Key Takeaways

- Used equipment financing rates range from 7%–20% in 2026; your credit score, loan amount, and the equipment’s age all determine where you land in that range.

- Most lenders apply an “age plus loan term” rule: the equipment’s current age combined with your proposed loan term can’t exceed 12–15 years, or expect a decline.

- Age limits vary by asset type; medical and tech equipment caps out at 3–5 years, commercial trucks at 7–10 years, and construction equipment at up to 15 years.

- Used equipment fully qualifies for the Section 179 deduction, which allows up to $2.5 million in write-offs for 2026, as long as the equipment is new to your business and used more than 50% for business purposes.

- Approvals from online lenders typically come within 24–72 hours; SBA loans take 2–6 weeks. Factor that timeline into your purchase plan.

- A third-party appraisal before applying on any equipment over 8 years old or valued above $100,000 speeds up approval and gives the lender a defensible collateral baseline.

- CAT Financial offers both loans and leases on pre-owned CAT machinery with down payments ranging from 0–30%, including limited-time promotional rates as low as 0% on qualifying used equipment.

Buying new equipment drains cash fast, and most businesses can’t afford to do it outright. Used equipment financing solves that by spreading the cost of pre-owned machinery over time, keeping your working capital intact.

This guide covers everything lenders don’t advertise upfront, from age restrictions and appraisal requirements to CAT financing and Section 179 tax advantages.

What Is Used Equipment Financing?

Used equipment financing is a business loan or lease that lets you acquire pre-owned machinery, vehicles, or technology by making fixed payments over a set term instead of paying the full purchase price upfront. The equipment itself typically serves as collateral.

“Used” simply means new to your business. A 2-year-old excavator qualifies just as much as a 15-year-old CNC machine, though lenders treat them very differently based on age and condition.

This financing type applies across virtually every industry, from construction and agriculture to healthcare and manufacturing. According to the Equipment Leasing & Finance Foundation, 82% of U.S. companies use some form of financing when acquiring equipment.

If you’re starting from scratch, get grounded in what equipment financing is before going deeper.

How Does Used Equipment Financing Work?

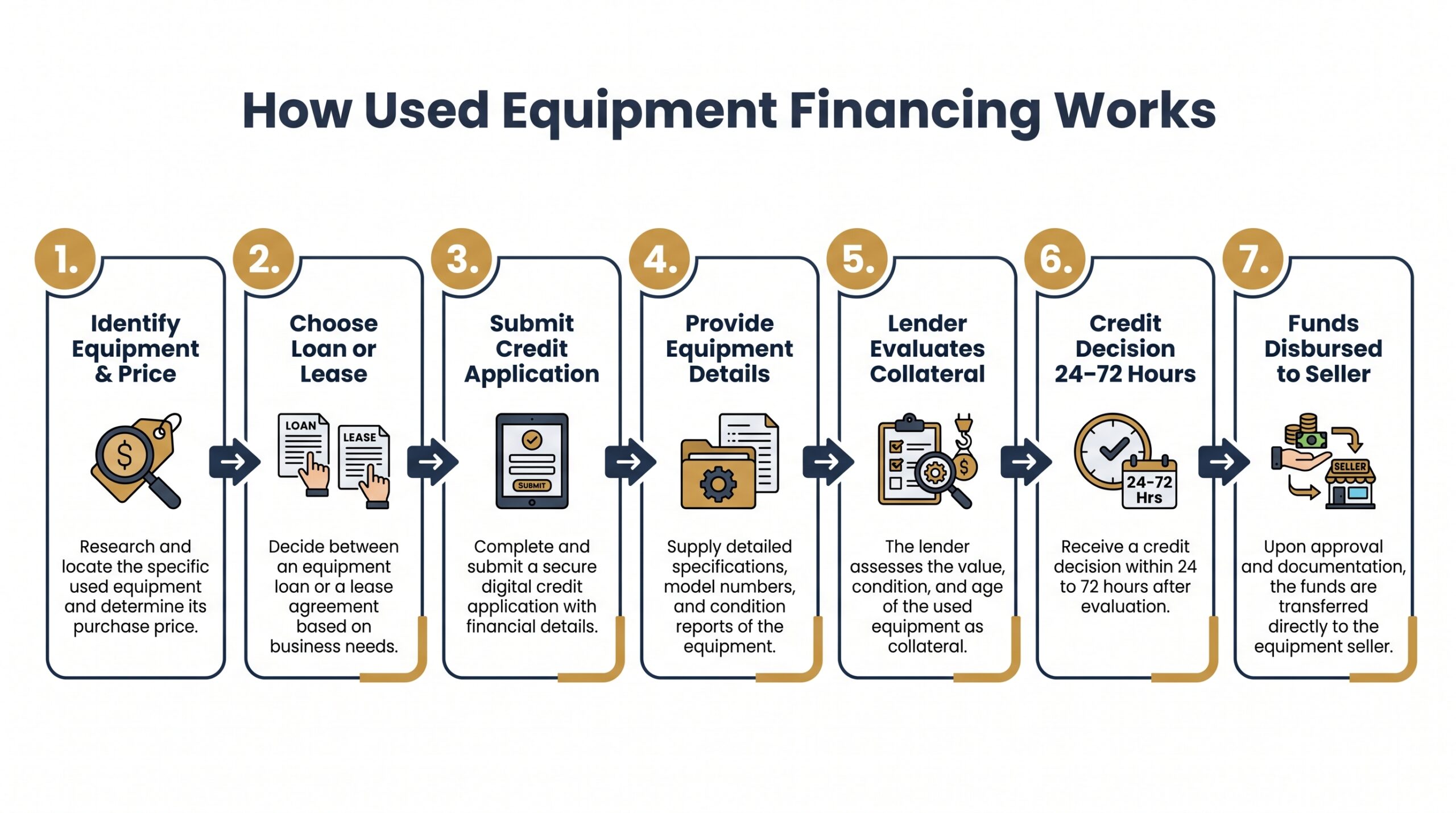

The process is more straightforward than most people expect. Most approvals happen within 24–72 hours, and funds go directly to the seller. Here’s exactly how it works:

- Identify the equipment and confirm the purchase price. Get a firm quote or invoice from the seller before applying.

- Choose a financing type. Decide between a loan (you own it from day one) or a lease (lower payments, flexible end-of-term options).

- Submit a credit application to your chosen lender, whether that’s a bank, credit union, or online lender.

- Provide equipment details. Age, make, model, serial number, photos, and current condition all factor into the lender’s decision.

- Lender evaluates credit, equipment value, and collateral. Used equipment gets scrutinized harder than new.

- Receive a credit decision; typically within 24–72 hours for smaller deals.

- Funds are disbursed directly to the seller. You take possession and start making payments.

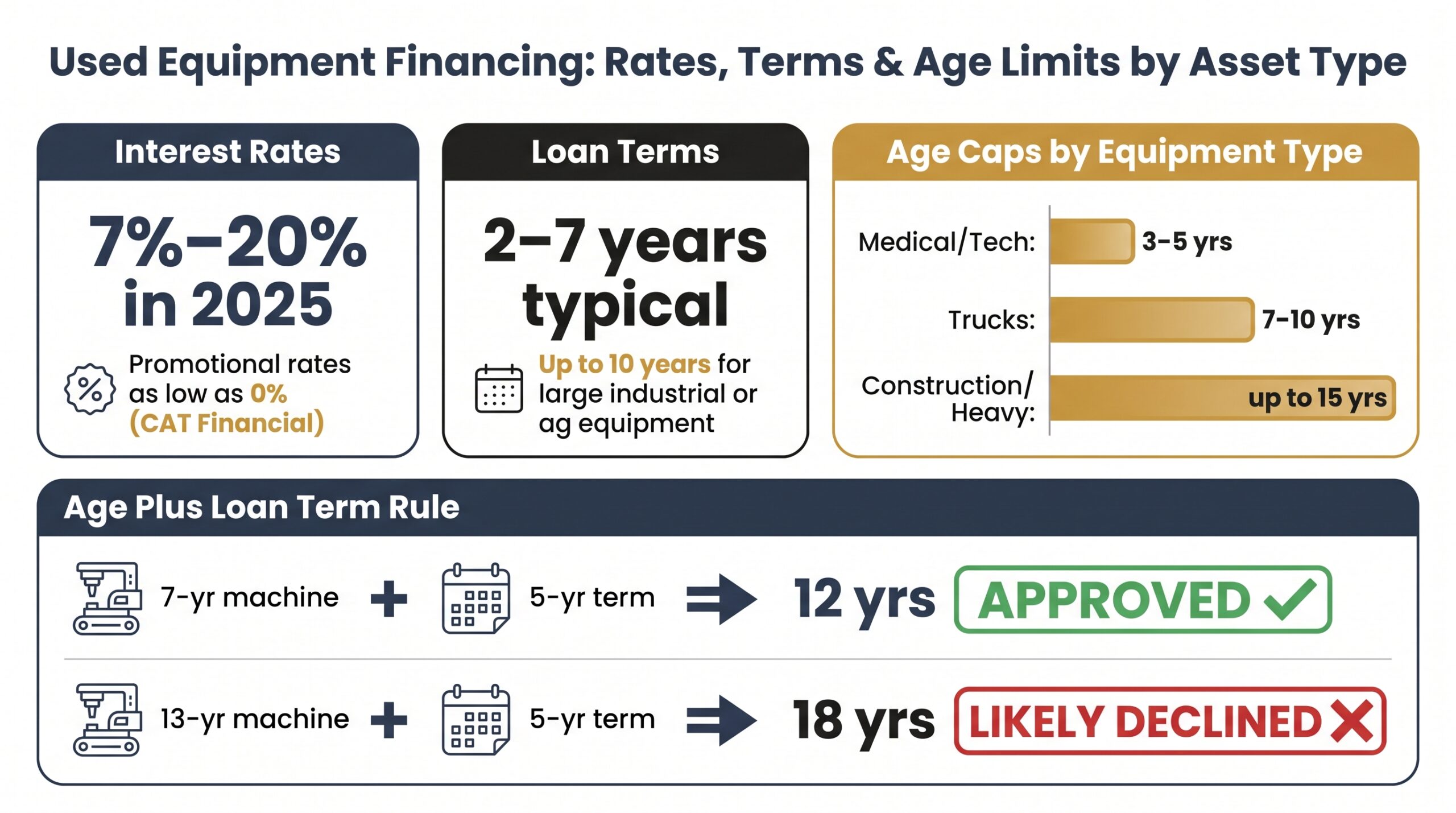

Terms for financing used equipment typically run 2–7 years. Rates range from 7%–20% depending on your credit profile, loan amount, and how old the equipment is.

Types of Used Equipment You Can Finance

Used equipment financing works across virtually every industry. Sources include dealer inventory, auctions, and private party sales, and lenders treat each source a little differently.

Construction and Heavy Equipment

Excavators, cranes, and bulldozers are among the most commonly financed assets. Most lenders allow equipment up to 10–15 years old, making construction equipment financing one of the most flexible categories available.

Agricultural and Farm Equipment

Tractors, combines, and harvesters qualify easily. Niche programs like AgDirect and CAT Financial offer specialized terms for farm equipment financing.

Medical and Dental Equipment

Stricter age limits apply here. Most lenders cap medical equipment financing at 3–5 years old due to rapid obsolescence, so that older imaging system may not qualify no matter how well it runs.

Manufacturing and Industrial Equipment

CNC machines, presses, and lathes hold value well. When an asset has strong resale demand, lenders tend to be more flexible on age.

Transportation and Fleet Equipment

Semi-trucks and commercial vehicles typically face 7–10 year age limits. Commercial truck financing lenders scrutinize mileage just as heavily as age.

Restaurant and Food Service Equipment

Ovens, refrigeration units, and prep equipment all qualify. Restaurant equipment financing on used assets is common, though lenders prefer equipment under 7 years old.

Other Business Equipment

IT hardware, office furniture, and specialty tools can all be financed. Approval depends heavily on resale value and remaining useful life.

Used Equipment Financing Options

Not all financing structures work the same way, and picking the wrong one costs you more than just money. Here are your main options and when each one actually makes sense.

Equipment Loans

You own the equipment from day one, and it serves as collateral. Lenders typically finance 80–100% of appraised value, depending on the asset and your credit profile.

Equipment Leasing

The lender owns the equipment; you make monthly payments with a buyout option at the end. It’s a smart choice for equipment that becomes obsolete quickly. See our equipment leasing vs. financing comparison to decide which fits your situation.

SBA 7(a) Loans for Used Equipment

Flexible and broadly applicable. According to the SBA’s 7(a) loan program, your business must be for-profit, U.S.-based, creditworthy, and unable to secure credit elsewhere on reasonable terms. This works well for smaller businesses that need versatile used equipment financing without the restrictions of more specialized programs.

SBA 504 Loans for Used Equipment

Designed for long-term fixed assets. Per the SBA 504 loan program guidelines, the used equipment must have at least 10 years of remaining useful life, which rules out older or fast-depreciating assets. Your business must also have tangible net worth under $20M and average net income under $6.5M.

Manufacturer and Dealer Financing (Including CAT Financial)

CAT used equipment financing through Cat Financial covers both loans and leases on pre-owned Cat machinery, with down payments ranging from 0–30%. Promotional 0% rate offers exist but are limited-time and credit-dependent. For heavy equipment buyers, this is one of the strongest manufacturer programs out there.

Auction and Private Party Financing

Specialty lenders do fund equipment purchased at auction or from private sellers. Expect to provide an appraisal or third-party inspection report, lenders need to verify value when there’s no dealer standing behind the sale.

Used Equipment Financing Rates and Terms

Interest Rates for Used Equipment

Expect rates between 7%–20% in 2025. Strong credit pushes you toward the lower end; weaker credit or older equipment pushes you higher.

CAT Financial and select manufacturer programs occasionally offer promotional rates as low as 0% on qualifying used equipment, but those windows close fast. See our equipment financing rates guide for a full breakdown.

Loan Terms and Repayment Periods

Most used equipment financing terms run 2–7 years. Large industrial or agricultural assets can stretch to 10 years with the right lender.

Down Payment Requirements

Most lenders require 0–20% down. Specialty and ag-focused lenders may push that to 30% on older or high-risk assets.

How Equipment Age Affects Loan-to-Value Ratios

Here’s what most lenders won’t tell you upfront: many use an “age plus loan term” rule. The equipment’s current age plus your proposed loan term can’t exceed 12–15 years total.

A 7-year-old machine with a 5-year loan term equals 12 years, most lenders approve that. A 13-year-old machine with a 5-year term equals 18 years, expect a decline or a shortened term offer.

Age caps by category: medical and tech equipment top out at 3–5 years, trucks at 7–10 years, and construction equipment at up to 15 years. Use our financing calculator to model different term scenarios before you apply.

How Equipment Appraisal and Inspection Affects Financing

Lenders treat used equipment as higher-risk collateral than new. Before approving financing on a used asset, they need to verify it’s actually worth what you’re paying for it.

Appraisals and inspections are most common in these scenarios:

- Equipment that’s 8+ years old

- Auction purchases where no dealer is vouching for condition

- Private party sales

- High-value assets over $100,000

Lenders typically request photos, serial numbers, maintenance records, hour-meter or odometer readings, a bill of sale, and proof of ownership. Auction purchases often require a qualifying third-party inspection report before the deal can close.

Poor condition or missing maintenance history can kill an approval outright, even if the equipment’s age passes the lender’s cutoff. The equipment itself can be the reason you get declined, not your credit.

Get a third-party appraisal before applying on any older or high-value asset. It speeds up the process and gives the lender a defensible value baseline to work from.

Requirements to Qualify for Used Equipment Financing

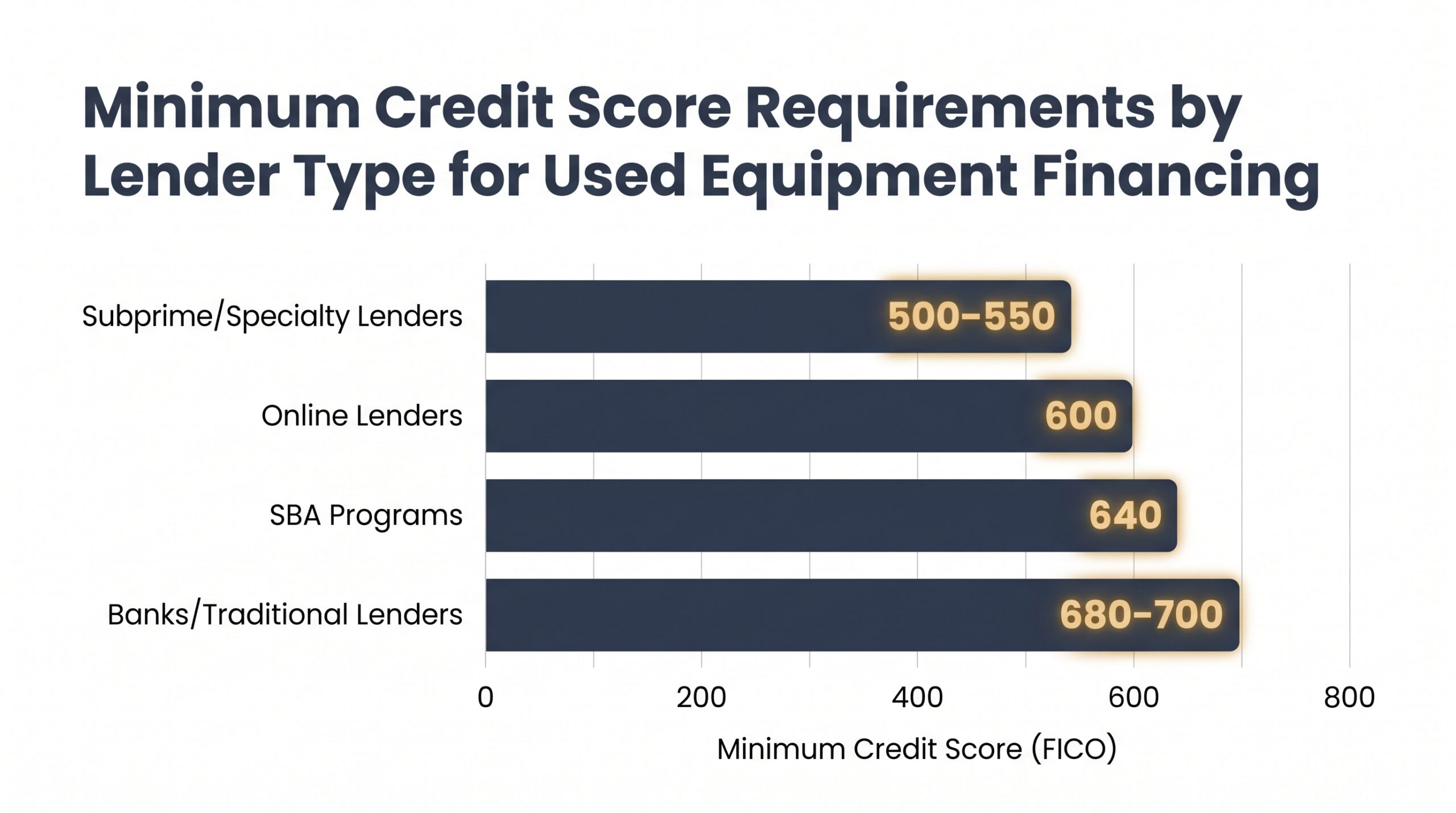

Credit Score Requirements

Banks typically want 680+, often 700+ for best pricing. Online and specialty lenders accept 600+, sometimes 580.

Subprime lenders may go as low as 500–550 with strong compensating factors like solid revenue or a large down payment. SBA programs generally require 640+. If your score is holding you back, check out no credit check equipment financing options.

Time in Business

Traditional lenders want 2+ years. Most online lenders will work with businesses as young as 6–12 months, though rates will reflect the added risk.

Annual Revenue

Revenue thresholds range from $50,000 to $250,000+ depending on the lender. Larger loan amounts naturally require stronger revenue to support the payments.

Equipment Age and Condition

Most lenders finance used equipment up to 10–15 years old depending on asset type, with stricter 3–5 year caps for medical and tech equipment. The equipment must be in working condition, financing something that’s non-operational or undocumented is a non-starter with most lenders. Minimum loan amounts typically start at $5,000.

Tax Benefits of Financing Used Equipment

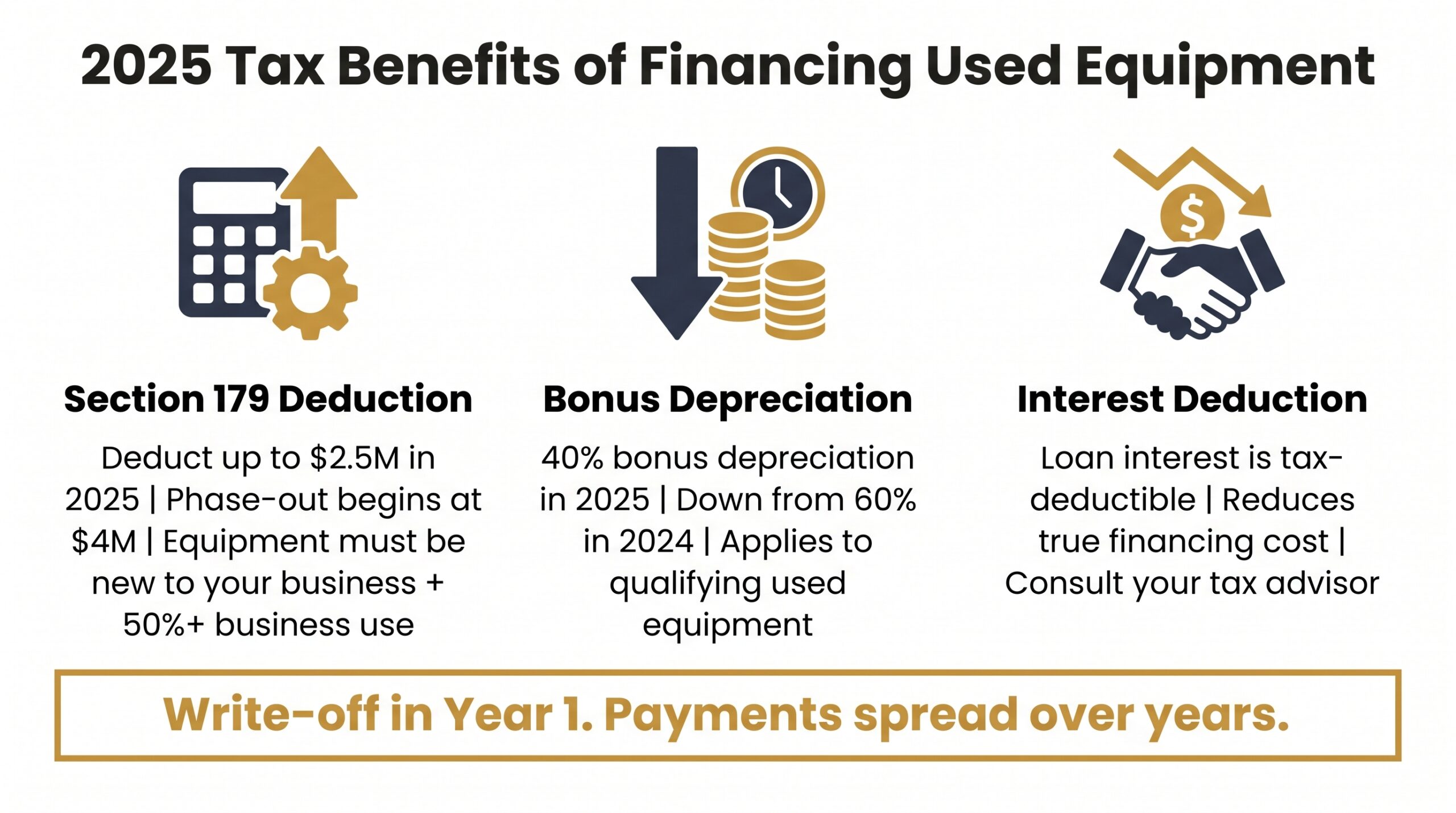

Here’s what most business owners miss: financing used equipment doesn’t disqualify you from significant tax deductions. The write-off comes in year one while payments stretch over years, that’s a real cash flow advantage worth planning around.

Section 179 Deduction: According to Section179.org, businesses can deduct up to $2.5 million in qualifying equipment purchases for 2025. The phase-out begins at $4 million in total purchases. Used equipment fully qualifies as long as it’s new to your business and used more than 50% for business purposes.

Bonus Depreciation: 40% bonus depreciation applies to equipment placed in service in 2025 under current law, down from 60% in 2024. Still meaningful, especially on larger purchases.

Interest Deductions: Interest paid on equipment loans is generally deductible as a business expense, which reduces the true cost of used equipment financing even further.

Combined, these benefits make financing used equipment one of the smarter tax strategies available to small businesses. Always consult a tax advisor for your specific situation.

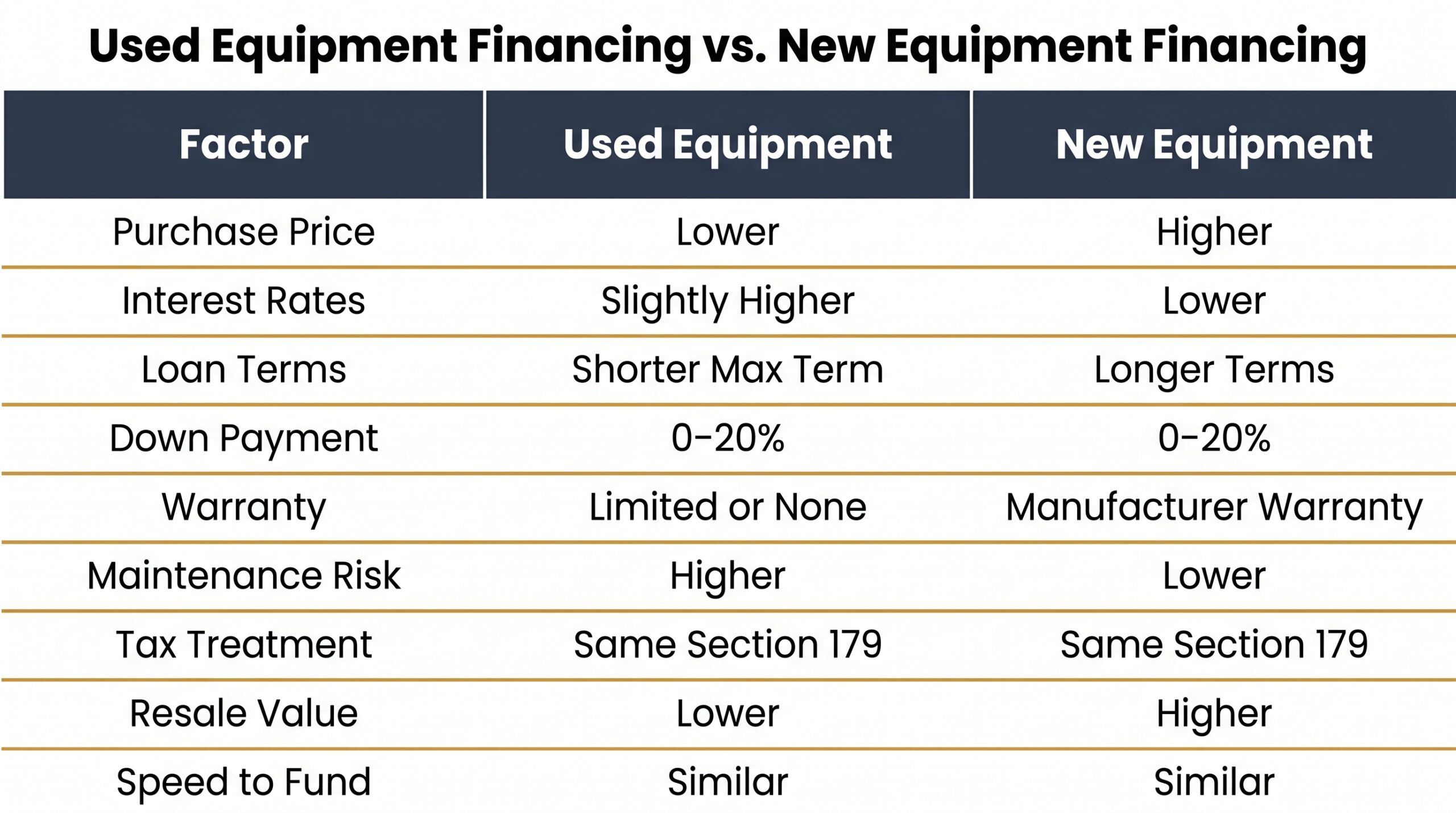

Used Equipment Financing vs. New Equipment Financing

According to the Equipment Leasing and Finance Foundation, 82% of businesses finance equipment regardless of whether it’s new or used. The real question is which path fits your situation. See our full equipment financing guide for broader context.

| Factor | Used Equipment | New Equipment |

|---|---|---|

| Purchase Price | Lower | Higher |

| Interest Rates | Slightly higher | Lower |

| Loan Terms | Shorter maximum term | Longer terms available |

| Down Payment | 0–20% | 0–20% |

| Warranty | Limited or none | Manufacturer warranty |

| Maintenance Risk | Higher | Lower |

| Tax Treatment | Same Section 179 eligibility | Same Section 179 eligibility |

| Resale Value | Lower | Higher |

| Speed to Fund | Similar | Similar |

Used equipment financing wins when capital preservation matters most. New financing makes more sense when warranty coverage and peak productivity are non-negotiable.

Pros and Cons of Financing Used Equipment

Used equipment financing isn’t the right move for every business. Here’s an honest look at both sides.

| Pros | Cons |

|---|---|

| Lower purchase price means lower monthly payments | Interest rates run higher than new equipment financing |

| Preserves working capital for operations | Stricter age and condition requirements from lenders |

| Same Section 179 tax deductions as new equipment | Potential for higher maintenance and repair costs |

| Available immediately, no manufacturer lead times | Shorter maximum loan terms than new equipment |

| Wide lender market: banks, dealers, online lenders | May require third-party appraisal or inspection |

| Strong option for budget-conscious businesses | Limited or no manufacturer warranty coverage |

The lower entry cost of financing used equipment is real, and so is the maintenance risk. A machine that saves you $40,000 upfront can cost you more if it’s unreliable in the field. Know your asset before you commit.

Tips for Getting the Best Used Equipment Financing Deal

- Run the age-plus-term math first. Before you apply, add the equipment’s current age to your desired loan term. If it exceeds 12–15 years, find a shorter term or a different lender before wasting a credit inquiry.

- Get a pre-purchase appraisal. On older or high-value equipment, a third-party appraisal speeds up approval and protects you from overpaying.

- Document everything. Maintenance records, hour-meter readings, and service history make lenders more comfortable and can get you better pricing on used equipment financing.

- Compare at least 3 lenders. Banks, online lenders, and dealer financing each have different appetites for risk. Check out the best equipment financing companies or work with an equipment financing brokers to shop multiple options fast.

- Negotiate. Used equipment deals have more flexibility than sellers advertise. Push on rate, term, and down payment.

- Time your Section 179 deduction. Equipment placed in service before December 31st qualifies for that tax year’s deduction. Don’t let a slow close push you into January.

- Watch for red flags. Sellers refusing to provide serial numbers, missing maintenance records, or “as-is” listings with no inspection access are warning signs for your mechanic and your lender.

How to Apply for Used Equipment Financing

- Identify the equipment. Have the make, model, year, serial number, purchase price, and seller type ready. Lenders treat dealer, auction, and private party sales differently.

- Gather your documents. You’ll typically need 3–6 months of business bank statements, 1–2 years of tax returns, a government-issued ID, business formation documents, and equipment photos or details.

- Check your qualifications. Compare your credit score and time in business against each lender’s minimums before applying and burning a credit inquiry.

- Compare lenders. Bank, online lender, SBA, and dealer financing all have different rates, terms, and approval speeds for used equipment financing.

- Submit your application. Online lenders typically decide in 24–72 hours. Banks and SBA lenders take 2–6 weeks.

- Review your financing agreement carefully. Check the rate, term, fees, and prepayment penalties before signing. Our equipment financing agreement guide breaks down exactly what to look for.

- Funding disbursed. The lender pays the seller directly, and you take possession of the equipment.

Frequently Asked Questions About Used Equipment Financing

Can you get a loan on used equipment?

Yes. Banks, credit unions, online lenders, and manufacturer programs like CAT Financial all finance pre-owned equipment. The equipment typically needs to be in working condition and within the lender’s age limits, usually 10–15 years depending on asset type.

What credit score do you need for used equipment financing?

Most online lenders require 600+. Banks typically want 680+. Some specialty and subprime lenders will go as low as 500–580 with strong compensating factors like solid revenue or a large down payment.

How hard is it to get used equipment financing?

Easier than most business owners expect. Online lenders can approve and fund in 24–72 hours if your credit and equipment meet their criteria. SBA loans take longer; plan for 2–6 weeks minimum.

Can you get an SBA loan with a 500 credit score?

The honest answer is: it’s very difficult. Most SBA 7(a) lenders require 640+. At 500, alternative lenders and subprime equipment lenders are more realistic options. Strong revenue or substantial collateral can help, but won’t guarantee SBA approval at that score.

What is the minimum amount you can finance for used equipment?

Most lenders set a $5,000 floor. Some microlenders go as low as $2,000–$3,000 for smaller purchases.

Does financing used equipment qualify for Section 179?

Yes. Used equipment qualifies for Section 179 up to $2.5 million in 2025, as long as it’s new to your business and used more than 50% for business purposes. Financing the purchase doesn’t disqualify you.

If you’re a newer business still building your credit profile, see our guide on startup equipment financing for options built around your situation.

Used equipment financing gives businesses real leverage. Lower entry costs, the same tax benefits as new, and a wide lender market that rewards preparation. Know your equipment’s age, document its condition, compare at least three lenders, and don’t leave Section 179 timing on the table. The businesses that win with used equipment financing aren’t just buying cheaper, they’re buying smarter.

Founder of Nanotom Capital & Nanotom Labs