Key Takeaways

- Leasing means paying to use equipment the lender owns; financing means borrowing to own it outright from day one, and this single distinction affects your taxes, balance sheet, and cash flow simultaneously.

- Monthly lease payments run 20–30% lower than loan payments on the same asset, but total cost over the term is higher. A $75,000 piece of equipment costs ~$70,830 net after financing vs. up to $108,000 through leasing.

- Section 179 lets you deduct up to $2,500,000 in equipment purchases in the year placed in service (2025), a first-year tax advantage that leasing cannot match.

- The 90% rule determines lease classification under ASC 842. If the present value of payments hits 90% or more of fair market value, the lease is treated as a finance lease with full balance sheet impact, eliminating the “off-balance-sheet” benefit most businesses expect.

- Leasing wins for fast-obsoleting equipment (IT hardware, diagnostic devices) and cash-constrained businesses; financing wins for assets with 10+ year lifespans (construction, agriculture) and profitable businesses with high tax liability.

- Equipment financing rates range from 6–20% depending on credit profile, with most lenders requiring a 10–20% down payment. Strong credit (680+) typically secures the 6–9% range.

- According to the Equipment Leasing & Finance Foundation, 82% of U.S. businesses use some form of equipment financing, in an industry worth $1.34 trillion, the structure you choose directly impacts your debt-to-equity ratio and future borrowing capacity.

Choosing the wrong way to acquire equipment can cost your business tens of thousands of dollars over just a few years. Understanding equipment leasing vs financing upfront means you stop overpaying and start making decisions that actually fit your cash flow.

This guide covers everything from balance sheet treatment to tax deductions, with real numbers attached.

Equipment Leasing vs. Financing: What’s the Core Difference?

The short answer: leasing means you pay to use equipment without owning it; financing means you take out a loan to purchase equipment and own it outright once the loan is paid off.

With equipment leasing, a lender buys the asset and rents it to you for a fixed term. You get full use of the equipment, but title stays with the lessor unless you exercise a buyout option at the end.

With equipment financing, you borrow money to buy the equipment directly. You own it from day one, it sits on your balance sheet, and you build equity as you pay down the loan.

This distinction matters at serious scale. The Equipment Leasing & Finance Foundation reports the U.S. equipment finance industry is worth $1.34 trillion, and 82% of businesses use some form of financing to acquire equipment. The equipment leasing vs financing decision affects your taxes, your credit, and your balance sheet, all at once.

Here’s exactly how each works, and which makes more financial sense for your situation.

How Equipment Leasing Works

You find the equipment you need, a leasing company buys it, and you pay them monthly to use it. No large down payment. No ownership transfer. Just access to the asset for a fixed term, typically 24 to 72 months.

Monthly payments run lower than financing because you’re only paying for the portion of the equipment’s value you consume, not the whole thing. A $50,000 piece of equipment leased over 60 months at a lease factor of 0.02 costs $1,000/month, often 20–30% less than a loan payment on the same asset.

Operating Lease

This is a true rental. You use the equipment, return it at term end, and the lessor absorbs the depreciation risk.

Under ASC 842, operating leases now appear on your balance sheet as a right-of-use asset and liability. They’re still treated differently than owned assets for accounting purposes, but don’t assume they’re invisible to lenders.

Finance (Capital) Lease

A finance lease behaves like ownership. You carry the asset and liability on your balance sheet, you handle depreciation, and you typically end up owning the equipment via a $1 buyout. When comparing equipment leasing vs financing, a finance lease sits closest to a loan in terms of accounting treatment.

What Happens at the End of the Lease Term?

You’ve got four options: return the equipment, purchase it at fair market value or a pre-agreed residual price, renew the lease, or upgrade to newer equipment.

Watch the early termination clauses carefully. Breaking a lease mid-term often triggers penalties equal to several remaining monthly payments; it’s one of the most common surprises businesses run into.

How Equipment Financing (Loans) Works

A lender gives you a lump sum to purchase the equipment, and the equipment itself serves as collateral. You own the asset from day one. If you default, the lender repossesses it, straightforward secured lending.

Typical terms run 2–7 years. Interest rates range from roughly 6% to 20% depending on your credit profile, time in business, and the asset type. Most lenders require a 10–20% down payment upfront, which is the biggest cash-flow difference when weighing equipment leasing vs financing.

The owned equipment sits on your balance sheet as a depreciating asset, offset by the loan liability. As you pay down the loan, you build equity in a tangible asset.

The tax upside is significant. According to section179.org, in 2025 the Section 179 deduction lets you write off up to $2,500,000 in qualifying equipment purchases in the year you buy, with the deduction phasing out above $4,000,000 in total purchases. That’s an immediate tax hit most leases can’t match.

Check out our guide on equipment financing rates for a full breakdown of what lenders are charging right now.

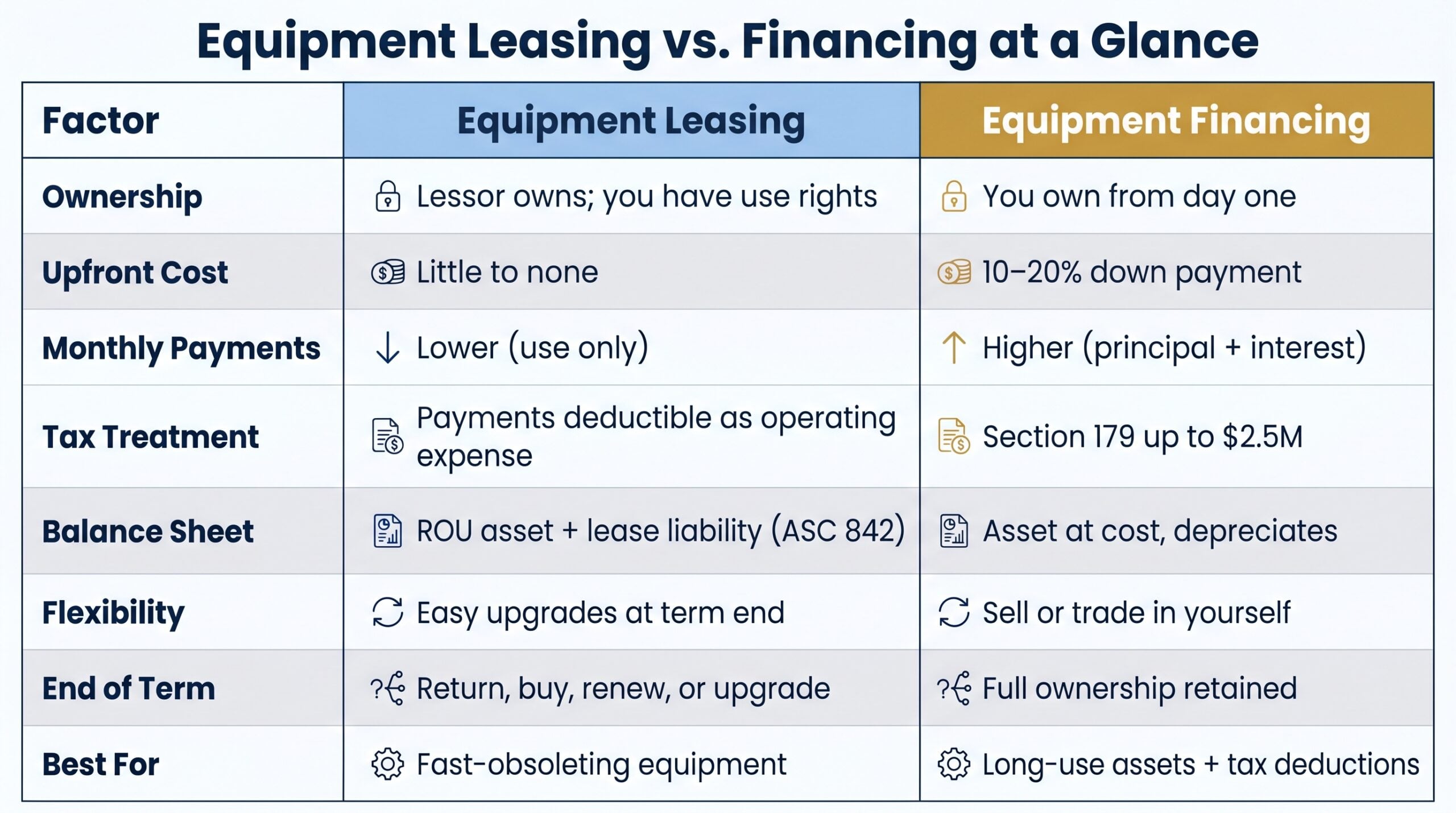

Equipment Leasing vs. Financing: Side-by-Side Comparison

Eight factors that actually move the needle, here’s the equipment leasing vs financing breakdown at a glance.

| Factor | Equipment Leasing | Equipment Financing (Loan) |

|---|---|---|

| Ownership | Lessor owns; you have use rights | You own from day one |

| Upfront Cost | Little to none; first/last payment only | 10–20% down payment typically required |

| Monthly Payments | Lower (paying for use, not full value) | Higher (repaying principal + interest) |

| Tax Treatment | Lease payments fully deductible as operating expense | Section 179 up to $2.5M; bonus depreciation available |

| Balance Sheet (ASC 842) | Operating: ROU asset + lease liability; Finance: asset + amortization + interest | Asset recorded at cost; depreciates over useful life |

| Flexibility / Upgrades | Easy to upgrade at term end | You own it. Sell or trade in yourself |

| End-of-Term Options | Return, buy, renew, or upgrade | Full ownership; no end-of-term decision needed |

| Credit / Debt Impact | Lease liability appears on balance sheet under ASC 842 | Loan increases debt-to-equity ratio directly |

| Best For | Tech-heavy or fast-depreciating equipment; cash-flow-sensitive businesses | Long-use assets; businesses maximizing tax deductions |

Pros and Cons of Equipment Leasing

Leasing looks attractive on paper: lower payments, no big down payment, easy upgrades. But the full picture of equipment leasing vs financing includes some real drawbacks worth knowing before you sign.

Advantages of Leasing

- Little to no upfront cost; preserves working capital

- Lower monthly payments than a loan on the same equipment

- Easy to upgrade at term end; ideal for technology or fast-depreciating assets

- Lease payments are typically fully deductible as operating expenses

- Predictable fixed payments simplify cash flow planning

- Lessor absorbs obsolescence risk on operating leases

Disadvantages of Leasing Equipment

- Higher total cost over the full term compared to buying outright

- You build zero equity; no resale or salvage value

- Payments continue even if the equipment sits idle

- Early termination penalties can be steep

- Usage restrictions and modification limits are common

- Under ASC 842, operating leases still create a lease liability on your balance sheet; the “off-balance-sheet” benefit largely disappeared after 2019

Pros and Cons of Equipment Financing

Financing wins on ownership and tax benefits. It’s not the right call for every situation, but when the numbers line up, it beats leasing on total cost and long-term flexibility.

Advantages of Financing

- Full ownership from day one; you build equity and capture resale value

- Section 179 lets you deduct up to $2,500,000 in the purchase year, a massive first-year tax advantage

- No usage restrictions or modification limits

- No end-of-term decisions or surprise buyout negotiations

- Most loans have no prepayment penalty; pay it off early and save on interest

- Depreciation on your books can offset taxable income year over year

Disadvantages of Financing

- Higher monthly payments than a comparable lease

- 10–20% down payment required; real cash out the door upfront

- You absorb all depreciation and obsolescence risk

- Upgrading means selling or trading in; more friction than a lease return

- The loan increases your debt load and can affect your debt-to-income ratio

For a deeper look at how lenders evaluate your application, see our guide on how equipment financing works.

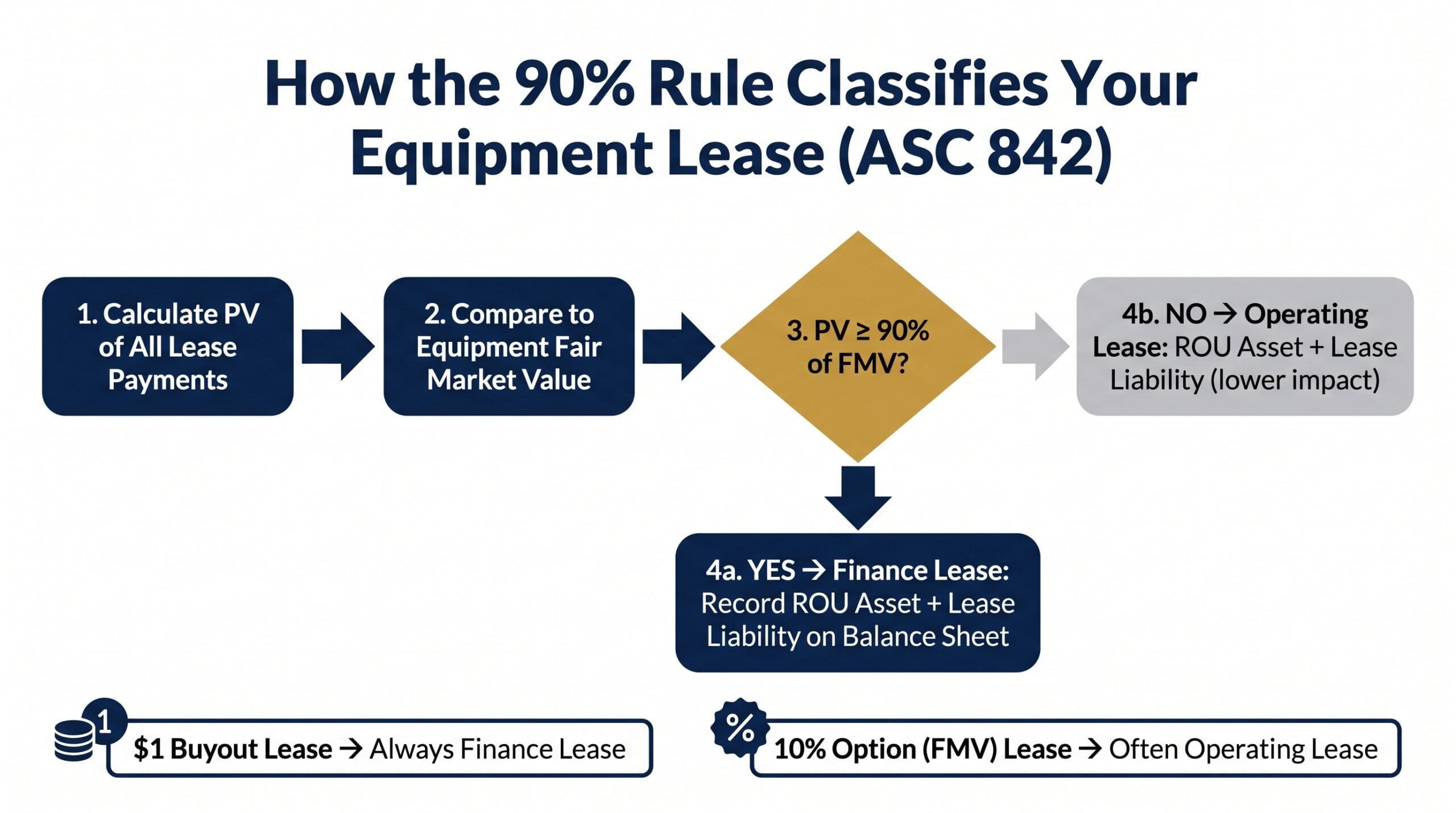

The 90% Rule in Equipment Leasing, Explained

Here’s what most guides skip over: the 90% rule doesn’t just affect your accounting, it can quietly eliminate the balance sheet benefit you thought you were getting from leasing in the first place.

The plain-English version: if the present value of all your lease payments adds up to 90% or more of the equipment’s fair market value, accounting standards treat the arrangement as ownership in disguise. Under ASC 842, that triggers finance lease treatment, meaning you record both a right-of-use asset and a lease liability, and your expenses split between amortization and interest, just like a loan.

Two lease structures commonly trigger this threshold:

- $1 buyout lease: You pay $1 at term end to own the equipment. Payments are higher monthly, but you’re clearly buying, classified as a finance lease every time.

- 10% option lease (FMV lease): You purchase at fair market value at term end. Lower monthly payments, more flexibility, and often stays closer to operating lease treatment.

Why does this matter in the equipment leasing vs financing conversation? Many business owners choose leasing expecting cleaner financials, then discover their lease still shows up as a liability. Knowing which side of the 90% threshold you’re on before signing protects your balance sheet strategy.

Tax Implications: Leasing vs. Financing Equipment

Tax treatment is where equipment leasing vs financing gets really interesting, and where the right choice can save you tens of thousands of dollars.

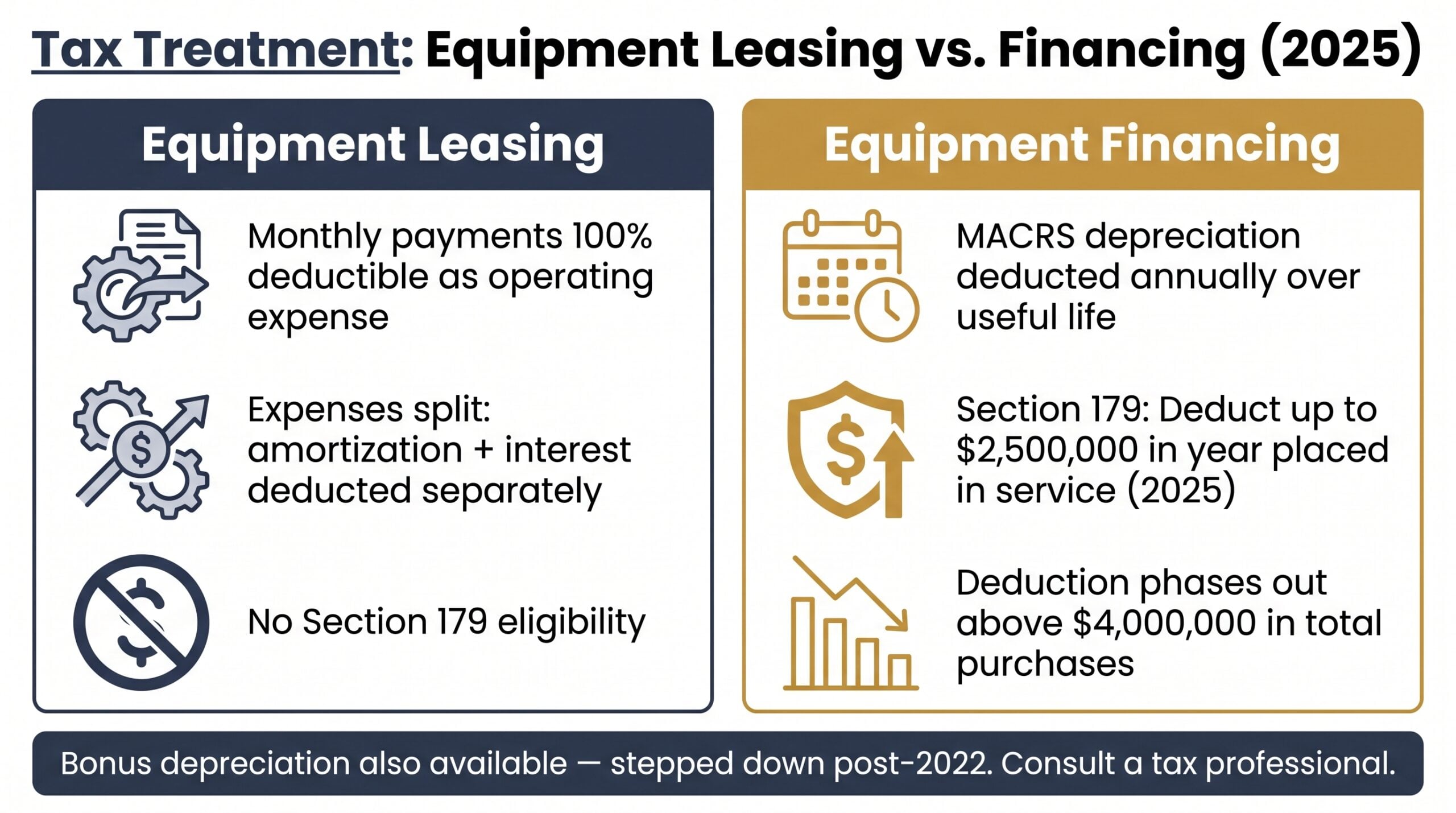

Tax Treatment for Equipment Leases

With an operating lease, your monthly payments are fully deductible as a business operating expense. Simple, predictable, and spread evenly across the lease term.

A finance lease works differently; you deduct amortization and interest separately, mirroring how a loan is treated on your taxes.

Tax Treatment for Equipment Financing (Loans)

When you finance and own the equipment, it depreciates over its useful life under MACRS. That depreciation is deductible annually, and you also deduct the interest portion of each loan payment. Slower than leasing’s clean operating expense deduction, but the Section 179 option changes the math entirely.

Section 179 Deduction: The Financing Tax Advantage

In 2025, according to the IRS, Section 179 lets you deduct the full purchase price of qualifying equipment (up to $2,500,000) in the year it’s placed in service. The deduction phases out dollar-for-dollar above $4,000,000 in total purchases. Bonus depreciation is also available, though it’s been stepping down since 2022.

For a profitable business, writing off $150,000 of equipment in year one instead of spreading it over seven years is a significant advantage in the leasing vs financing equipment decision. Always confirm your specific situation with a tax professional before structuring a deal around deductions.

Learn how loan structures affect your deductions in our guide to equipment financing agreements.

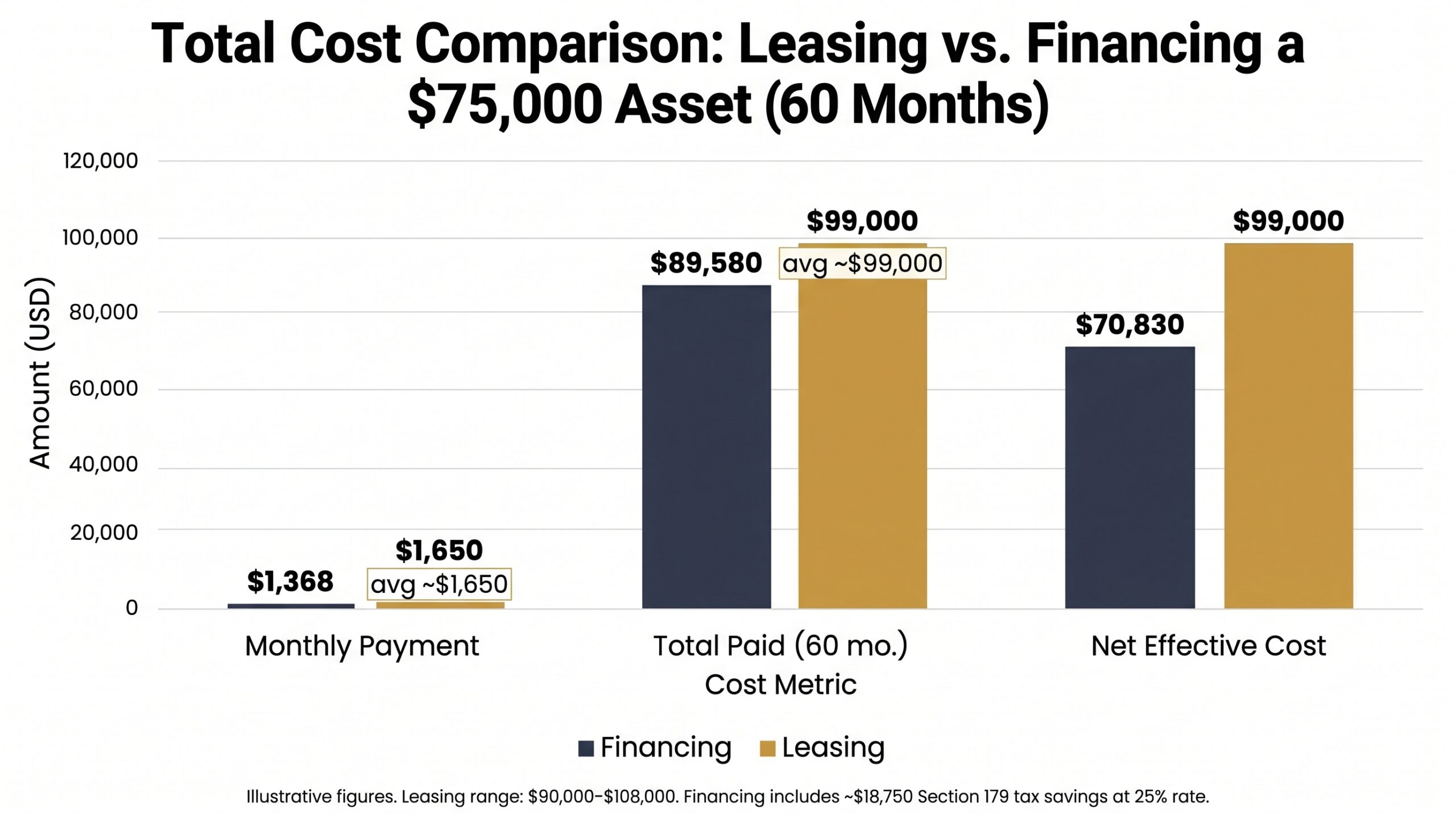

Real-World Cost Comparison: Lease vs. Finance on a $75,000 Piece of Equipment

Numbers make the equipment leasing vs financing decision concrete. Here’s how the same $75,000 piece of equipment plays out under each structure.

| Factor | Equipment Financing (Loan) | Equipment Leasing |

|---|---|---|

| Equipment Cost | $75,000 | $75,000 |

| Down Payment | $7,500 (10%) | $0 |

| Monthly Payment | ~$1,368/mo (8%, 60 months) | ~$1,500–$1,800/mo |

| Total Paid (60 months) | ~$89,580 | ~$90,000–$108,000 |

| Section 179 Tax Savings | ~$18,750 (25% tax rate on $75,000) | $0 (payments deducted annually instead) |

| Net Effective Cost | ~$70,830 | ~$90,000–$108,000 + possible buyout |

| Ownership at Term End | Yes, full equity | No, FMV buyout option only |

In this scenario, equipment financing and leasing costs are closer than most people expect on monthly payments. But financing pulls ahead significantly once Section 179 enters the picture. The lease preserves cash upfront but costs more in total, and leaves you with nothing at the end.

Numbers are illustrative and vary based on lender, credit profile, and equipment type. Use our equipment financing calculator to run your own numbers.

Types of Equipment Leases Explained

Not all leases work the same way, and the differences matter more than most people realize when you’re comparing equipment leasing vs financing on a specific deal.

Operating Lease

The closest thing to a true rental. You use the equipment, make monthly payments, and return it at term end. Lower payments, no ownership, and under ASC 842, it still creates an ROU asset and lease liability on your balance sheet.

Finance (Capital) Lease

Structured to transfer ownership risks and rewards to you. Accounting treats it like a purchase; you record an asset and a liability, and expenses split between amortization and interest. Triggers when the 90% rule or other ASC 842 criteria are met.

$1 Buyout Lease

You pay $1 at term end and own the equipment outright. Monthly payments are higher to compensate. In the equipment leasing and financing spectrum, this sits closest to a traditional loan, and it’s always classified as a finance lease.

10% Option (FMV) Lease

Purchase the equipment at term end for 10% of its original value. Lower monthly payments than a $1 buyout, more flexibility than an operating lease. A solid middle ground in the leasing vs financing equipment decision.

TRAC Lease (for Transportation Equipment)

Terminal Rental Adjustment Clause leases are built for fleets, trucks, and vehicles. The residual value is adjustable at term end, if the equipment sells for more than projected, you get a credit; less, and you pay the difference. Common in trucking and logistics. See our guide on trucking and fleet equipment financing for fleet-specific details.

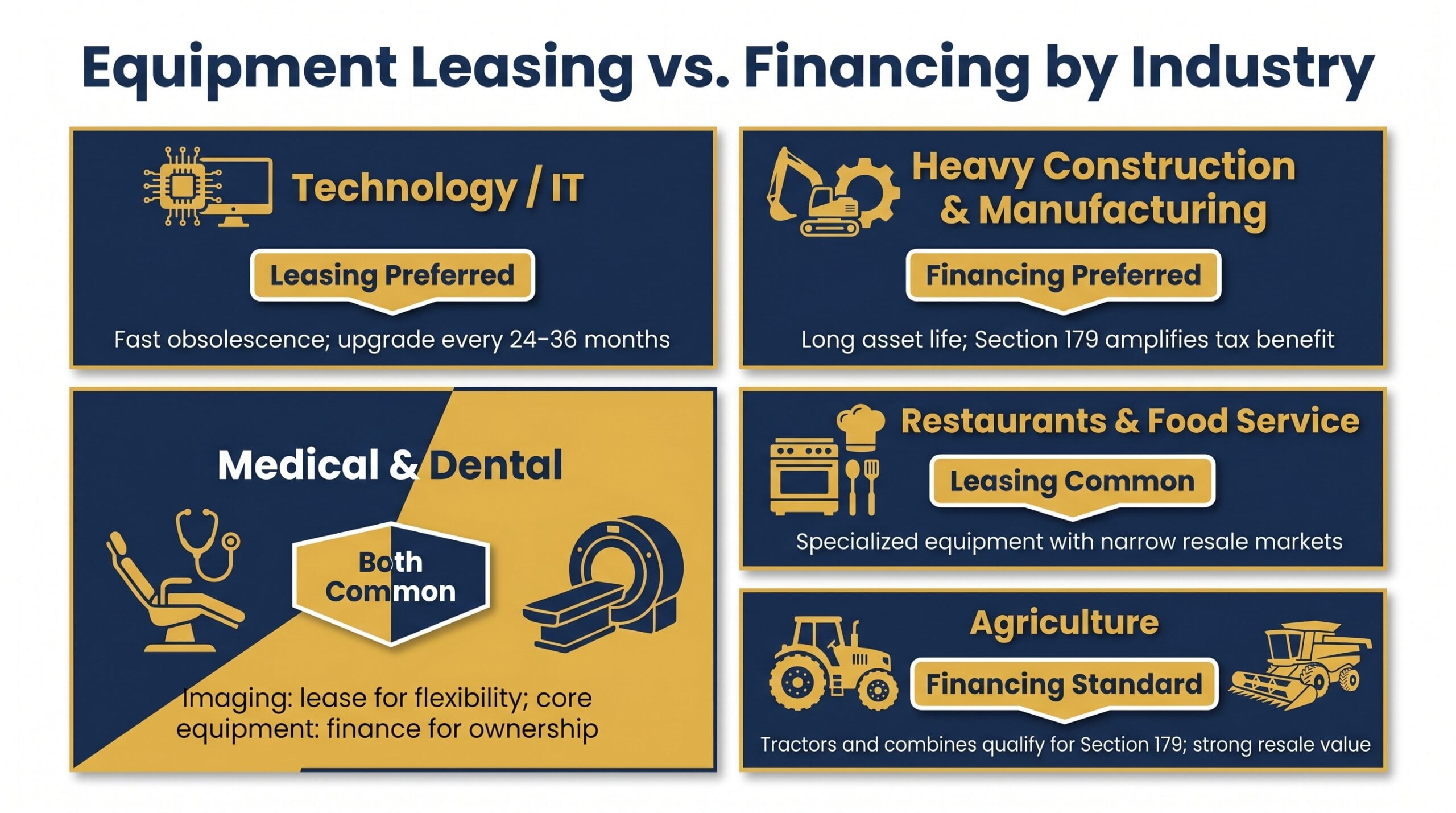

Which Industries Use Equipment Leasing vs. Financing Most?

Industry norms and equipment lifecycle drive the equipment leasing vs financing decision as much as any financial calculation.

- Technology/IT: Leasing dominates. Servers, computers, and software hardware obsolesce fast; a 36-month lease keeps you current without owning yesterday’s tech.

- Heavy Construction/Manufacturing: Financing wins. Excavators and CNC machines hold value for decades. Ownership builds equity, and Section 179 amplifies the tax benefit.

- Medical/Dental: Both are common. High-cost imaging equipment often gets leased for flexibility; core clinic equipment gets financed for long-term ownership. See our guide on medical and dental equipment financing for specifics.

- Restaurants/Food Service: Leasing is popular for specialized kitchen equipment with narrow resale markets. Read more in our restaurant equipment financing guide.

- Agriculture: Financing is standard. Tractors and combines qualify for Section 179 and hold strong resale value. Our agricultural equipment financing guide covers crop-season payment structures too.

When Leasing Makes More Sense for Your Business

The honest answer is that leasing isn’t always the inferior option; it’s just the right option in specific situations. Here’s when it wins in the equipment leasing vs financing decision:

- The equipment obsoletes fast. IT hardware, diagnostic devices, and technology-heavy tools are worth leasing; you’ll want to upgrade before you’ve finished paying off a loan anyway.

- Cash preservation is the priority. No down payment and lower monthly payments protect working capital for payroll, inventory, and growth.

- You plan to upgrade every 2–4 years. Leasing builds that cycle in cleanly without the hassle of selling used equipment.

- Revenue is variable. Lower fixed monthly costs give you breathing room in slow seasons.

- You don’t need long-term ownership. If the equipment has no strategic value after the project or contract ends, why own it?

- Clean expense treatment matters. Operating lease payments offset against revenue simply and predictably.

Startups especially tend to benefit from leasing’s lower barrier to entry. Our startup equipment financing guide explains why leasing equipment financing is often the smarter first move for newer businesses.

When Financing (Buying) Makes More Sense for Your Business

Flip the equation, and financing wins clearly in these scenarios:

- The equipment lasts 10+ years. Excavators, industrial presses, and agricultural machinery hold value long after a loan is paid off. Ownership compounds that value.

- Your business is profitable. Section 179 lets you deduct up to $2,500,000 in the year you place equipment in service; a massive year-one tax advantage leasing can’t match.

- You want equity and resale options. Owned equipment is an asset you can sell, refinance, or borrow against.

- The equipment is highly specialized. Custom-built or modified equipment has no practical return market; leasing it makes little sense.

- Your credit qualifies for competitive rates. Strong business credit profiles regularly secure 6–9% financing, making total cost of ownership very manageable.

- You need full operational control. Financing imposes no usage restrictions, mileage caps, or modification limitations that many leases include.

Finding the right lender matters just as much as the structure itself. Our guide to the top equipment financing companies compares top lenders across rates, terms, and approval requirements.

How to Choose: Key Questions to Ask Before Deciding

Before you commit to either side of the equipment leasing vs financing decision, run through these seven questions. Your answers will point you in the right direction faster than any formula.

- How long will I use this equipment? Under 4 years → leasing. 5+ years → financing.

- Will the technology become obsolete? Yes → leasing keeps you current. No → financing builds equity.

- Do I need the Section 179 deduction this year? Profitable year with high tax liability → financing wins decisively.

- How much working capital do I want to preserve? Capital-constrained → leasing’s zero-down structure helps. Cash-strong → financing’s total cost is lower.

- Does my business qualify for competitive rates? Strong credit (680+) opens 6–9% financing. Weaker credit may find leasing more accessible.

- Do I want ownership and resale value? Yes → finance it. No → lease it.

- Will a lease liability affect other borrowing? Under ASC 842, leases hit your balance sheet. If debt covenants matter, run the numbers carefully.

Mostly short-term, flexible, low-capital answers point to leasing. Mostly long-term, profitable, ownership-focused answers point to financing. Not sure which lenders to approach? Our guide to working with an equipment financing broker can help you find the right match.

Frequently Asked Questions

What are the disadvantages of leasing equipment?

You don’t build equity, and total payments often exceed the equipment’s purchase price. Most leases include usage restrictions, mileage caps, or modification limitations. At term end, you either return the equipment or pay a buyout; you’re not automatically an owner.

What is the 90% rule in leasing?

Under ASC 842, a lease is classified as a finance lease if the present value of lease payments equals or exceeds 90% of the equipment’s fair market value. When triggered, the lease gets recorded on your balance sheet as both an asset and a liability, similar to ownership accounting.

What is the difference between leasing and financing equipment?

In the equipment leasing vs financing comparison, financing means you borrow money to purchase the equipment outright and own it from day one. Leasing means you’re paying for the right to use equipment the lender owns, with a possible buyout option at term end.

Is leasing a better option than financing?

Neither is universally better. Leasing wins when flexibility, low upfront costs, and upgrade cycles matter. Financing wins when you want ownership, long-term use, and the Section 179 tax deduction. Your specific cash position, tax situation, and equipment type drive the right answer.

Can you get equipment financing with bad credit?

Yes. Many lenders approve equipment financing and leasing with scores below 620, especially when the equipment serves as strong collateral. Startups and businesses with thin credit histories have options too. See our guide on equipment financing with no credit check for low-credit pathways.

What types of equipment can be leased or financed?

Nearly any business-use equipment qualifies, construction machinery, medical devices, restaurant equipment, commercial vehicles, IT hardware, agricultural equipment, and manufacturing tools. Lenders generally fund anything with identifiable resale value. Soft costs like software or installation are sometimes included up to a percentage of the total deal.

Ready to make your decision? Whether you’re leaning toward equipment leasing & financing or straight ownership, the next step is comparing real offers. Run your numbers with our equipment financing calculator, and match with lenders who fit your credit profile, industry, and timeline, so you close on terms that actually work for your business.

Founder of Nanotom Capital & Nanotom Labs