Key Takeaways

- Equipment loans carry just a 9% denial rate, the lowest of any loan category, because the asset itself backstops the deal, making no credit check approvals structurally viable.

- “No credit check” usually means no hard pull or no minimum FICO, not zero credit review; lenders still assess revenue, bank statements, and equipment resale value instead.

- Most no credit check equipment financing programs require $100K–$250K in annual revenue and 3–4 months of bank statements as the primary approval criteria in place of your credit score.

- Startups can qualify through SBA Microloans (FICO as low as 500, up to $50,000) or lenders like Smarter Finance USA with no hard minimums, but expect a 30–50% down payment to offset the lender’s risk.

- True no credit check financing carries APRs of 10–22%+, compared to 6–9% at traditional banks; the rate premium is the direct cost of skipping your credit history.

- A personal guarantee is required by most no credit check lenders regardless of whether credit was pulled; your personal assets remain on the line even without a credit inquiry.

- High-resale equipment, commercial excavators, semi-trucks, medical imaging devices gets the most flexible underwriting; the more liquid the asset, the better the terms.

Your credit score is tanking your equipment deal, but that doesn’t mean you’re out of options. Equipment financing with no credit check programs exist specifically to get businesses funded based on what matters more: revenue, cash flow, and the value of the equipment itself.

This guide breaks down every real option, names the lenders, and shows you exactly what “no credit check” actually means before you sign anything.

What Is Equipment Financing With No Credit Check?

Equipment financing with no credit check is a funding structure where the lender deprioritizes or entirely skips your personal FICO score, replacing it with other underwriting signals. Those signals typically include your business bank statements, monthly revenue, and the collateral value of the equipment you’re financing. If you’re new to how this works overall, our guide on what is equipment financing covers the foundational mechanics in full.

The equipment itself does the heavy lifting. If you default, the lender seizes and resells it, which is why a $150,000 CNC machine is easier to finance than a $15,000 laptop. That asset-backed security is what makes no credit check equipment financing possible at all.

True No Credit Check vs. Soft Pull: What’s the Real Difference?

Most lenders blur this line. Here’s the honest breakdown.

- True no credit check: The lender runs zero credit inquiry, hard or soft. Approval is based purely on equipment value, business revenue, or both. Rare, but it exists.

- Soft pull: The lender checks your credit without affecting your score. They’re still seeing your history, they’re just not dinging you for the inquiry.

- Alternative underwriting: No minimum FICO is advertised, but lenders review bank statements, time in business, and industry risk instead. Your credit score is still visible; it’s just weighted differently.

REIL Capital, for example, advertises a no-credit-check program for borrowers under FICO 500, underwriting based primarily on equipment condition and resale value. That’s closer to a true no credit check product than most competitors offer.

Why Lenders Often Say “No Credit Check”, And What They Actually Mean

Easy equipment financing marketing loves the phrase “no credit check.” What lenders usually mean is no hard pull or no minimum score requirement; they’re still assessing your business health, just through revenue and asset value instead of your credit file.

When equipment secures the loan, lenders file a UCC-1 lien against it. That lien gives them a legal claim to the asset if you default. It’s the primary reason true no credit check equipment financing is structurally possible without a full creditworthiness review.

How Does No Credit Check Equipment Financing Work?

The approval logic is straightforward: if the equipment holds enough resale value, the lender’s risk drops low enough that your credit score becomes secondary. The Federal Reserve’s 2024 Small Business Credit Survey found equipment loans carry just a 9% denial rate, the lowest of any loan category, largely because the asset itself backstops the deal.

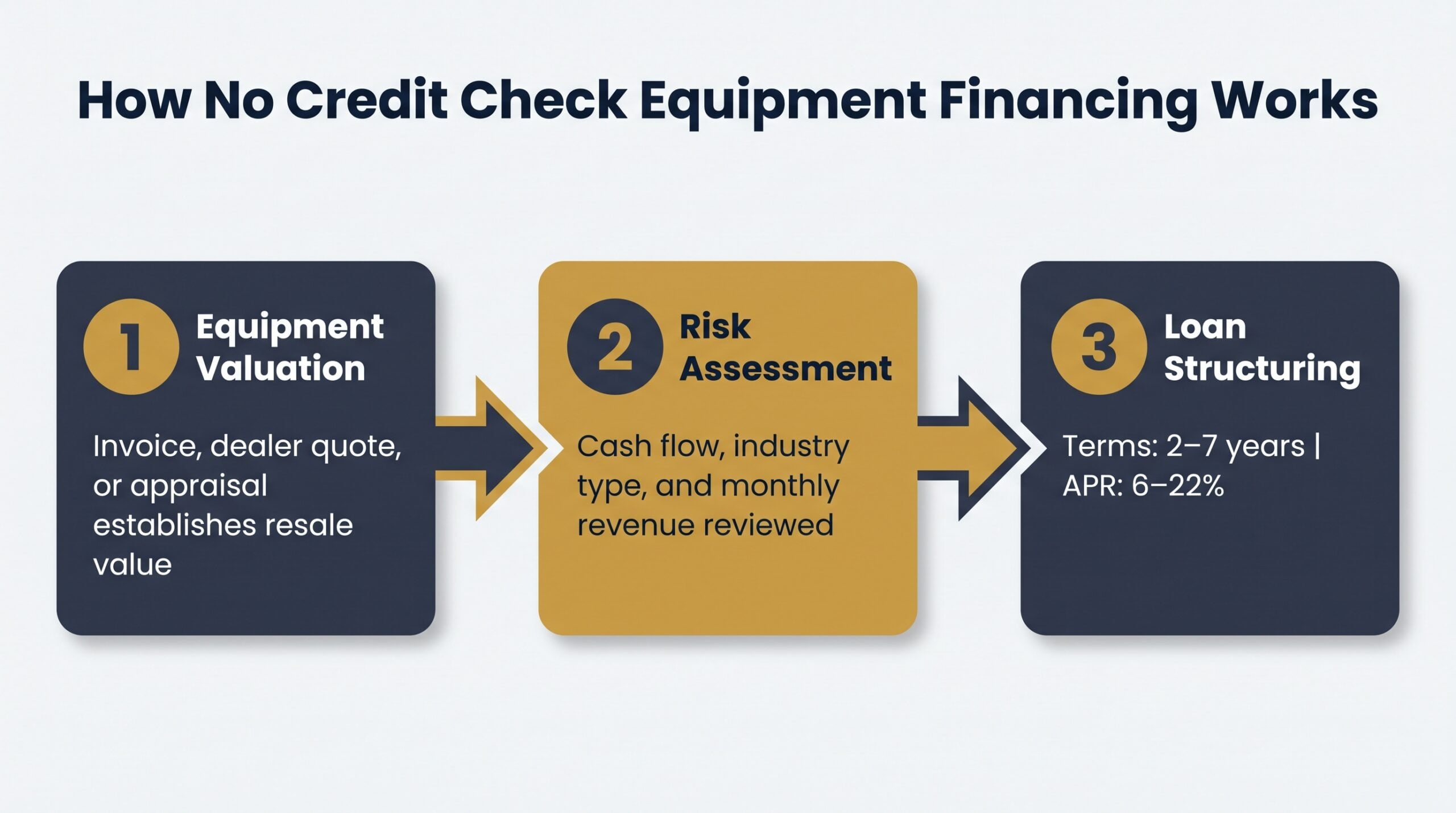

Here’s the three-step process most no credit check equipment financing lenders follow:

- Equipment valuation: The lender establishes resale value through the purchase invoice, dealer quote, or independent appraisal.

- Risk assessment: Cash flow, industry type, and business revenue are reviewed to confirm repayment capacity.

- Loan structuring: Terms typically run 2–7 years with APRs ranging from 6–22%, depending on asset quality and business profile.

Lenders like Smarter Finance USA and REIL Capital calculate a borrowing base, usually 60–100% of the equipment’s resale value. The stronger that ratio, the more likely a soft pull or no pull gets approved.

Equipment Value as the Primary Approval Driver

High-demand equipment with strong resale markets gets the most flexible underwriting. A refrigerated semi-trailer or a commercial excavator is easier to finance without a credit check than niche or rapidly depreciating assets.

Lenders know exactly what they can recover if the loan goes sideways. That recoverability calculation is what makes equipment financing no credit check products structurally viable. Your credit score is just one more data point, and often not the deciding one.

Alternative Qualifying Criteria: Revenue, Bank Statements, and Time in Business

When credit steps back, these metrics step forward:

- Annual revenue: Most lenders want $100K–$250K minimum to confirm repayment capacity.

- Bank statements: 3–4 months of statements show cash flow consistency and average daily balance.

- Time in business: 6 months is the floor for most programs; 2 years unlocks better rates and higher advance amounts.

Easy equipment financing through alternative criteria isn’t a loophole. It’s a legitimate underwriting model built around business performance instead of personal credit history.

Types of No Credit Check Equipment Financing Options

Not all no credit check equipment financing products work the same way. Here are the five main structures, who they’re built for, and what each one actually costs.

Equipment Leasing

Leasing sidesteps credit requirements because the lender retains ownership of the equipment throughout the term. The asset itself is the collateral, so approval leans on equipment value over borrower creditworthiness.

- How it minimizes credit checks: Lessor owns the asset, reducing default risk significantly.

- Ideal for: Businesses needing frequent equipment upgrades or those with thin credit files.

- Typical terms: 2–5 years, rates from 6–15% depending on asset type.

- Example: A restaurant financing commercial ovens through restaurant equipment financing, or a medical practice acquiring imaging equipment through medical equipment financing.

See how leasing stacks up against ownership in our equipment leasing vs. financing breakdown.

Revenue-Based Financing

Here the lender underwrites based on monthly revenue, not credit score. Many programs accept FICO scores as low as 500.

- How it minimizes credit checks: Revenue consistency replaces creditworthiness as the primary signal.

- Ideal for: Businesses with strong sales but bruised credit.

- Typical terms: Repayment tied to a fixed percentage of monthly revenue, usually 6–24 months.

- Example: A landscaping company with seasonal cash flow spikes qualifying based on peak-season revenue averages. Businesses in this industry can explore dedicated landscaping equipment financing with bad credit programs built specifically for their approval profile.

Merchant Cash Advances for Equipment

MCAs advance capital against future receivables. Approval is fast (sometimes same-day), and credit history carries minimal weight.

- How it minimizes credit checks: Future sales volume drives approval, not past credit behavior.

- Ideal for: High-revenue businesses needing equipment quickly.

- Typical terms: Factor rates from 1.15–1.45, repayment via daily or weekly revenue splits.

- Example: A food truck operator funding a commercial generator before peak festival season, see our guide to food truck equipment financing for options tailored to mobile businesses.

MCAs are easy equipment financing to access, but the effective APR can be high. Use them strategically, not as a default.

Sale-Leaseback Agreements

You sell equipment you already own to a lender, then lease it back. You get immediate capital; they get the asset as collateral.

- How it minimizes credit checks: The transaction is secured by owned assets, not creditworthiness.

- Ideal for: Asset-rich businesses needing working capital.

- Typical terms: Lease terms of 2–5 years, rates vary by asset condition and type.

- Example: A laundromat owner unlocking $80,000 in capital from paid-off commercial washers and dryers.

Vendor Financing Programs

Manufacturers and dealers sometimes underwrite deals directly, often offering 0% promotional rates to move inventory. Credit requirements are frequently more flexible than traditional lenders.

- How it minimizes credit checks: Vendor absorbs risk to close the sale; approval criteria are looser by design.

- Ideal for: Businesses buying new equipment from major manufacturers or authorized dealers.

- Typical terms: 0–5% promotional rates for 12–36 months, standard rates after promotional period.

- Example: A contractor purchasing excavators through a dealer program, explore more in our construction equipment financing guide.

Who Qualifies for Equipment Financing Without a Credit Check?

Qualification thresholds vary significantly by lender and product type. Here’s what actually moves the needle.

Minimum Revenue and Time-in-Business Requirements

For established businesses, most no credit check equipment financing programs want to see:

- Annual revenue: $100K–$250K minimum, verified through bank statements or tax returns.

- Time in business: 6 months at the floor; 2 years unlocks the best terms and highest advance amounts.

- Bank statements: 3–4 months showing consistent deposits and a healthy average daily balance.

These thresholds replace your credit score as the primary approval signal. Strong revenue with thin credit still gets deals done.

Startup-Specific Pathways With No Credit History

Startups aren’t automatically disqualified. Lenders like Smarter Finance USA evaluate applications case by case with no hard minimums on credit score, revenue, or time in business.

SBA Microloans accept FICO scores as low as 500 and fund up to $50,000, a realistic entry point for early-stage businesses. The tradeoff is a larger down payment, typically 30–50%, to offset the lender’s increased risk exposure.

Our startup equipment financing guide covers every available pathway in detail.

Industry Types That Get Approved Most Easily

Easy equipment financing approvals cluster around industries where equipment holds strong resale value. If a lender can repossess and resell quickly, they’ll underwrite more aggressively.

- Construction: Excavators, cranes, and loaders retain value and have deep secondary markets.

- Trucking: Semi-trucks and trailers are liquid assets; explore trucking equipment financing options.

- Medical: Imaging and diagnostic equipment commands strong resale prices.

- Restaurant: Commercial kitchen equipment has consistent demand in the secondary market.

- Agriculture: Tractors and combines hold value well; see agricultural equipment financing for specifics.

The pattern is consistent: the more liquid the equipment, the more flexible the no credit check equipment financing terms.

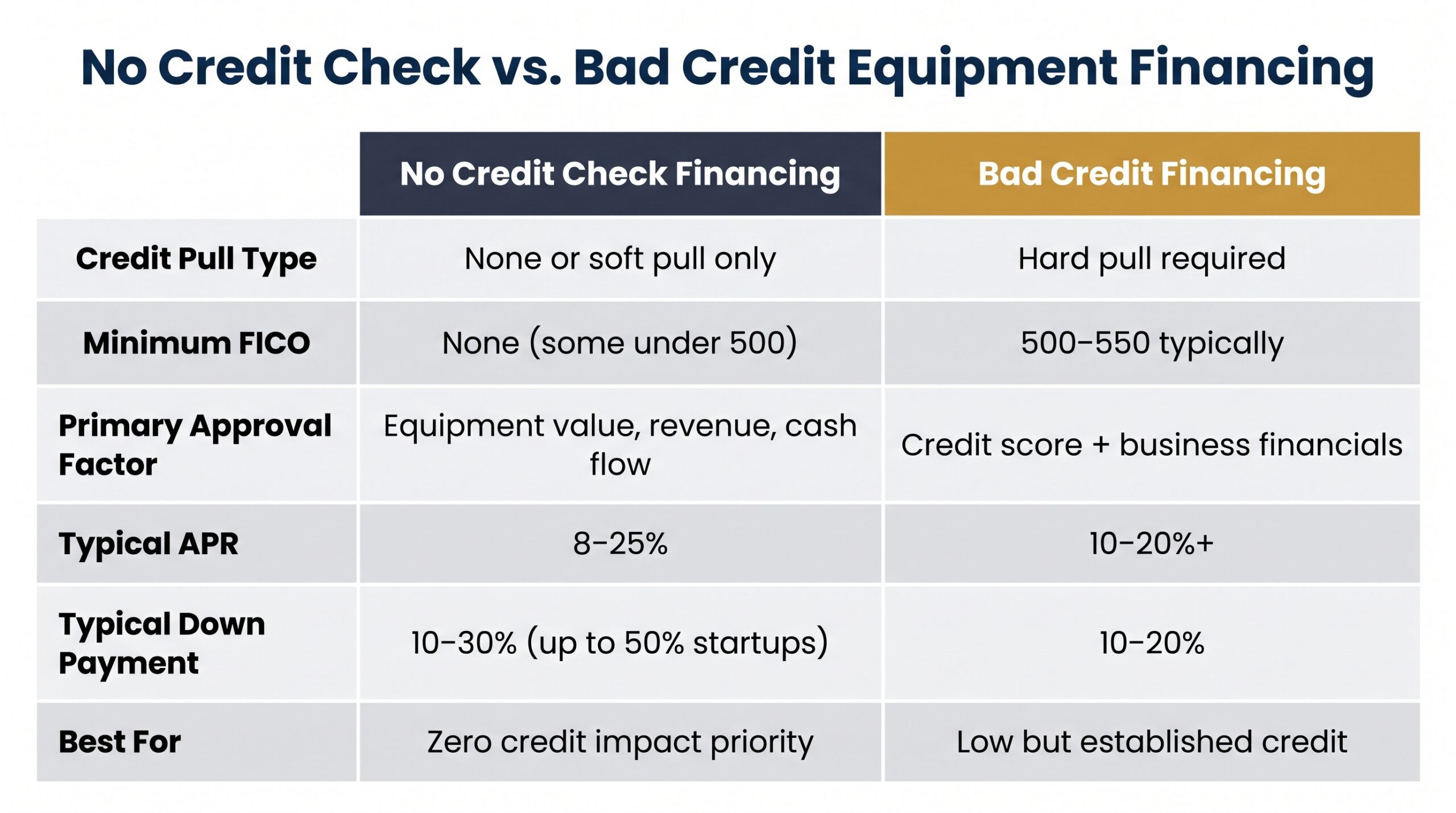

No Credit Check vs. Bad Credit Equipment Financing: What’s the Difference?

These two terms get used interchangeably online. They’re not the same thing, and confusing them can cost you time and unnecessary hard inquiries on your credit file.

No credit check equipment financing means the lender skips the credit pull entirely, or runs a soft pull only, and bases approval on asset value, revenue, or cash flow. Bad credit financing means the lender does pull your credit, they’ll just approve lower scores, typically 500–550, at higher rates to compensate for the risk.

| Factor | No Credit Check Equipment Financing | Bad Credit Equipment Financing |

|---|---|---|

| Credit Pull Type | None or soft pull only | Hard pull required |

| Minimum FICO | None (some programs under 500) | 500–550 typically |

| Primary Approval Factor | Equipment value, revenue, cash flow | Credit score plus business financials |

| Typical Rate Range | 8–25% APR (asset-risk dependent) | 10–20%+ APR |

| Typical Down Payment | 10–30% or higher for startups | 10–20% |

| Best For | Businesses wanting zero credit impact | Businesses with low but established credit |

The practical takeaway: if protecting your credit file matters, pursue true no credit check equipment financing first. If your score is low but exists, bad credit financing may offer better rates than you’d expect.

Pros and Cons of No Credit Check Equipment Financing

No credit check equipment financing solves a real problem. But it comes with tradeoffs you need to price in before you commit.

| Pros | Cons |

|---|---|

| Accessible for startups and credit-challenged businesses | Higher interest rates, often 10–22%+ APR |

| Fast approvals, same-day decisions are possible | Larger down payments required, typically 20–50% |

| No hard credit pull protects your score | Shorter repayment windows with some lenders |

| Equipment serves as its own collateral | Restricted to equipment purchases, not working capital |

| Reported payments can build business credit over time | Predatory lenders actively operate in this space |

The speed and accessibility of easy equipment financing is genuinely valuable for businesses that can’t wait through a traditional bank’s 30–60 day underwriting process. A same-day approval on a $75,000 piece of revenue-generating equipment often justifies a higher rate.

The down payment requirement deserves honest attention. If you’re a startup pursuing no credit check equipment financing, budget for 30–50% upfront. That’s not a penalty, it’s the cost of replacing credit history with cash commitment.

That last con on the list, predatory lenders, warrants its own section. The no-credit-check space attracts bad actors specifically because borrowers are vulnerable. Know the red flags before you apply anywhere.

Watch Out: Predatory Lenders in the No Credit Check Space

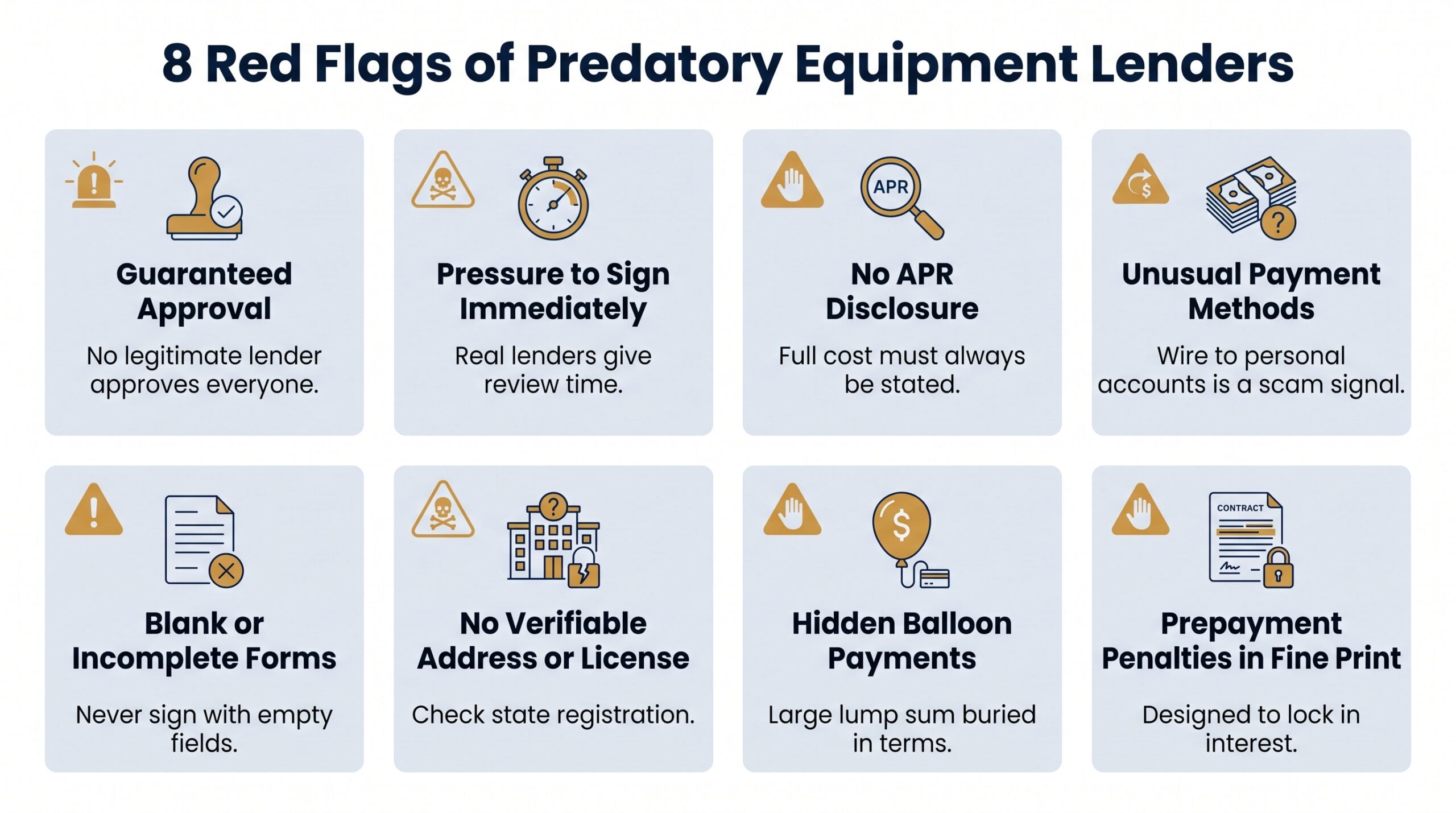

Here’s what most guides skip: the no credit check equipment financing market attracts predatory lenders precisely because borrowers here have fewer options and feel more pressure to say yes. Credit-challenged business owners are the target.

Know what a bad deal looks like before you’re sitting across from one.

Red Flags to Avoid Before You Sign

- Guaranteed approval language: No legitimate lender approves everyone. “100% approval guaranteed” is a marketing lie, not a product feature.

- Pressure to sign immediately: Real lenders give you time to review. Artificial deadlines exist to stop you from comparing offers.

- Missing APR disclosure: Legitimate no credit check equipment financing always discloses the full cost of capital. If APR isn’t stated, walk away.

- Unusual payment requests: Wire transfers to personal accounts, gift cards, or cryptocurrency are not standard lender payment methods. Ever.

- Blank or incomplete forms: Never sign a document with empty fields. They get filled in after you’ve signed.

- No verifiable business address or license: Check state business registrations. Legitimate lenders are findable and licensed.

- Balloon payments buried in terms: A low monthly payment that ends in a massive lump sum is designed to trap you, not help you.

- Prepayment penalties in fine print: Some lenders penalize early payoff to lock in their interest income. Read every fee schedule before signing.

The SBA recommends comparing at least three financing offers before committing. Easy equipment financing shouldn’t mean easy to exploit, and the best lenders operate with full transparency on rates, terms, and fees from the first conversation.

At Nanotom Capital, every offer includes complete APR disclosure, no blank forms, and zero pressure tactics. That’s the baseline for what legitimate no credit check equipment financing looks like.

What to Expect: Rates, Terms, and Requirements

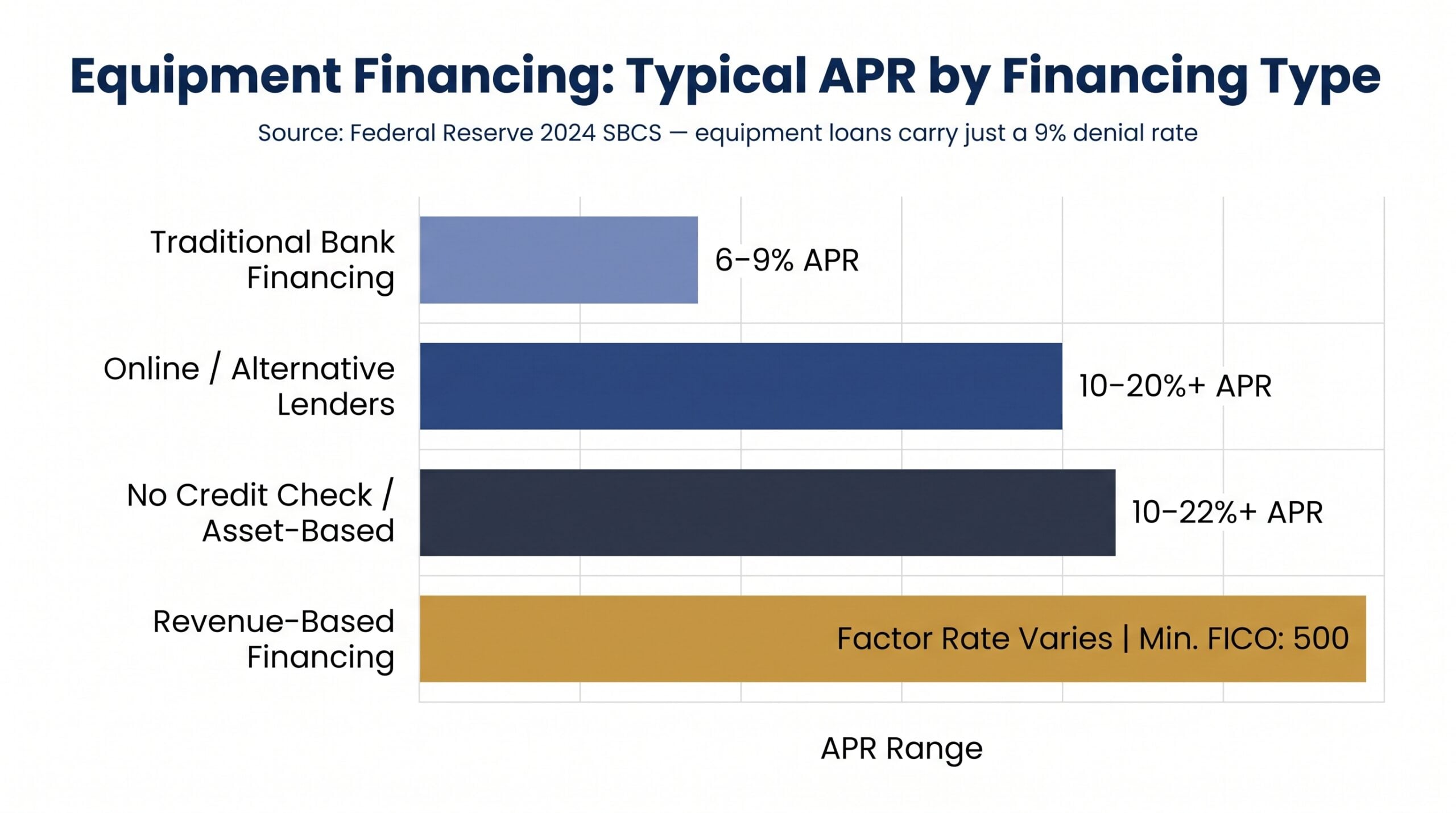

According to the Federal Reserve’s 2024 Small Business Credit Survey, equipment and auto loans had just a 9% denial rate, the lowest of any loan category. Approval is achievable. The real question is what it costs.

Typical Rate Ranges by Financing Type

| Financing Type | Typical APR | Minimum FICO |

|---|---|---|

| Traditional bank financing | 6–9% | 650+ |

| Online / alternative lenders | 10–20%+ | 550–650 |

| No credit check / asset-based programs | 10–22%+ | None |

| Revenue-based financing | Varies (factor rate) | 500 minimum |

For a deeper dive on rate drivers, see our equipment financing rates guide. Use our equipment financing calculator to model your monthly payments before you apply.

Down Payment, Loan Amounts, and Term Length

Here’s what no credit check equipment financing programs typically look like across the core deal structure variables:

- Loan amounts: $10,000–$5,000,000 depending on equipment type and lender appetite.

- Term lengths: 2–7 years, with shorter terms common on higher-risk deals.

- Down payments: 0% for strong-credit borrowers up to 50% for startups with no credit history.

Document requirements are consistent across most easy equipment financing programs:

- EIN and business registration documents

- 3–4 months of business bank statements

- Equipment invoice or dealer quote

- Personal guarantee, required by most lenders regardless of credit check policy

That last point matters. A personal guarantee means your personal assets are on the line even when the lender skips your credit report. Understand what you’re signing.

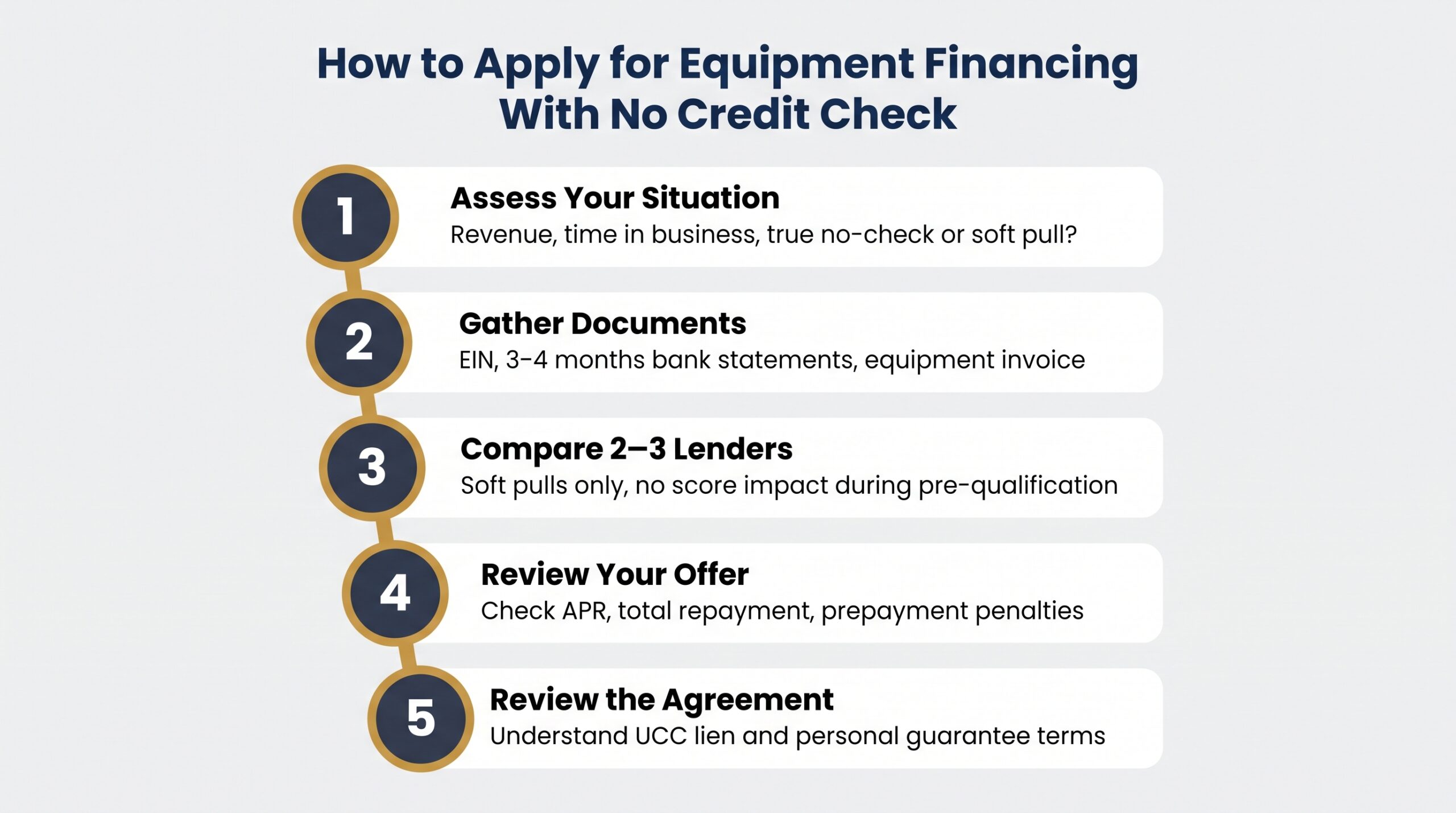

How to Apply for Equipment Financing With No Credit Check

Most no credit check equipment financing applications take under 30 minutes. Here’s the exact process.

Step 1: Determine Which Financing Type Fits Your Situation

Start with your own profile. How long have you been operating? What’s your monthly revenue? Do you need true no-credit-check, or are you okay with a soft pull that won’t affect your score?Your answers narrow the field fast. A startup with no revenue history needs a different product than a 3-year-old business with $300K annual revenue.

Step 2: Gather Your Documentation

Most easy equipment financing applications require the same short document list:

- EIN and business registration or formation documents3–4 months of business bank statementsEquipment invoice or dealer quote with pricingBasic business information, legal name, address, industry type

Having these ready before you apply cuts approval time significantly.

Step 3: Compare Lenders and Get Pre-Qualified

Apply with at least 2–3 lenders. Pre-qualification uses soft pulls only, so your credit score won’t move. If comparing lenders feels overwhelming, an equipment financing broker can shop your profile across multiple programs simultaneously.

Step 4: Submit Your Application and Review Your Offer

Once you select a lender, submit the full application. When the offer arrives, check four things: total repayment amount, APR, prepayment penalties, and end-of-lease or buyout options.The monthly payment number alone tells you almost nothing.

Step 5: Review the Agreement Before Signing

This is where deals go wrong. Look specifically for UCC lien language, most no credit check equipment financing agreements include a lien on the equipment and sometimes broader business assets. Understand your personal guarantee obligations.Our equipment financing agreement guide walks through every clause worth flagging before you sign.

Key Terms Glossary: No Credit Check Equipment Financing

These terms appear in nearly every no credit check equipment financing agreement. Know them before you sign anything.

- UCC-1 Lien

- A legal security interest filed against business assets used as collateral. Most equipment financing agreements include a UCC-1 filing, which gives lenders the right to repossess the equipment if you default.

- Soft Credit Pull

- A credit inquiry that does not affect your credit score. Used during pre-qualification — you can shop multiple lenders without any score impact.

- Hard Credit Pull

- A formal credit inquiry that appears on your credit report and can lower your score by a few points. Triggered when you submit a full loan application with most traditional lenders.

- Equipment Collateral

- The financed asset securing the loan. If payments stop, the lender repossesses and sells the equipment to recover their capital. This is the core mechanic that makes easy equipment financing possible without credit history.

- Borrowing Base

- The percentage of equipment value a lender will finance. A lender with an 80% borrowing base on a $100,000 machine advances $80,000 — you cover the remaining $20,000 as a down payment.

- Personal Guarantee

- A personal promise to repay the debt if your business defaults. Common across no credit check equipment financing programs regardless of whether credit was pulled.

- Revenue-Based Underwriting

- An approval method that weights monthly cash flow and bank deposits over credit score. The primary engine behind most no-credit-check and easy equipment financing programs available today.

Frequently Asked Questions

Can I get equipment financing with bad credit?

Yes. Some lenders approve borrowers with FICO scores as low as 500–550 when revenue is strong or a larger down payment offsets the risk. Bad credit financing and no credit check equipment financing are different products; both are available, but bad credit programs still pull your credit while no-credit-check programs skip it entirely.

What credit score do you need for equipment financing?

Traditional banks typically require 650 or higher. Online and alternative lenders may accept 550–600. True no credit check equipment financing programs have no FICO floor; approval is based on equipment value, revenue, and cash flow instead.

Can you get an SBA loan with a 500 credit score?

The honest answer is: it depends on the program. Standard SBA 7(a) loans generally require 650+, and SBA 504 loans require closer to 680. SBA Microloans (up to $50,000) may accept scores as low as 500, but equipment financing is typically the faster and more accessible route at that credit level.

What is the easiest loan to get approved for with no credit?

Equipment financing and revenue-based financing are among the most accessible options when credit history is thin or nonexistent, the equipment itself serves as collateral. Vendor financing programs and microloans are also worth exploring as easy equipment financing alternatives.

Can startups get equipment financing with no credit check?

Yes. Startups can qualify through equipment leasing, vendor programs, SBA Microloans, or lenders with no minimum time-in-business requirement. A down payment of 20–50% significantly improves approval odds. See our startup equipment financing guide for a full breakdown of options built specifically for new businesses.

Ready to explore no credit check equipment financing without the guess

Founder of Nanotom Capital & Nanotom Labs