Key Takeaways

- 82% of businesses that acquired equipment in 2023 used some form of financing, making equipment loans and leases the norm, not the exception.

- Alternative and fintech lenders approve startups with zero months in business and credit scores as low as 550–600, while traditional banks require 2+ years of operating history and a 680+ FICO.

- Personal credit score is the single most important approval factor at Day 1, target 650+ to qualify for better rates and avoid the 20–30% down payment lenders require from riskier applicants.

- Financed equipment qualifies for Section 179 deductions up to $2,500,000 and 100% bonus depreciation in 2025, meaning an $80,000 equipment purchase can be fully deducted in Year 1 without paying cash upfront.

- CB Insights research shows 29–38% of startups fail due to cash flow problems. Financing equipment instead of paying cash preserves the working capital runway that keeps early-stage businesses alive.

- A 20% down payment, a detailed business plan with cash flow projections, and equipment with strong resale value are the three most effective ways to compensate for missing revenue history on an application.

- Default triggers repossession, a personal guarantee, and potential legal action for any deficiency balance. Contacting your lender before missing a payment is the most effective protection available.

You need equipment to launch, but lenders want two years of financials you don’t have yet. Startup equipment financing exists specifically to solve this problem. It uses the equipment itself as collateral, so your lack of operating history doesn’t automatically disqualify you.

This guide covers every realistic path from application to funded: lender types, rate ranges, and workarounds for the barriers most new founders hit first.

What Is Startup Equipment Financing?

Startup equipment financing is a funding structure where a lender purchases or funds business equipment on your behalf, and you repay the amount over a fixed term, with the equipment itself securing the loan.

Unlike standard small business loans, equipment financing for startup businesses relies heavily on collateral value rather than revenue history. That’s what makes it one of the most accessible funding options for new companies. According to the Equipment Leasing and Finance Association, 82% of businesses that acquired equipment in 2023 used some form of financing.

- Who qualifies: Startups with 0–24 months in business, including pre-revenue companies with strong personal credit

- What’s covered: Most tangible business equipment; machinery, vehicles, medical devices, restaurant gear, technology hardware

- Funding speed: As fast as 24 hours with some lenders, typically 2–7 business days

How Startup Equipment Financing Works

The core mechanic is straightforward. A lender funds the equipment, you repay in fixed monthly installments, and the equipment secures the debt. If you default, the lender takes the equipment back.

That’s exactly why new business equipment financing is available to founders who’d never qualify for an unsecured loan. The collateral does a lot of the heavy lifting that your revenue history can’t.

Equipment Loans vs. Equipment Leasing for Startups

Loans mean you own the equipment outright once you’ve repaid. Leases keep payments lower and let you upgrade as technology changes. Neither is universally better, it depends on how fast your equipment depreciates. For a deeper breakdown, see equipment leasing vs. financing.

| Factor | Equipment Loan | Equipment Lease |

|---|---|---|

| Ownership | Yes, at term end | No (unless buyout clause) |

| Monthly Cost | Higher | Lower |

| Best For | Long-life equipment | Fast-depreciating tech |

| End-of-Term Options | Keep equipment | Return, renew, or buy |

Step-by-Step: How to Apply as a New Business

- Identify equipment needed and get a vendor quote

- Gather documents: personal credit report, EIN, business plan, bank statements

- Submit your application to a startup-friendly lender

- Receive approval. Alternative lenders can move in as little as 24 hours

- Lender pays the vendor directly; you repay the lender on a fixed schedule

Types of Equipment You Can Finance as a Startup

Most tangible business equipment qualifies, new or used. Lenders care about the collateral value, not the equipment category. Soft costs like delivery, installation, and training can sometimes be rolled into the financed amount, which reduces your upfront cash burden even further.

- Restaurant equipment financing: ovens, fryers, refrigeration, POS systems

- Medical and dental equipment financing: imaging devices, exam chairs, diagnostic tools

- Heavy construction equipment financing: excavators, cranes, skid steers

- Commercial vehicles and trucks

- Manufacturing and production machinery

- Technology, computers, and servers

- Fitness and gym equipment

- Landscaping equipment

- Food truck builds and retrofits

- Laundromat washers and dryers

- Agricultural equipment

Used equipment is fully eligible with most lenders. Many cap financed equipment at 10 to 15 years old, but a two-year-old commercial oven or a refurbished CNC machine qualifies without issue.

The Real Startup Challenge: Why New Businesses Get Rejected (And How to Overcome It)

Here’s what most equipment financing guides skip. They’re written for businesses with two years of tax returns and a healthy revenue stream. If that’s not you, here’s what you’re actually up against, and how to work around it.

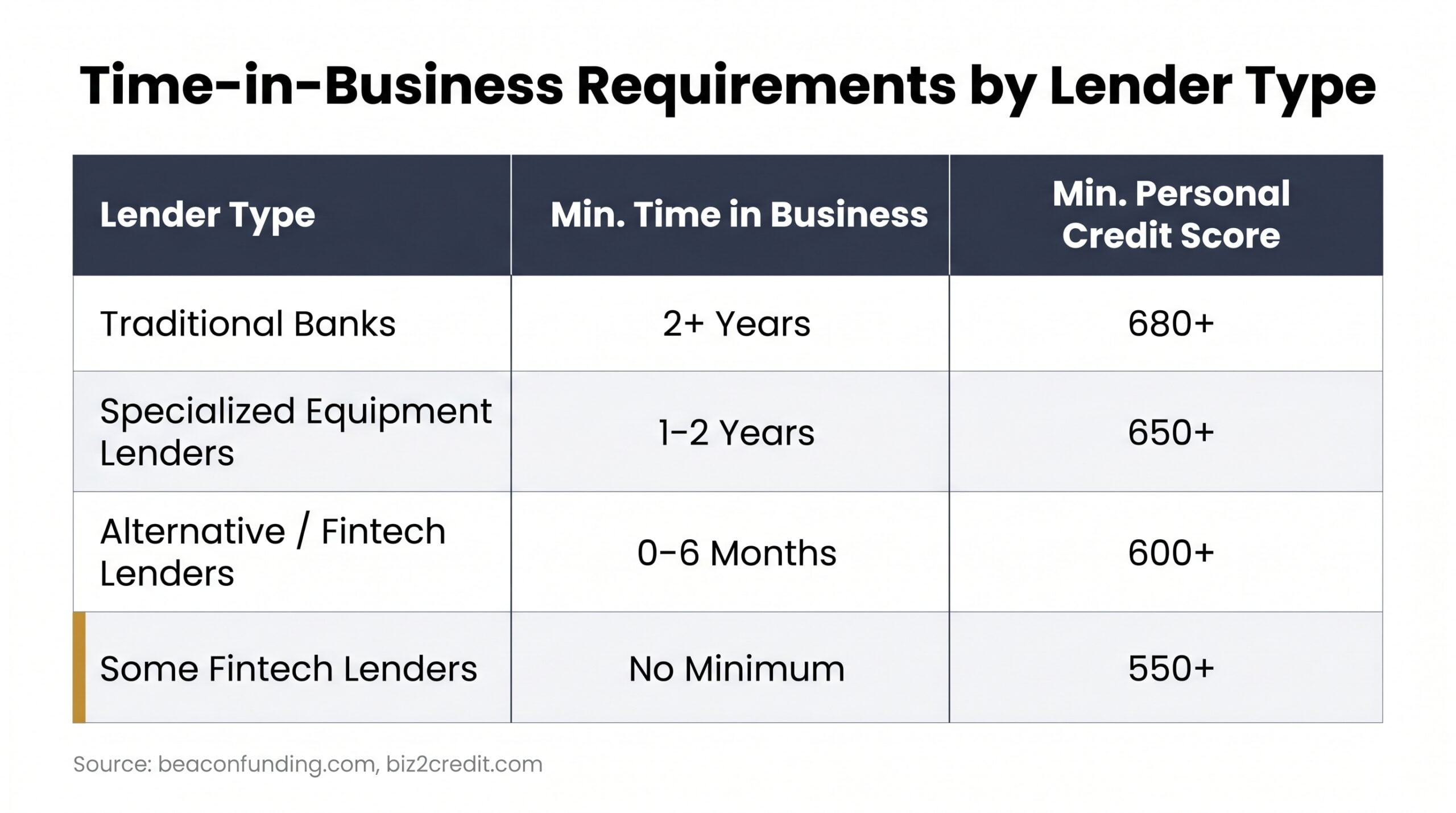

Time-in-Business Requirements by Lender Type

| Lender Type | Minimum Time in Business |

|---|---|

| Traditional banks | 2+ years |

| Specialized equipment lenders | 1–2 years |

| Alternative/fintech lenders | 0–6 months (some have no minimum) |

Personal Credit vs. Business Credit for Startups

At Day 1, your personal FICO is everything. Alternative lenders typically require a 600 minimum; traditional lenders want 650 or higher. Your business credit score is nearly irrelevant; you haven’t had time to build one yet.

Using a Co-Signer or Guarantor to Strengthen Your Application

A personal guarantee is standard in new business equipment financing. You’re promising repayment with your personal assets, full stop. A creditworthy co-signer can unlock better rates, but not every lender allows them. Ask upfront before you get too far into the process.

How a Business Plan Can Substitute for Revenue History

Some lenders will accept projected cash flow statements, industry comparables, documented owner experience, and a larger down payment in place of actual revenue history.

A 20% down payment signals commitment and materially reduces lender risk. It won’t replace two years of tax returns, but it can shift a decline into an approval.

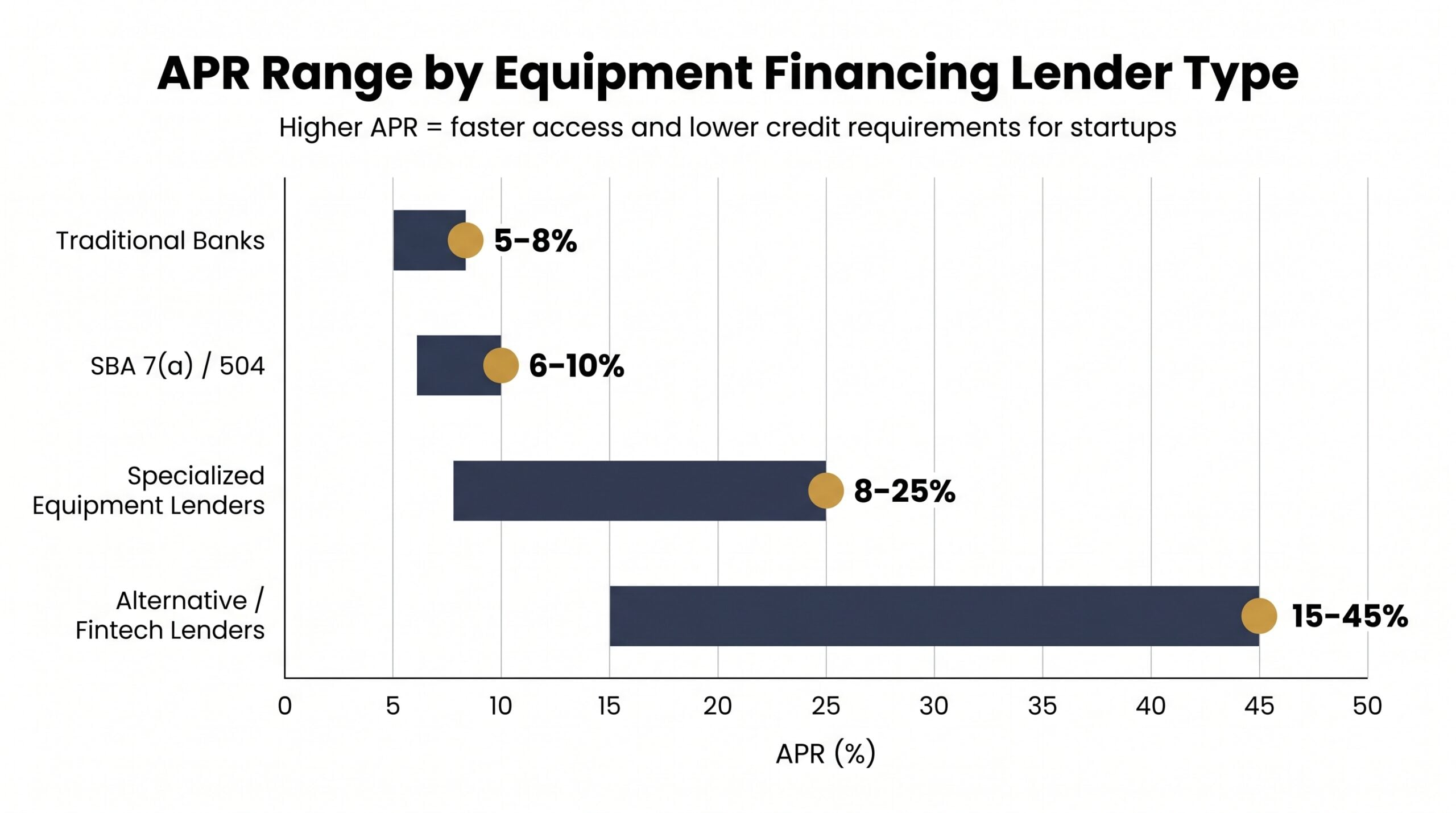

Startup Equipment Financing Options Compared

| Lender Type | Min. Time in Business | Min. Credit Score | Approx. APR Range | Speed | Best For |

|---|---|---|---|---|---|

| Alternative/Fintech | 0–6 months | 550–600+ | 15–45% | Same day to 48 hrs | Brand-new startups |

| Specialized Equipment Lenders | 6–24 months | 600+ | 8–25% | 1–3 days | Startups with some history |

| SBA 7(a)/504 | Varies | 640–680+ | 6–10% | Weeks | Lower-cost, longer timeline |

| Traditional Banks | 2+ years | 680+ | 5–8% | Weeks to months | Established businesses |

Alternative and Fintech Lenders (Best for True Startups)

These are your most realistic Day 1 options. Approval decisions lean heavily on personal credit and equipment value, not revenue. You’ll pay more in equipment financing rates, but you can actually get approved. That’s the trade-off, and for most early-stage founders it’s the right one.

Specialized Equipment Finance Companies

These lenders underwrite equipment every day and understand collateral values far better than a generalist bank ever will. See our full breakdown of the best equipment financing companies to compare specific lenders side by side.

SBA 7(a) and SBA 504 Loans for Startup Equipment Needs

The SBA 7(a) is more startup-friendly, as it can cover equipment purchase and installation costs. The 504 is better suited for large, long-lived assets with a 10-plus year useful life.

Both programs require demonstrated repayment ability, per SBA.gov guidelines. If your timeline is flexible and your paperwork is solid, the rates make it worth the wait.

Traditional Bank Equipment Loans

Cheapest rates. Strictest requirements. If you’re under two years old, banks will almost certainly decline you. File this option away for year three and move on.

Startup Equipment Financing Qualification Requirements

Here’s what lenders actually look at when a startup applies. Meet these benchmarks and your approval odds improve significantly. Fall short on one, and you’ll need to compensate somewhere else.

Minimum Credit Score Requirements

Most alternative lenders require a 600 personal FICO minimum. A 650 puts you in a meaningfully better position for rates and terms. Some specialty lenders go as low as 550, but expect higher rates and larger down payments in exchange.

If your credit file is thin, explore equipment financing with no credit check options before assuming you’re locked out entirely.

Down Payment Expectations for New Businesses

Plan for 10–20% down with mid-tier credit. Drop below 600 or apply in your first few months of operation, and lenders typically want 20–30%. A larger down payment signals commitment and directly reduces their collateral risk; it’s one of the clearest levers you can pull.

Revenue and Financial Documentation

If you’re generating revenue, bring 3–6 months of bank statements. Pre-revenue? You’ll need a detailed business plan with cash flow projections, proof of owner industry experience, and your EIN and formation documents.

Some lenders skip revenue requirements entirely on smaller deals where the equipment’s collateral value is strong relative to the loan amount. Don’t assume the worst before you ask.

Real-World Startup Use Cases by Industry

Restaurant Startup

A founder opens a fast-casual concept in month two of operation. They need commercial ovens, walk-in refrigeration, and a POS system, for a total of $75,000. With a 680 personal FICO and 15% down, they qualify through an alternative lender and have equipment delivered within a week of applying.

Medical Practice Startup

A physician leaving a hospital system to open a private practice needs diagnostic imaging equipment worth $120,000. A specialized healthcare equipment lender underwrites heavily on the equipment’s resale value and the physician’s professional credentials, offsetting the zero-revenue history almost entirely.

Construction Startup

A new contractor needs an excavator to bid commercial jobs. An equipment-specific lender finances the asset with the machine itself as primary collateral. No two years of tax returns required. For more on this path, see trucking equipment financing strategies that apply across heavy equipment categories.

Food Truck Operator

A first-time operator finances a full truck build-out and commercial kitchen equipment through a dedicated food truck equipment financing program. Many of these programs are structured for pre-revenue applicants and treat the truck itself as sufficient collateral.

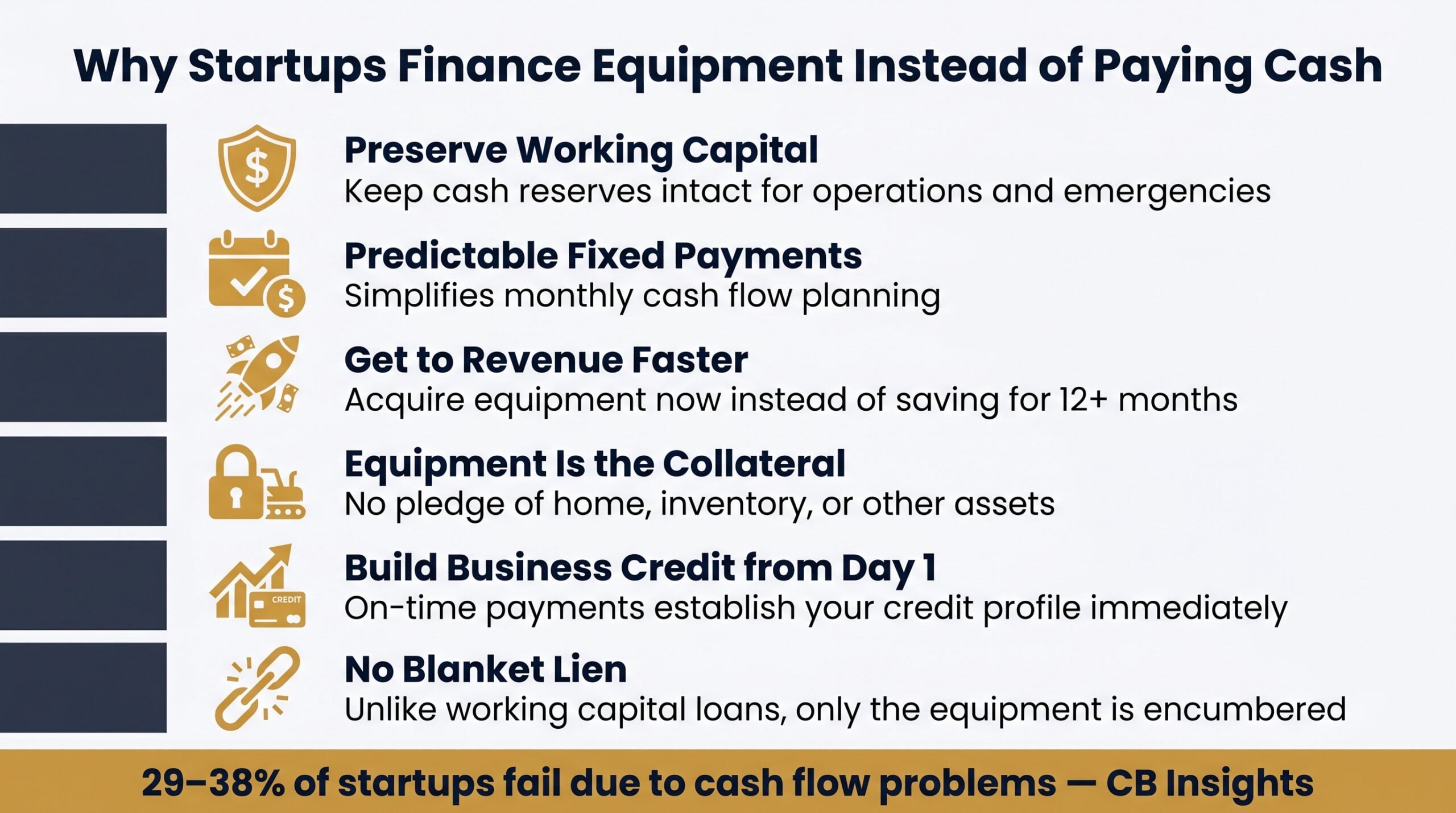

Benefits of Financing Equipment Instead of Paying Cash as a Startup

CB Insights research shows 29–38% of startups fail due to cash flow problems. Draining your reserves on equipment purchases is one of the fastest ways to join that statistic.

Startup equipment financing keeps that cash in your account where it belongs, and it does a few other things worth knowing about.

- Preserve working capital. Cash is your survival buffer in year one. Equipment financing for your startup lets you acquire what you need without wiping out your runway.

- Predictable fixed payments. Monthly installments make cash flow planning straightforward, with no surprise costs.

- Get to revenue faster. Financing equipment now beats saving for 12 months and missing the market window entirely.

- Equipment is the collateral. You’re not pledging your home, inventory, or other business assets to secure the loan.

- Build business credit immediately. On-time payments start establishing your business credit profile from Day 1.

- No blanket lien. Unlike most working capital loans, equipment financing for new businesses typically doesn’t encumber all your business assets.

Tax Advantages: Section 179 and Bonus Depreciation for Startup Equipment

Most first-time founders miss this one. You don’t need to pay cash to claim the tax deduction; financed equipment qualifies for Section 179 and bonus depreciation just the same.

- Section 179 (2025): Deduct up to $2,500,000 in equipment purchases in the year placed in service. According to Section179.org, the deduction phases out above $4,000,000 in total purchases, well beyond startup scale.

- Bonus Depreciation (2025): 100% first-year depreciation on qualifying property placed in service after January 19, 2025, per IRS guidance.

The practical impact is real. A startup finances $80,000 in equipment, makes manageable monthly payments, and still deducts the full $80,000 in Year 1. That’s a material reduction in tax liability during the year you can least afford a large tax bill.

For a deeper look at how the loan structures behind these deductions actually work, see our equipment financing explained guide. Always consult a tax professional before applying these deductions to your specific situation.

What Happens If Your Startup Defaults on Equipment Financing?

The honest answer is that most guides won’t walk you through this. Default consequences are real, and understanding them upfront makes you a better borrower, not a scared one.

Here’s what the default sequence typically looks like:

- Repossession. The lender reclaims the equipment; it’s their collateral, and they move quickly.

- Deficiency balance. If the equipment sells at auction for less than you owe, you’re responsible for the gap.

- Personal guarantee triggered. Your personal assets, savings, home equity, and other property become fair game.

- Credit damage. Both your personal and business credit scores take significant hits.

- Legal action. Lenders can pursue judgments against you personally for unpaid deficiency balances.

The single best protection is communication. If cash flow tightens, call your lender before you miss a payment. Many offer forbearance or loan restructuring for borrowers who reach out early; they’d rather work with you than repossess equipment and sell it at a loss.

Before you sign anything, read your equipment financing agreement carefully, especially the personal guarantee clause and default cure periods. Match your loan term to the equipment’s actual revenue-generating life. A five-year loan on equipment that wears out in three is a structural problem from Day 1.

Tips to Improve Your Chances of Approval as a Startup

These steps directly address the gaps that get startups declined. Work through as many as you can before submitting an application.

- Protect your personal credit score. Target 650 minimum before applying. Pay down revolving balances and dispute any errors on your report now.

- Prepare a detailed business plan. Include realistic revenue projections and demonstrate industry experience. Lenders want to see a credible path to repayment.

- Offer a larger down payment. Coming in at 15–20% signals commitment and meaningfully reduces the lender’s risk exposure.

- Apply with a co-signer. A guarantor with strong credit can be the difference between approval and decline when your own history is thin.

- Choose equipment with strong resale value. Lenders get more comfortable when the collateral holds its value, think name-brand, widely-used machinery over niche assets.

- Work with specialists, not generalists. Equipment financing brokers and specialized lenders understand startup risk far better than a community bank loan officer.

- Lease first, refinance later. Build a payment track record through a lease, then use that history to qualify for better loan terms.

- Start small. Finance a $15,000 piece of equipment, pay it cleanly, and you’ve got business credit history for the next application.

Use Our Equipment Financing Calculator to Estimate Your Payments

Before you apply, run the numbers. Knowing your estimated monthly payment tells you whether the financing fits your projected cash flow, or whether you need to adjust the loan amount, term, or down payment first.

Two quick examples at common startup rate ranges:

- $50,000 financed at 12% APR over 60 months: approximately $1,112/month

- $25,000 financed at 15% APR over 48 months: approximately $695/month

Those numbers look very different against a startup generating $8,000 per month in revenue versus one that’s still pre-revenue. Running scenarios before you apply helps you avoid overextending in year one, when cash flow is tightest.

Use our equipment financing calculator to plug in your actual loan amount, estimated rate, and preferred term. It takes 30 seconds and gives you a clear baseline before any lender conversation.

Frequently Asked Questions About Startup Equipment Financing

Can a brand-new business with no revenue get equipment financing?

Yes. Some alternative lenders and fintech platforms offer equipment financing for startup businesses with no minimum time in business or revenue requirement. Strong personal credit and high-value collateral are typically the deciding factors.

What credit score do I need for startup equipment financing?

Most alternative lenders require a minimum personal credit score of 600, with 650+ preferred for better rates. Some specialty lenders approve applicants at 550+ with a larger down payment.

How much can a startup borrow for equipment?

Loan amounts range from a few thousand dollars to $5 million or more, depending on the lender. Startups typically start smaller and scale borrowing as they build credit history.

Is startup equipment financing available for used equipment?

Yes. Most programs cover both new and used equipment. Lenders will scrutinize the age and resale value of used assets more carefully, but financing is available.

How fast can a startup get approved for equipment financing?

Alternative lenders can approve new business equipment financing in as little as 24–48 hours. SBA loans move considerably slower, often taking several weeks to months.

Do I need a down payment for startup equipment financing?

Not always. Some lenders offer 100% financing with no down payment, while higher-risk startup applicants may be required to put down 10–30% upfront.

Can I finance equipment if my startup has bad credit?

Options exist. Specialty lenders and programs built around collateral value rather than credit scores can work for challenged-credit startups, though rates will be higher. See our guide on equipment financing with no credit check for programs designed specifically for this situation.

Startup equipment financing is more accessible than most founders realize. Whether you opened last month or last week, lenders exist who understand your stage and will work with what you have. Know your numbers, protect your personal credit, choose the right lender type for your situation, and get your equipment working for you now, rather than waiting until conditions are perfect. They rarely will be.

Founder of Nanotom Capital & Nanotom Labs