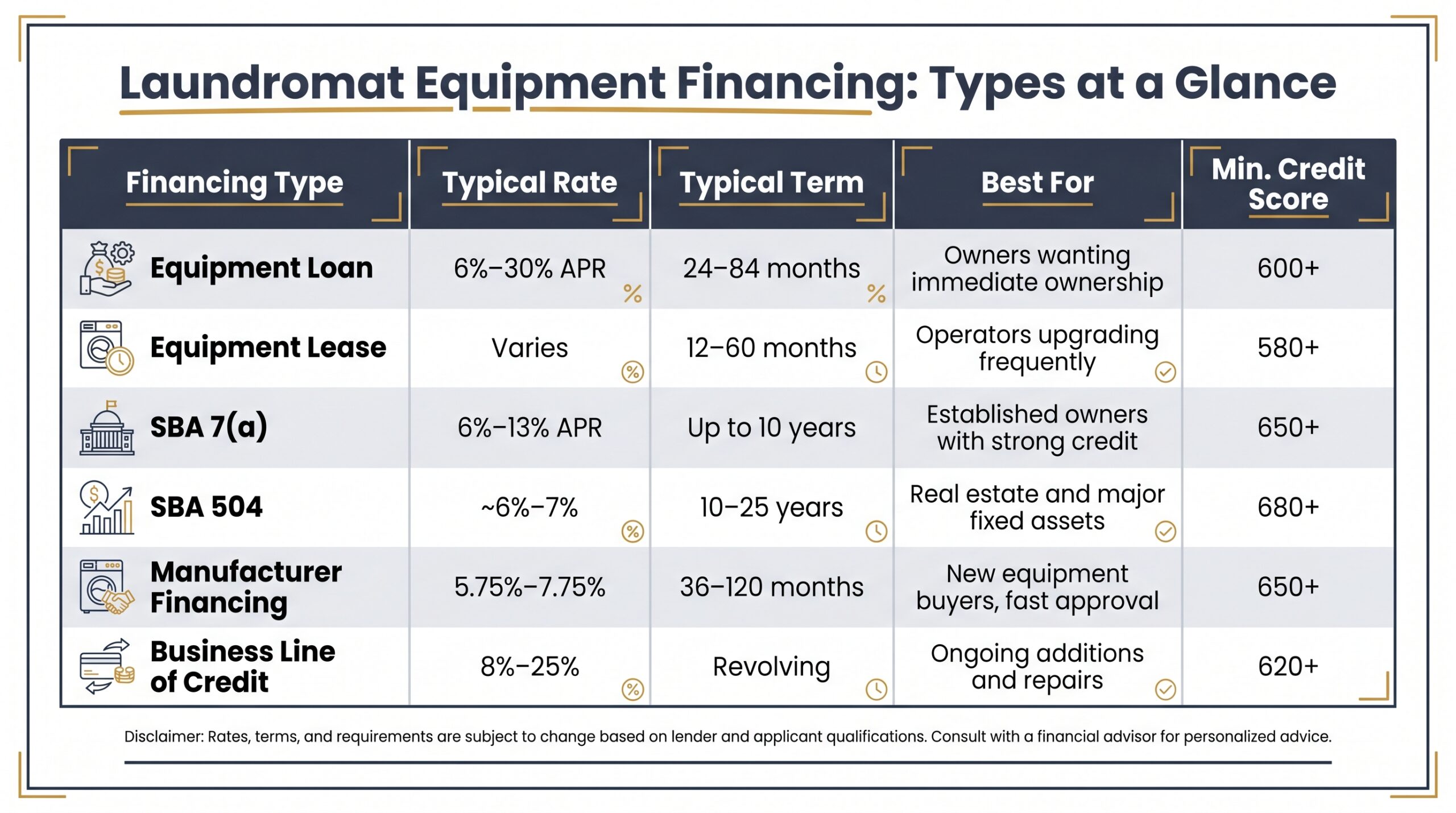

| Financing Type | Typical Rate | Typical Term | Best For | Min. Credit Score |

|---|---|---|---|---|

| Equipment Loan | 6%–30% APR | 24–84 months | Owners who want immediate ownership | 600+ |

| Equipment Lease | Varies | 12–60 months | Operators upgrading frequently | 580+ |

| SBA 7(a) | 6%–13% APR | Up to 10 years | Established owners with strong credit | 650+ |

| SBA 504 | ~6%–7% | 10–25 years | Real estate + major fixed assets | 680+ |

| Manufacturer Financing | 5.75%–7.75% | 36–120 months | New equipment buyers, fast approval | 650+ |

| Business Line of Credit | 8%–25% | Revolving | Ongoing additions and repairs | 620+ |

Equipment Loans

You own the equipment from day one. The machine itself serves as collateral, which keeps rates competitive. Terms run 24–84 months, and this structure pairs well with Section 179 deductions since you hold title immediately.

Equipment Leasing

Lower upfront cost, more flexibility. Operating leases keep debt off your balance sheet; finance leases function more like loans with a buyout at the end. The difference matters, equipment leasing vs. financing breaks it down fully before you sign anything.

SBA 7(a) Loans

The most flexible SBA option for standalone equipment purchases. Rates run 6%–13% APR, loans go up to $5 million, and terms stretch to 10 years. You’ll need 2+ years in business and a 650+ credit score for most lenders. Approval is slower, but for qualified borrowers, the terms are genuinely hard to beat. According to the SBA, the 7(a) program is the agency’s primary vehicle for equipment, working capital, and business acquisition financing.

SBA 504 Loans

A lot of competing guides conflate 504 with 7(a), they’re not the same. SBA 504 is designed for real estate and large fixed-asset projects, not standalone equipment purchases. If you’re buying a building and equipping it at the same time, 504 makes sense. For equipment only, 7(a) is your lane.

Manufacturer Financing Programs

Huebsch, UniMac, and Dexter, all under Alliance Laundry Systems, offer proprietary financing with promotional rates starting at 5.75% for 36 months, 6.75% for 48 months, and 7.75% for 60 months. Pre-qualification up to $200,000 is often instant. The tradeoff is that you’re locked into their equipment catalog, so make sure that works for your build before committing.

Business Lines of Credit

Revolving credit works well for incremental equipment additions, emergency repairs, or bridging gaps between financing rounds. Rates are higher than term loans, but the flexibility is real. Check current equipment financing rates to benchmark whatever you’re quoted.

Startup Laundromats vs. Existing Businesses: Key Financing Differences

Your business stage shapes your financing options more than almost any other factor. A first-time laundromat owner and an operator with three years of tax returns are effectively different borrowers in a lender’s eyes.

New and Startup Operators

Expect tighter terms. Most lenders require 20%–30% down, a credit score of 680 or higher, a detailed business plan, financial projections, and a personal guarantee. SBA loans are possible but harder to secure without operating history.

Manufacturer programs from Huebsch or Dexter and alternative lenders are typically the most accessible starting points. Explore your full range of startup equipment financing options before assuming you’re limited to one path.

Established Operators (2+ Years)

Business tax returns and bank statements unlock meaningfully better terms. Cash-flow underwriting gives lenders real data to work with, which means lower rates, longer terms, and less reliance on personal credit. SBA 7(a) becomes genuinely accessible here, and the difference in total cost over a 60- or 84-month term is substantial.

Expansion and Retool Financing

Upgrading an existing location is the easiest financing scenario of the three. Documented revenue, known equipment performance, and an established banking relationship all work in your favor. Lenders view retooling as lower risk than a ground-up build, and the terms tend to reflect that clearly.

How to Qualify for Laundromat Equipment Financing

Qualification requirements vary significantly by lender type. Here’s what each tier actually expects:

| Lender Type | Min. Credit Score | Down Payment | Min. Time in Business | Notes |

|---|---|---|---|---|

| Traditional Banks / SBA | 680–700+ | 10%–20% | 2+ years | Best rates, slowest approval |

| Alternative / Online Lenders | 550–600+ | 0%–10% | 6–12 months | Faster funding, higher rates |

| Leasing Companies | 600+ | 0%–10% | 1+ year | Off-balance-sheet flexibility |

| Manufacturer Programs | 650+ | 0%–20% | Startup-friendly | Locked to brand catalog |

| Startup Programs | 600+ (700+ co-signer) | 20%–30% | None required | Personal guarantee required |

Documentation You’ll Need

Most laundromat equipment financing applications require a completed application, 3–12 months of bank statements, 1–2 years of business and personal tax returns, an equipment invoice or purchase agreement, and business formation documents. A personal guarantee is standard across nearly every lender type, don’t be surprised when it comes up.

Coin-operated laundromats face one extra hurdle. Lenders may request additional documentation to verify cash income, utility bills correlated to usage or third-party revenue reports are common asks. Card-based operators simply pull transaction records. It’s a real difference in friction at the application stage, and it’s worth thinking about before you choose your payment infrastructure.

Real-World Loan Scenario: What Financing Actually Costs

Most laundromat equipment financing guides stop at rates and terms. Here’s what those numbers actually mean for a real purchase.

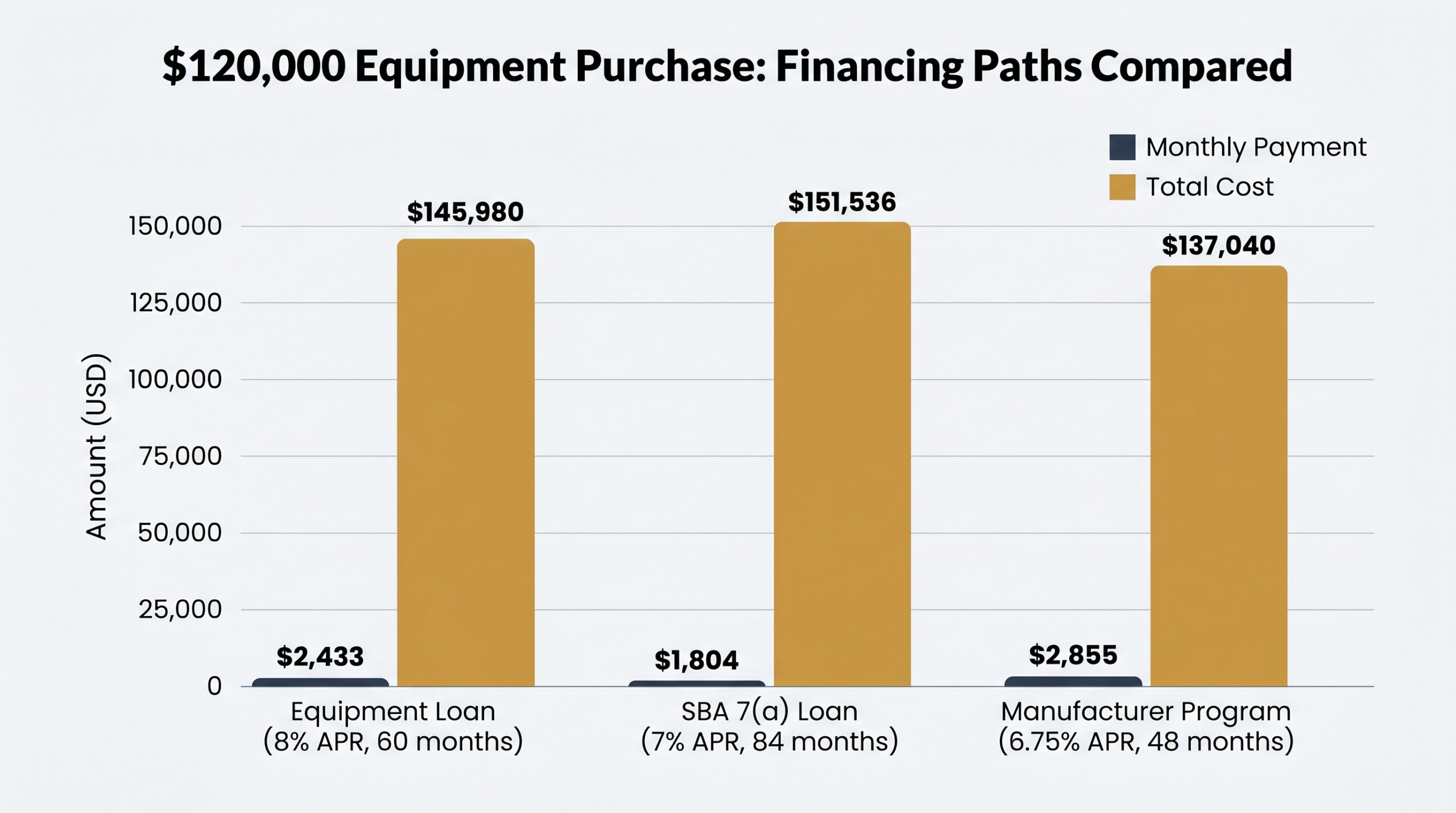

Scenario: A laundromat owner finances $120,000 in new equipment, 10 front-load washers at $5,000 each, 6 dryers at $6,500 each, and a card-based payment system at $5,000.

| Financing Path | Rate | Term | Monthly Payment | Total Cost |

|---|---|---|---|---|

| Equipment Loan | 8% APR | 60 months | ~$2,433 | ~$145,980 |

| SBA 7(a) Loan | 7% APR | 84 months | ~$1,804 | ~$151,536 |

| Manufacturer Program | 6.75% APR | 48 months | ~$2,855 | ~$137,040 |

The tradeoffs are clear. The SBA loan delivers the lowest monthly payment but costs more overall, and takes weeks to fund. The manufacturer program carries the lowest total cost but locks you into specific equipment and requires stronger credit. The equipment loan splits the difference on both.

These are approximate figures. Use our equipment financing calculator to model your specific loan amount, rate, and term before committing to any path.

Tax Advantages of Financing Laundromat Equipment

Laundromat equipment financing doesn’t just spread your costs, it can generate significant tax savings in the year you put equipment into service. Most guides don’t get into this, so it’s worth spending a minute on.

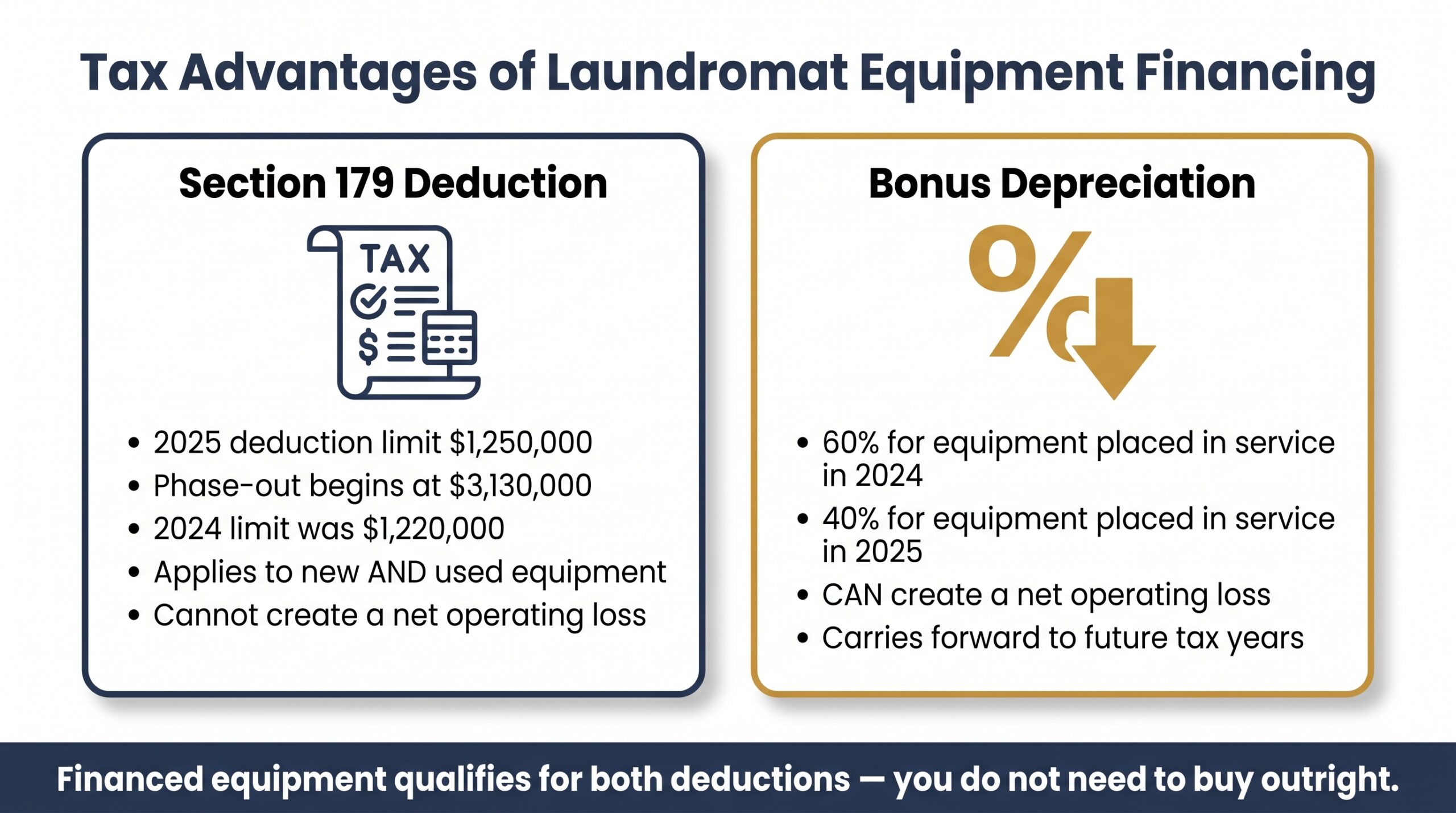

Section 179 Deduction

For 2025, according to the IRS, Section 179 lets you deduct up to $1.25 million in qualifying equipment purchases, with the phase-out beginning at $3.13 million. The 2024 limit was $1.22 million. Commercial washers, dryers, water heaters, and payment systems all qualify. So does used equipment, as long as it’s new to your business and used 50%+ for business purposes.

One constraint worth knowing: Section 179 can’t create a net operating loss. If your deduction would push you into negative income territory, the excess carries forward, it doesn’t disappear, but it doesn’t help you this year either.

Bonus Depreciation

Bonus depreciation works alongside Section 179 but under different rules. Equipment placed in service in 2024 qualifies for 60% bonus depreciation. For 2025, that drops to 40% under the current phase-down schedule. Unlike Section 179, bonus depreciation can create a net operating loss, which may carry forward to future tax years, making it a useful tool for operators expecting near-term losses.

Practical impact: an owner financing $120,000 in equipment could potentially deduct a substantial portion in year one, meaningfully reducing net tax liability. For a full breakdown of how financing structures interact with these deductions, see equipment financing explained. Always consult a tax professional before applying these strategies.

Financing vs. Buying Outright: Pros and Cons

Cash purchases feel clean. No payments, no interest, no lender. But for most laundromat operators, financing is the smarter operational call, and here’s why.

| Financing | Buying Outright | |

|---|---|---|

| Cash Preservation | ✓ Keeps reserves intact | ✗ Depletes working capital |

| Total Cost | ✗ Higher due to interest | ✓ No interest paid |

| Ownership | ✓ Immediate (loans) or end-of-term (leases) | ✓ Immediate |

| Tax Timing | ✓ Section 179 and bonus depreciation still apply | ✓ Same deductions available |

| Business Credit | ✓ Builds credit history | ✗ No credit benefit |

| Approval Required | ✗ Yes, takes time | ✓ No approval needed |

| Personal Guarantee | ✗ Often required | ✓ Not applicable |

Laundromats are capital-intensive from day one. Utilities, lease payments, supplies, and marketing all compete for the same cash. Draining your reserves to buy equipment outright leaves almost no buffer for the first 90 days of operation, when revenue is still ramping up and surprises are most likely.

Financing preserves that buffer. And since Section 179 applies to financed equipment too, you’re not giving up the tax benefit to keep your cash. For most operators, that’s a pretty straightforward decision.

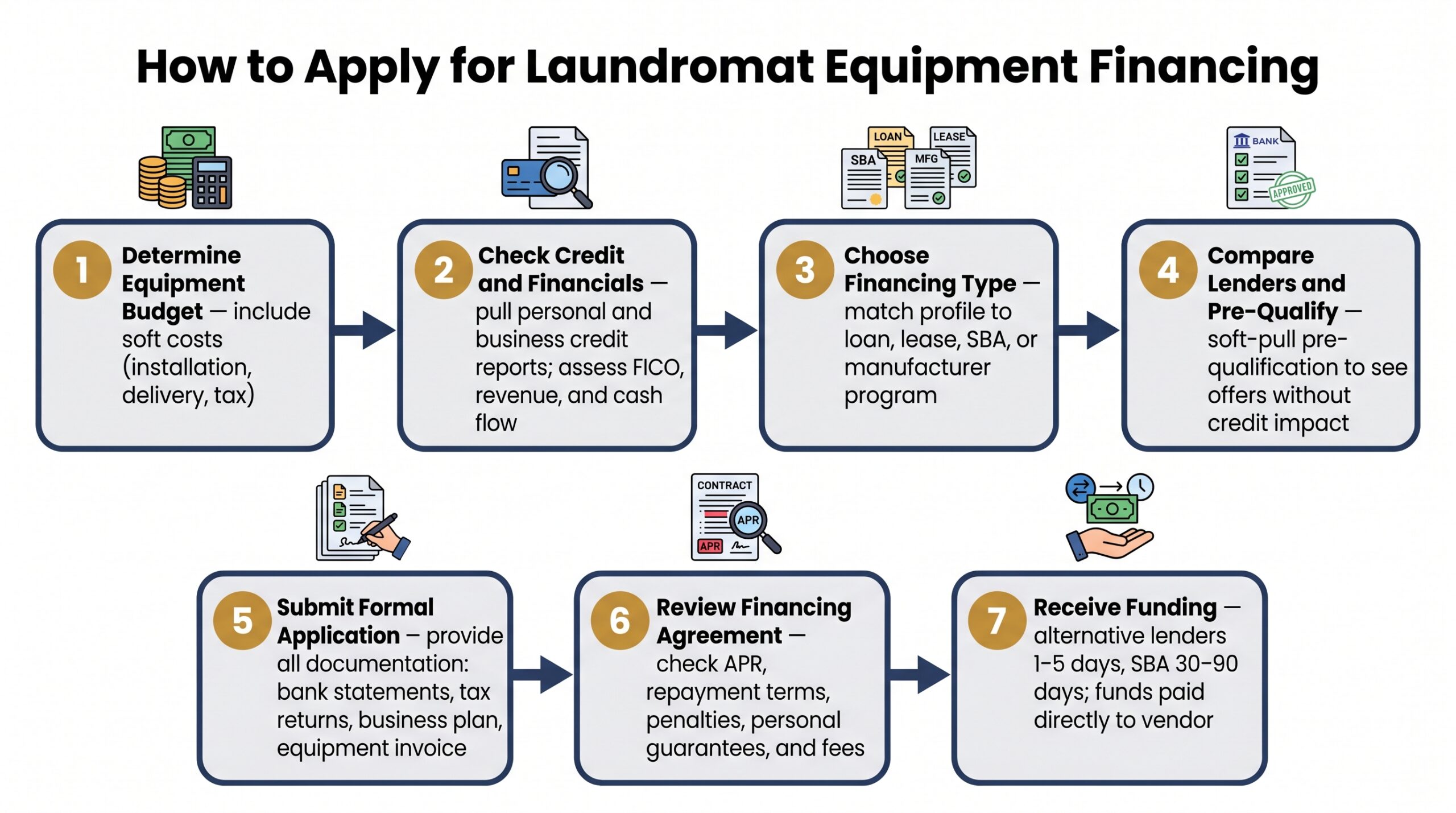

How to Apply for Laundromat Equipment Financing: Step-by-Step

- Determine your equipment needs and total budget. Get vendor quotes and include soft costs, installation, delivery, and plumbing can add $5,000–$15,000 to a mid-size build-out.

- Check your credit and business financials. Pull both personal and business credit reports. Gather two years of tax returns and 3–12 months of bank statements before approaching any lender.

- Choose the right financing type. Match your credit profile, time in business, and cash flow to the appropriate structure using the comparison table in Section 4.

- Compare lenders and pre-qualify. Many lenders offer soft-pull pre-qualification that won’t affect your credit score. Review the best equipment financing companies before submitting anything formal.

- Submit your formal application. Provide all documentation outlined in Section 6, incomplete applications slow everything down, sometimes by weeks.

- Review the financing agreement carefully. Check APR, total repayment amount, prepayment penalties, balloon payments, and personal guarantee terms. Our guide to the equipment financing agreement covers every clause worth scrutinizing.

- Receive funding and purchase equipment. Alternative lenders typically fund in 1–5 business days. SBA loans run 30–90 days. Plan your equipment delivery and installation timeline accordingly.

Tips for Getting the Best Rate on Laundromat Equipment Financing

- Improve your credit before applying. Moving from 650 to 700 can shave a full percentage point or more off your rate. On a $120,000 loan over 60 months, that’s real money.

- Document card-based revenue. Digital transaction records simplify underwriting. Lenders price risk lower when they can verify income cleanly. Coin-op operators should prepare utility correlation data as a supplement.

- Get 3–5 quotes minimum. Use an equipment financing broker to compare multiple lenders with a single soft pull instead of accumulating hard inquiries.

- Put more down if you can. A larger down payment reduces lender risk and typically earns a lower rate in return.

- Watch manufacturer promotions. Alliance Laundry Systems brands, Huebsch, UniMac, Dexter, run seasonal programs with rates as low as 5.75%–6.75%. Timing your purchase to these windows cuts total cost significantly.

- Bundle soft costs into financing. Ask whether installation, delivery, and plumbing can be rolled into the loan. Reducing out-of-pocket expenses at closing protects your working capital.

- Mind your year-end timing. Equipment must be purchased and placed in service before December 31 to qualify for Section 179 in that tax year. Don’t let a delayed delivery push your deduction into the following year.

Frequently Asked Questions About Laundromat Equipment Financing

Can I finance laundromat equipment with bad credit?

Yes. Alternative lenders accept scores as low as 550–600, and some leasing programs go below 500 with strong documented revenue. You’ll pay higher rates, but approval is possible. See our guide to equipment financing with no credit check for low-credit paths.

Can a startup laundromat get equipment financing?

Yes, through manufacturer programs, alternative lenders, or SBA loans backed by strong personal credit and a solid business plan. Expect a larger down payment, 20%–30% is typical, and a personal guarantee will almost certainly be part of the deal.

What is the minimum loan amount for laundromat equipment financing?

Most equipment lenders start at $5,000–$10,000. Manufacturer programs typically require a minimum of $10,000–$25,000. For smaller purchases like a single payment system, alternative lenders are your most flexible option.

Can I finance used or refurbished laundromat equipment?

Yes. Most equipment lenders, including Trust Capital and Western Equipment Finance, finance used and refurbished machines. Some lenders impose age limits, typically 10–15 years, or require an equipment inspection before funding.

How long does it take to get approved for laundromat equipment financing?

Alternative lenders approve and fund in 1–5 business days. Traditional banks and SBA loans run 2–8 weeks. If you need equipment fast, an alternative lender or manufacturer program is the faster path, by a wide margin.

Is laundromat equipment financing tax-deductible?

Yes. Financed equipment still qualifies for Section 179 and bonus depreciation in the year it’s placed in service. You don’t need to own it outright to claim the deduction; the financing structure doesn’t disqualify you.

What’s the difference between an equipment loan and an equipment lease for a laundromat?

A loan gives you ownership from day one and uses the equipment as collateral. A lease typically requires less upfront, may keep the liability off your balance sheet, and offers flexibility to upgrade at term end. If you’re planning to keep the equipment long-term, a loan will almost always cost less over time.

Ready to move forward? Nanotom Capital works with laundromat owners at every stage, startup builds, mid-size expansions, and full-fleet replacements. Get pre-qualified for laundromat equipment financing today with no impact to your credit score, and have a funding decision in as little as 24 hours.

Founder of Nanotom Capital & Nanotom Labs