Key Takeaways

- Equipment financing rates range from 5% to 15% APR for established businesses with good credit. Medical and healthcare borrowers qualify for the lowest rates (4%–12%), while technology financing runs the highest (8%–20%).

- 82% of U.S. businesses use some form of financing when acquiring equipment, making this one of the most widely used small business financial tools in a $1.34 trillion industry.

- For 2025, Section 179 allows businesses to deduct up to $2.5 million in financed equipment placed in service during the tax year — you claim the full deduction now while spreading cash payments over up to 60 months.

- A 700+ credit score with a 20% down payment puts you in the best rate tier (5%–10% APR); scores as low as 520 can still qualify through alternative lenders, typically at 18%+ APR.

- Online lenders approve equipment financing in 24 to 48 hours; traditional banks take 2 to 4 weeks — your timeline should drive which lender type you approach first.

- On a $200,000 loan at 10% APR over 84 months, you’ll pay approximately $75,940 in total interest. Choosing a shorter term costs more per month but significantly reduces total borrowing cost.

- Most lenders finance 80%–100% of equipment cost and can roll in soft costs like delivery, installation, and training up to 25% of the total financed amount.

Buying equipment outright drains capital fast, and for most businesses, that’s a trade-off they can’t afford. Equipment financing lets you acquire what you need now and pay over time, keeping cash available for payroll, inventory, and growth. This guide covers everything: rates, lenders, bad-credit options, SBA alternatives, and the math behind real monthly payments.

What Is Equipment Financing?

Equipment financing is a type of small business loan used to purchase business-critical equipment, vehicles, machinery, or software. The equipment itself typically serves as collateral, allowing businesses to spread payments over a fixed term (usually 1 to 7 years) while preserving working capital. Once fully repaid, the business owns the equipment outright.

This isn’t a niche product. The U.S. equipment finance industry was valued at approximately $1.34 trillion in 2023, and 82% of U.S. businesses use some form of financing when acquiring equipment, according to the Equipment Leasing and Finance Association (ELFA).

Equipment financing loans range from small purchases like a $5,000 commercial oven to multi-million-dollar manufacturing lines. The structure stays largely the same regardless of size: fixed payments, a defined term, and the equipment securing the debt.

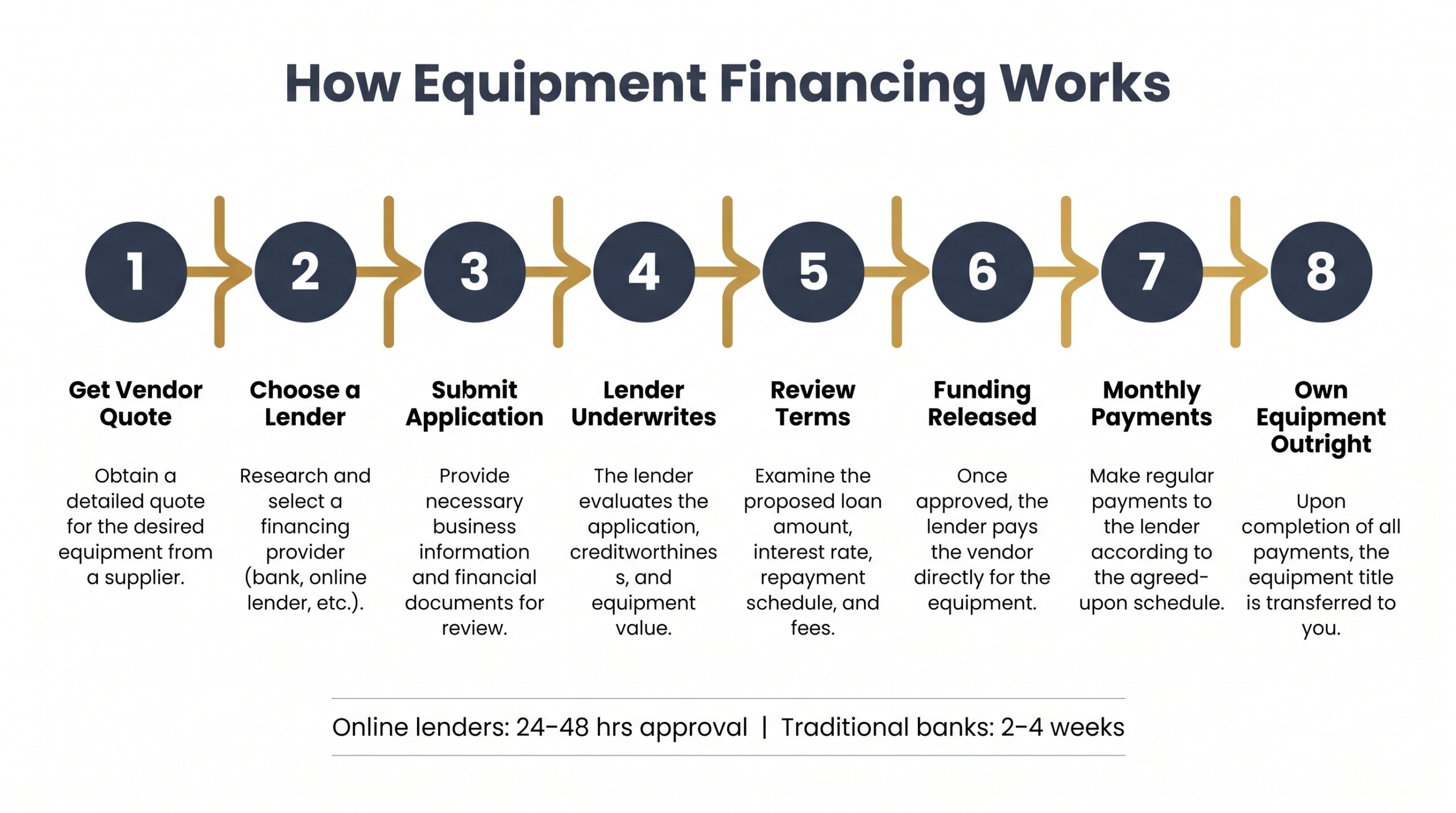

How Does Equipment Financing Work? (Step-by-Step)

The equipment financing process is straightforward, but knowing each stage helps you move faster and negotiate better terms.

- Identify the equipment and get a vendor quote. Lenders need to know exactly what they’re financing. A formal invoice or quote locks in the amount.

- Choose a lender type. Banks, alternative lenders, SBA programs, and vendor financing all offer equipment financing loans with different speeds and requirements.

- Submit your application. Expect to provide business tax returns, bank statements, a voided check, and the vendor quote.

- Lender underwrites the deal. They’ll evaluate your credit score, time in business, annual revenue, and the equipment’s resale value.

- Review and accept your terms. Rate, repayment term, and any required down payment are all negotiable to a degree.

- Funding hits. Many lenders pay the vendor directly. Others fund your account and you pay the vendor.

- Make fixed monthly payments over the agreed term.

- Own the equipment outright once the final payment clears.

Online lenders can approve equipment financing in 24 to 48 hours. Traditional banks often take two to four weeks.

Types of Equipment You Can Finance

Equipment financing covers nearly every asset a business depends on. Here’s what qualifies across the most common industries.

Heavy Machinery and Construction Equipment

Excavators, cranes, bulldozers, and forklifts are among the most frequently financed assets in the country. Ticket sizes often run $100,000 to $500,000+. See our guide to heavy equipment financing for industry-specific rates.

Commercial Vehicles and Fleets

Semi-trucks, cargo vans, trailers, and refrigerated vehicles all qualify. Fleet financing lets you add multiple units under one loan structure. Learn more in our trucking equipment financing guide.

Technology, Computers, and Software

Servers, workstations, point-of-sale systems, and even SaaS licenses can be financed. Technology depreciates fast, so shorter terms of 24 to 36 months typically make the most sense.

Medical and Dental Equipment

MRI machines, dental chairs, and diagnostic tools often cost hundreds of thousands of dollars. Specialized lenders offer programs tailored to healthcare cash flow cycles. Explore options in our medical and dental equipment financing guide.

Restaurant and Food Service Equipment

Commercial ovens, walk-in coolers, hood systems, and POS platforms all qualify for equipment financing loans. Our restaurant equipment financing guide covers lenders that specialize in food service.

Other Specialty Equipment

Agricultural equipment, salon stations, gym equipment, and printing presses all fall under commercial equipment financing. If your business depends on it, a lender will likely finance it.

One often-overlooked benefit: many lenders will roll soft costs like delivery, installation, and training into the loan, typically up to 25% of the total financed amount. And if you’re considering used or refurbished equipment, that’s covered in detail further below.

Equipment Financing vs. Equipment Leasing: What’s the Difference?

These two products get confused constantly. The core distinction is simple: equipment financing means you own the asset at the end of the term. Leasing means you return it or pay a residual to buy it.

| Factor | Equipment Financing | Equipment Leasing |

|---|---|---|

| Ownership at end of term | You own it outright | Return, renew, or buy at residual |

| Monthly payment level | Higher | Lower |

| Flexibility to upgrade | Low | High |

| Balance sheet impact | Asset and liability recorded | Varies by lease type |

| Tax treatment | Depreciation + interest deduction | Lease payments may be fully deductible |

| Best for | Long-life equipment you’ll use for years | Fast-depreciating tech or short-term needs |

Equipment financing loans make the most sense when the asset holds its value and you plan to use it long-term. Leasing wins when you need the latest technology every few years.

For a deeper breakdown, see our full equipment financing vs. leasing comparison.

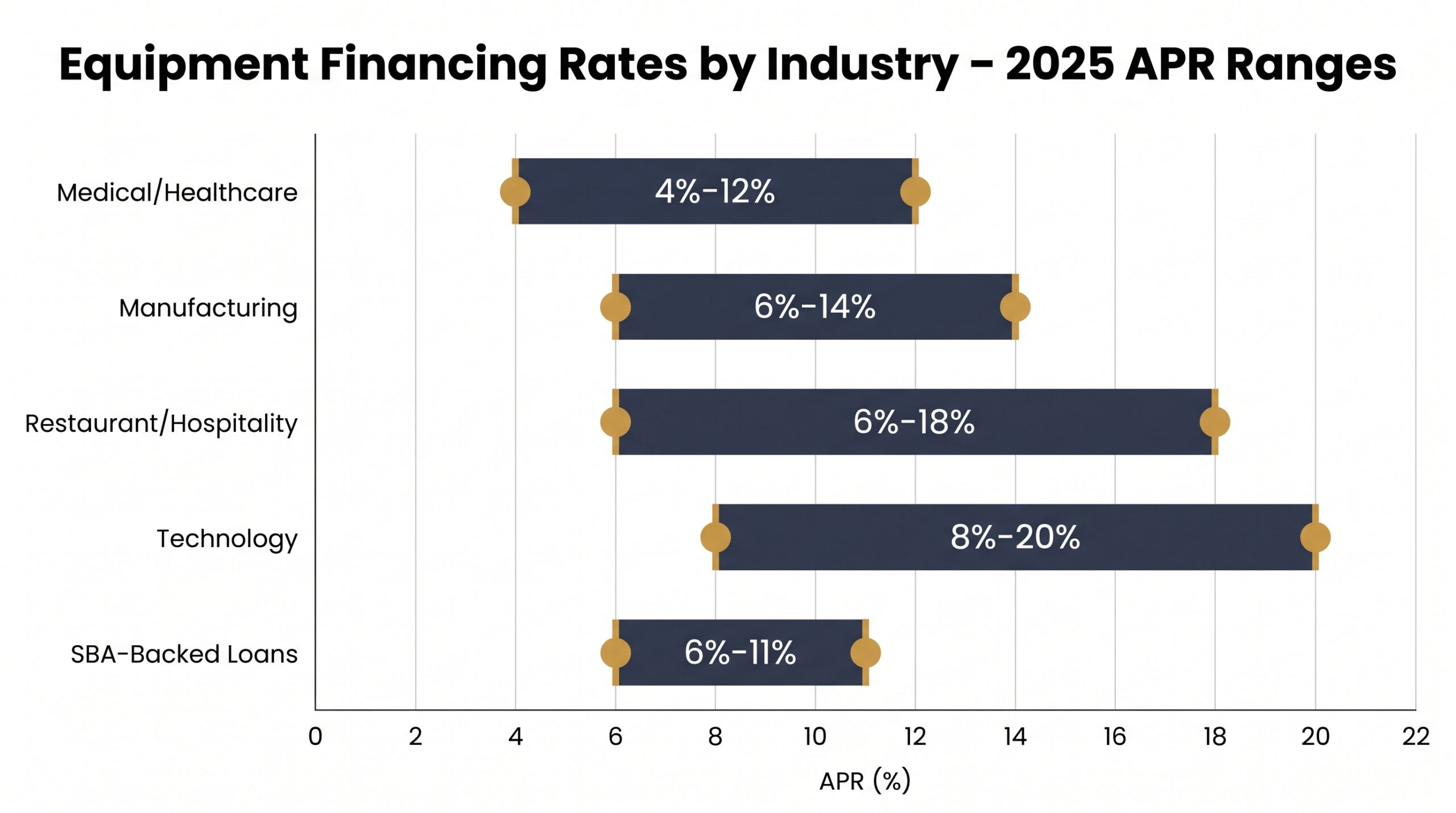

Equipment Financing Rates: What to Expect in 2025

Most equipment financing rates fall between 5% and 15% APR for established businesses with good credit. Rates vary significantly by industry, lender type, and borrower profile.

| Industry | Typical APR Range |

|---|---|

| Medical / Healthcare | 4% – 12% |

| Manufacturing | 6% – 14% |

| Restaurant / Hospitality | 6% – 18% |

| Technology | 8% – 20% |

| SBA-backed equipment loans | 6% – 11% |

Fixed vs. Variable Rate Equipment Loans

Most equipment financing loans use fixed rates, meaning your payment never changes. Some bank products offer variable rates tied to the prime rate, which introduces payment uncertainty. For most small businesses, fixed wins on budgeting predictability alone.

What Factors Affect Your Rate?

Lenders price equipment financing based on six core factors: credit score, time in business, annual revenue, equipment type and resale value, down payment size, and industry risk. Strong credit (700+) and a 20% down payment can meaningfully move your rate toward the lower end of the range.

For a full rate breakdown by lender and credit tier, see our equipment financing rates guide.

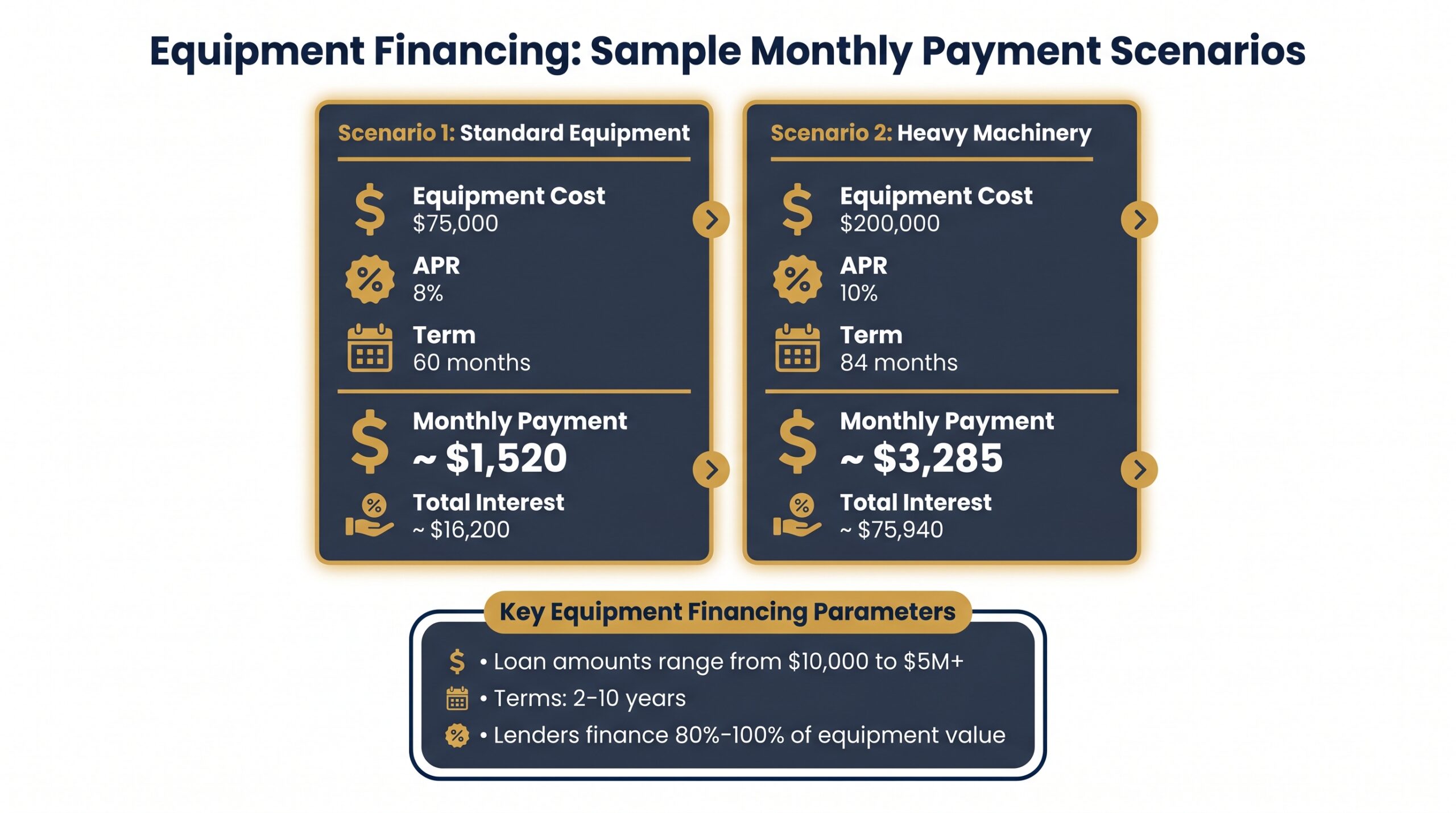

Equipment Financing Loan Amounts and Terms

Equipment financing loans typically range from $10,000 to $5 million or more. Most lenders will finance 80% to 100% of the equipment’s value, and terms generally run 2 to 7 years. Long-life assets like industrial machinery can stretch to 10-year terms.

Sample Payment Scenario: What Does Equipment Financing Actually Cost?

Here’s what real monthly payments look like at common loan sizes and rates.

| Equipment Cost | APR | Term | Monthly Payment | Total Interest Paid |

|---|---|---|---|---|

| $75,000 | 8% | 60 months | ~$1,520 | ~$16,200 |

| $200,000 | 10% | 84 months | ~$3,285 | ~$75,940 |

Longer terms lower your monthly payment but increase total interest paid. Shorter terms cost more per month but save significantly over the life of the loan.

Every deal is different. Use our equipment financing calculator to run custom payment estimates based on your actual loan amount, rate, and term.

How to Qualify for Equipment Financing

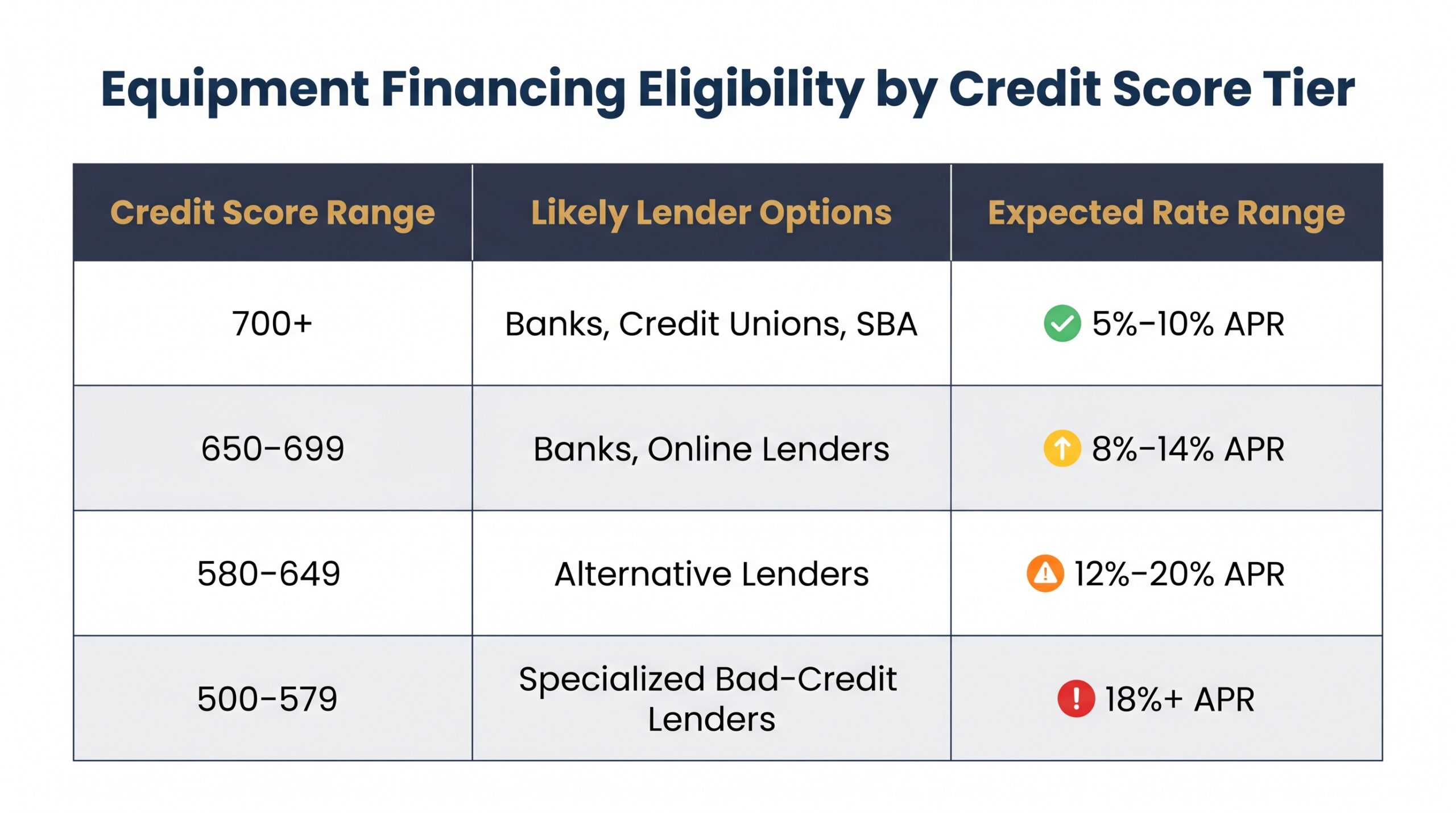

Credit Score Requirements

Traditional banks and credit unions typically require a 650 to 680+ credit score for equipment financing loans. Online and alternative lenders often approve borrowers at 520 to 600, with higher rates to match the added risk.

| Credit Score | Likely Lender Options | Expected Rate Range |

|---|---|---|

| 700+ | Banks, credit unions, SBA | 5% – 10% APR |

| 650 – 699 | Banks, online lenders | 8% – 14% APR |

| 580 – 649 | Alternative lenders | 12% – 20% APR |

| 500 – 579 | Specialized bad-credit lenders | 18%+ APR |

Time in Business

Most traditional lenders want at least 2 years of operating history. Some alternative lenders will work with businesses as young as 6 to 12 months, especially when the equipment serves as strong collateral.

Revenue Requirements

Expect most lenders to want $100,000 to $250,000 in annual revenue. Some equipment financing programs have no stated minimum, but they’ll scrutinize bank statements closely regardless.

What If You Have Bad Credit or Are a Startup?

Bad credit doesn’t automatically disqualify you. A larger down payment of 10% to 30%, additional collateral, or a personal guarantee can offset credit risk with many lenders. SBA 7(a) loans have no official credit score minimum, but most SBA lenders require 620 to 640+ in practice. SBA microloans may be accessible with lower scores.

See our guides on equipment financing with no credit check and startup equipment financing for targeted options.

Where to Get Equipment Financing: Lender Types Compared

Not all equipment financing lenders are equal. Your best option depends on your credit profile, how fast you need funding, and how much documentation you can tolerate.

Traditional Banks and Credit Unions

Banks offer the lowest rates on equipment financing loans, often 5% to 10% APR for qualified borrowers. The tradeoff is strict requirements and approval timelines that can stretch 2 to 4 weeks.

Online and Alternative Lenders

Online lenders approve equipment financing in 24 to 48 hours and accept lower credit scores. Rates run higher, typically 10% to 25% APR, but the speed and flexibility are unmatched for time-sensitive purchases.

SBA Loans (7(a) and 504)

SBA 7(a) loans go up to $5 million at 6% to 11% APR with longer repayment terms. The SBA 504 program suits long-life fixed assets, requires roughly 10% down, and works well for real-estate-adjacent equipment purchases. Both require significant documentation and patience.

Vendor and Manufacturer Financing

Buying directly from a vendor sometimes unlocks promotional rates, occasionally 0% APR for short periods. It’s convenient but can limit your negotiating leverage on equipment price.

Equipment Financing Brokers

Brokers shop your deal across multiple lenders simultaneously. They’re especially valuable for complex transactions or borrowers with credit challenges who need someone to advocate for the best terms.

See our best equipment financing companies roundup and our guide to equipment financing brokers to compare specific lenders.

Can You Finance Used or Refurbished Equipment?

Yes. Most lenders offer equipment financing for used and refurbished assets, though the terms differ from new equipment loans. Lenders evaluate remaining useful life, current condition, age, and resale value when structuring the deal.

A few practical realities to know upfront. Loan terms on used equipment are often shorter, since lenders want repayment before the asset loses significant value. Many lenders cap equipment age at 10 to 15 years old at the time of purchase. And rates may run slightly higher than comparable new equipment financing.

Three tips for financing used equipment successfully:

- Get an independent appraisal before applying so you know the asset’s true market value.

- Research resale comps for your specific make and model; lenders do the same.

- Buy from a reputable dealer when possible, since private-party purchases face more lender scrutiny.

For a full breakdown of lenders, rates, and eligibility rules, see our dedicated used equipment financing guide.

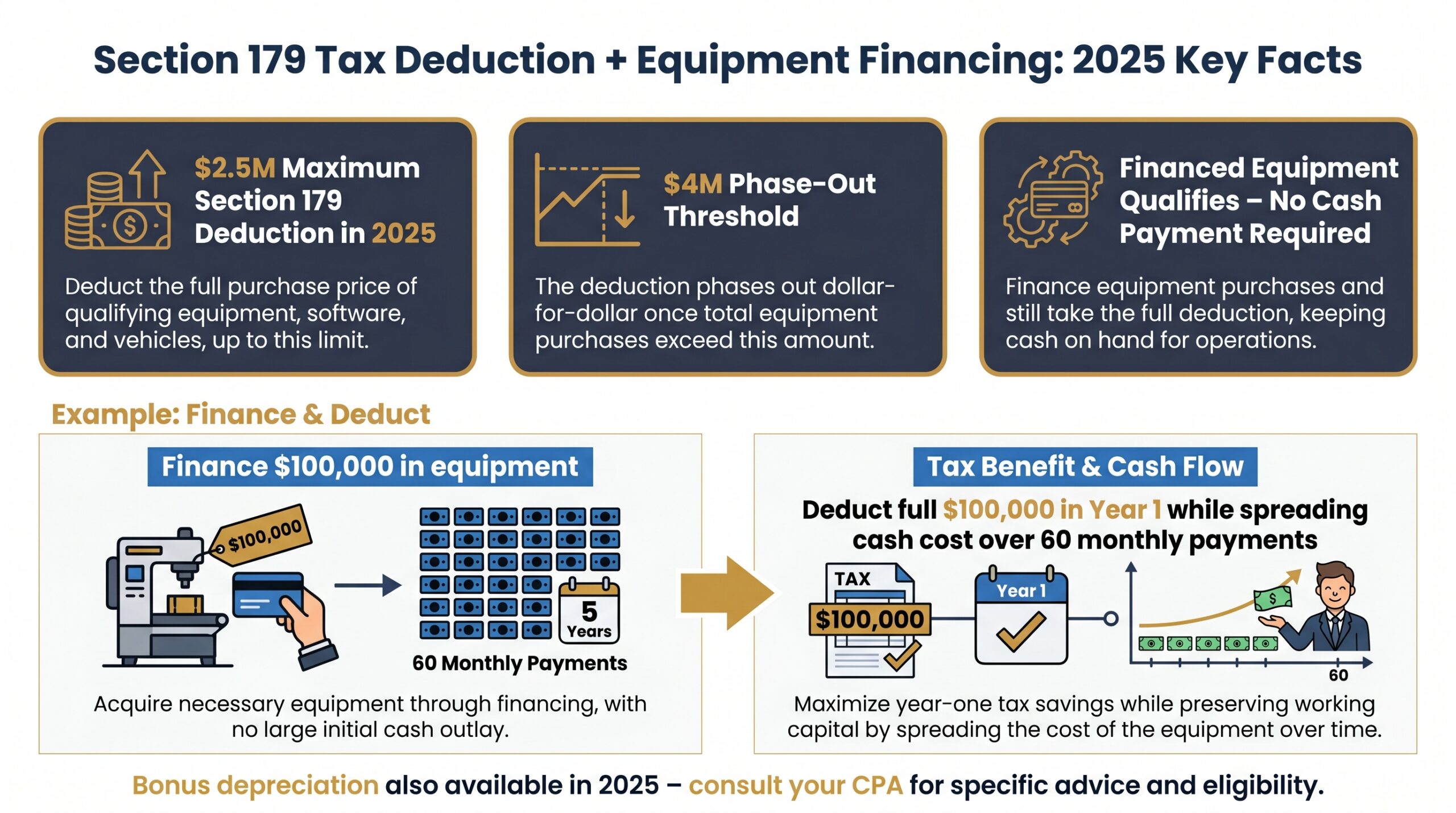

Tax Advantages of Equipment Financing (Section 179 and Bonus Depreciation)

Equipment financing unlocks one of the most valuable tax strategies available to small businesses: Section 179 expensing.

For 2025, businesses can deduct up to $2.5 million of qualifying equipment placed in service during the tax year, according to the IRS. The phase-out begins at $4 million in total equipment purchases. Here’s the part most business owners miss: you don’t have to pay cash to claim the deduction. Financed equipment qualifies for Section 179 as long as it’s placed in service within the tax year.

That means you could finance $100,000 in equipment, deduct the full amount in year one, and still spread the actual cash cost across 60 monthly payments. You get the tax benefit now while preserving working capital.

Bonus depreciation is also available in 2025, though it has been phasing down from its previous 100% level. Consult your accountant for the current rate and how it stacks with Section 179 for your specific situation.

The combination of commercial equipment financing and smart tax planning can significantly reduce the true net cost of your purchase. Talk to your CPA before year-end to make sure your equipment is placed in service in time to qualify.

How Equipment Financing Appears on Your Balance Sheet

When you take out an equipment financing loan, the asset goes on your balance sheet immediately. The equipment is recorded at its purchase price as a fixed asset, and the loan appears as a corresponding liability. Each payment reduces the liability while the asset depreciates over its useful life.

This structure builds equity over time. As the loan balance drops and the equipment retains residual value, your net asset position strengthens.

Some CFOs historically preferred operating leases to keep debt off the balance sheet. That strategy largely closed under ASC 842, the current GAAP standard, which requires both financing leases and operating leases to appear on the balance sheet as right-of-use assets and lease liabilities.

The practical takeaway: equipment financing loans and financing leases now receive similar balance sheet treatment. The decision between them should hinge on ownership preference, tax strategy, and end-of-term flexibility rather than off-balance-sheet optics.

If your company is subject to debt covenants or lender financial ratio requirements, discuss the balance sheet impact of any new equipment financing with your CFO or accountant before signing.

Benefits of Equipment Financing vs. Paying Cash

Paying cash for equipment feels safe, but it’s often the wrong financial move. Equipment financing lets you put that capital to work elsewhere while the equipment generates the revenue to cover its own payments.

Here’s why most financially sophisticated businesses choose to finance equipment even when they have the cash available:

- Preserve working capital. Cash stays liquid for payroll, inventory, opportunities, and emergencies.

- Predictable fixed payments. Monthly payments don’t fluctuate, making cash flow planning straightforward.

- Section 179 tax deductions. You can deduct the full purchase price in year one without paying cash upfront.

- Build business credit. Consistent on-time payments strengthen your credit profile for future borrowing.

- Access better equipment sooner. Don’t wait years to save up while competitors upgrade.

- Self-liquidating structure. The equipment earns revenue that offsets the monthly payment directly.

The core argument for commercial equipment financing is simple: if the equipment generates more than it costs per month, financing it is a net positive for your business.

How to Apply for Equipment Financing

The application process is straightforward. Here’s exactly what to expect from start to funded.

- Define your purchase. Know the equipment you’re buying, the vendor, and the total cost before approaching any lender.

- Check your credit and financials. Pull your personal and business credit scores. Know your annual revenue and debt obligations going in.

- Gather your documents. Most lenders want 2 years of business tax returns, 3 to 6 months of bank statements, an equipment invoice or quote, your driver’s license, and your EIN.

- Compare lenders. Don’t take the first offer. See our best equipment financing companies guide to evaluate banks, online lenders, and SBA options side by side.

- Submit your application. Online lenders often return decisions in 24 to 48 hours. Banks and SBA equipment financing loans take longer.

- Review the offer carefully. Check the APR, total repayment cost, and any prepayment penalties before signing.

- Sign and receive funds. Once you execute the equipment financing agreement, funds typically go directly to the vendor.

Equipment Financing FAQs

How hard is it to get equipment financing?

Moderate, and easier than most unsecured business loans. Because the equipment serves as collateral, lenders take on less risk. Most businesses with 1+ year in operation and a 600+ credit score can qualify for some form of equipment financing.

Who offers equipment financing?

Banks, credit unions, online lenders, SBA-approved lenders, equipment manufacturers, vendors, and equipment financing brokers all offer financing for equipment. Your best option depends on your credit profile, timeline, and deal size.

Do you need a down payment for equipment financing?

Not always. Many lenders finance 100% of the equipment cost. Expect a 10% to 20% down payment requirement if you have lower credit, are buying used equipment, or are working with a conservative bank lender.

Can you pay off equipment financing early?

Usually yes, but check for prepayment penalties first. Some lenders charge 1% to 5% of the remaining balance for early payoff. Others allow it at no cost. Confirm this before signing any equipment financing agreement.

What happens at the end of an equipment financing term?

You own the equipment outright. There’s no balloon payment, no return obligation, and no residual buyout. The loan is paid off, and the asset is yours free and clear.

Can you get an SBA loan with a 500 credit score?

The SBA has no official minimum credit score, but most SBA-approved lenders require 620 to 640 in practice. At 500, your best paths are SBA microloans or specialized bad-credit equipment lenders rather than traditional SBA 7(a) programs.

What is the minimum credit score for equipment financing?

Traditional banks typically want 650 or higher. Online and alternative lenders may approve equipment financing loans for scores as low as 520 to 600, often at higher rates with shorter terms.

Ready to move forward? Compare today’s top lenders in our best equipment financing companies guide, or use our equipment financing calculator to run your own payment scenarios before you apply.

Founder of Nanotom Capital & Nanotom Labs